Economic Commentary: Demographics

While I’m not especially old, I can’t call myself young anymore. When I go to the gym, it takes me longer to stretch than to work out. People my age debate the best vitamin supplements, not the best burger joints. When I am asked for identification at the market, it isn’t to confirm I am old enough to buy beer; it’s to see whether I am eligible for a senior discount.

Signs of aging aren’t confined to my personal life. We see them everywhere: Populations in developed nations are collectively getting older, a trend that will have a tremendous influence on economic performance in the years ahead.

Politics and policy have tended to dominate economic discussions of late. Recent swings on both fronts have created uncertainty for the near-term outlook. By contrast, demographics work gradually and subtly, with a powerful long-term influence. Demographic change may be the most underappreciated economic issue facing the world today.

Roots of the Problem

An economy’s development is powered by a combination of growth in the labor force and growth in productivity. The former is the product of trends in fertility, longevity and immigration.

As an undergraduate, I was exposed to the research of the Nobel Prize-winning economist Gary Becker, who analyzed the economics of fertility (the rate of child-bearing). His study of international data across time and place revealed a startling truth: richer families have fewer children, and poorer families have more. The same is broadly true for richer countries and poorer countries.

This might initially seem counter-intuitive, as wealthier families can theoretically afford to have more children. But children are expensive, both explicitly and implicitly. The opportunity cost of caring for kids (time taken away from work or leisure time) can be substantial, more so for parents with higher incomes. And as with other consumption goods, we tend to substitute away from having children as their costs rise. (I know this sounds heartless, but it is a useful way of explaining the data.)

“The richer the country, the lower its birth rate.”

For families of more modest means, the costs of child-raising are lower. And in many societies, children start contributing to the family’s income at an early age. These conditions favor larger families.

In societies where children are expected to care for the elderly, fertility tends to be lower. The capacity for care is fixed, and must be split between generations. The presence of well-developed child care and elder care programs can change the equation; Japan, for example, is addressing a severe fertility problem by opening more day care facilities.

China provides an interesting case study of the effects of economics on fertility. Interestingly, China’s birth rate was already falling when the one-child policy was implemented in 1979, and declined only slightly after the program began. Since the policy was relaxed in 2016, fertility in China has barely budged. The reason: China’s increasing standard of living.

To be sure, cultural and religious influences have a bearing on fertility. But incentives matter. Countries have tried to promote higher birth rates through various policy measures (exemptions for children in the U.S. tax code are one example). But they rarely have much impact on family size.

Man-made and natural disasters can also have an effect on fertility. Wars and pandemics prompt a replenishment of population. Happily, we have not had a global episode on either front for a long time, but when extraordinary events occur, they create unevenness in the size of successive generations.

The “baby boom” that followed World War II is a case in point. It not only produced a burst in fertility starting in 1946, but an “echo” of that development a generation later. The result was the millennial generation, which is discussed as much for its behavior as its size.

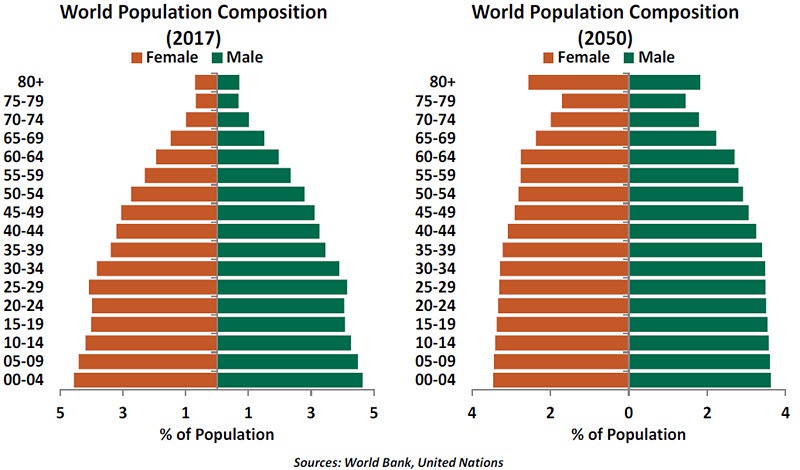

Peaks and valleys in the age distribution can create complications for societies. When they occur, they cause the labor force to wax and wane, resulting in periodic imbalances between those working and those retired. We’re seeing the consequences of both of these phenomena at the moment.

Life Goes On

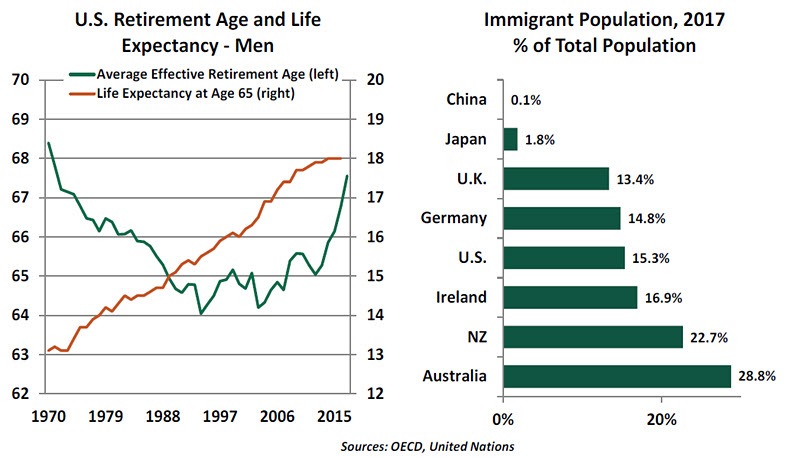

While fertility measures the rate of childbirth, longevity focuses on how long those children can expect to live. In most parts of the world, longevity has been on a persistent upswing, thanks to advances in nutrition and health care. Since 1960, life expectancy for Americans at age 65 has risen from 77 to 83. Measures of the quality of life at advanced ages have also improved. This should, in theory, improve the resilience of the labor force.

However, official retirement ages have not kept pace with life expectancy, and there is still a strong tendency to transition away from full-time employment when benefit payments become available. The more generous these payments, the more likely it is that workers will retire.

With the postwar generation crossing retirement age in substantial numbers each year, sustaining growth in the labor force becomes more challenging. (This also creates an immense problem for retirement systems, which we discuss later.)

“In many places, immigration has become a four-letter word.”

Immigration can help fill in demographic gaps, and has done so successfully throughout history. Countries more open to immigration have better labor force growth; immigrant communities in many countries also have high rates of entrepreneurship and innovation, which can abet economic potential.

But in many places, immigration has become a four-letter word. Uncontrolled migration in several regions has raised anxiety and contributed to an advancing wave of nationalism. Negative rhetoric surrounding immigration has spread quickly, obscuring the more positive aspects of welcoming non-natives.

Immigration is an exceptionally complicated issue, with dimensions far beyond economics. But without sufficient immigration, the demographic challenges faced by many countries will prove more difficult to manage.

Bridging the Divide

Technology provides two main avenues to circumvent the limitations of aging labor forces. The first is tapping into labor supply beyond borders. A dearth of workers in one country might lead to the work shifting to another. Of course, some occupations require proximity between customer and provider, but an expanding range of activities can be done from almost anywhere.

But logistics and politics could limit offshoring. Countries receiving business will need sufficient physical and human capital to handle it; educational attainment (including language skills) and infrastructure in developing countries is often uneven. And the optics of shifting jobs from domestic to foreign workers could certainly arouse concern among nationalists.

The mismatch of population and capital is a central theme to watch in the years ahead. Nearly all of the next generation’s global population growth is projected to come from emerging markets, which are considerably younger. And a significant fraction of this growth will occur in countries considered “dangerous” by the United Nations.

“Demographic imbalances could cause more mass migration in the years ahead.”

Youth can be an asset, if it has the opportunity to achieve. But a lack of opportunity can lead to political instability and the kind of mass migration that has been so challenging over the past several years. The fact that the Mediterranean Sea separates some of the youngest and poorest countries from some of the oldest and richest will provide a continuous challenge for border control in Europe. The same may be true for the frontier separating Mexico and the United States.

The second way in which technology can compensate for aging is in the development of robotics and artificial intelligence. Investment in these areas is accelerating, and the resulting boost in productivity may compensate for slower labor force growth. Androids serving as nurses to the elderly are a poignant example of this theme.

But while the advance of machines might serve those who are retired, they will also threaten those still working. The path to an automated future will be a bumpy one.

Consequences

The implications of aging populations are far-ranging.

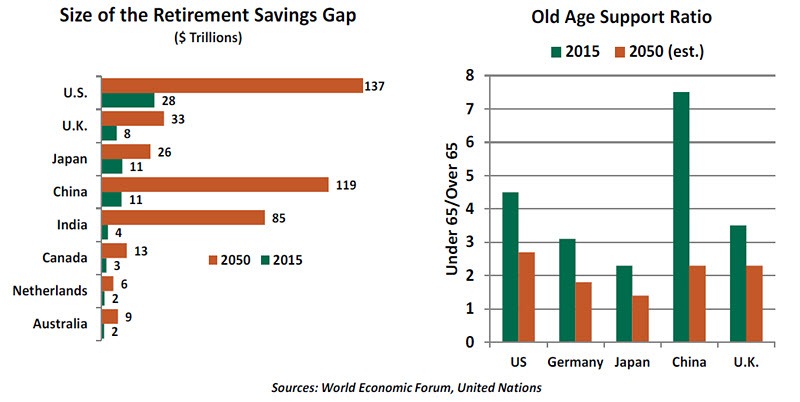

As we discussed last December, the world is poorly prepared for retirement. Individuals and the systems that serve them have been guilty of collective myopia, which will make the golden years much less golden.

Behavioral economists have demonstrated that human beings struggle with complex problems, especially when the consequences are far off into the future. Determining how much to save, how to invest, and how to manage resources after retirement are difficult tasks for most people. Pension systems, whether public or private, take these weighty matters off of peoples’ hands and vest them in administrators who (in theory) have the background to address them successfully.

But the rise in longevity creates a challenge for retirement planning. Participants and systems have had to adapt to retirement horizons of twenty years or longer, which require substantially higher levels of saving and asset accumulation.

And as corporations and governments seek to shed the risk and responsibility that comes with administering retirement plans, pensions have been in decline in many parts of the world. In some cases, this has been done intelligently (the Australian superannuation program is one example). In others, individuals have been left adrift. Defined contribution plans, which shift responsibility for the plan’s funding and performance to the individual, have become much more common; used well, they can be successful. But not everyone has access to such plans, and some who do choose not to participate. And still others fail to save sufficiently or make good investment choices.

“Problems with retirement systems are broad and deep.”

Government-provided retirement programs take a range of different forms. But without sufficient distance between these systems and the broader government ledger, bad outcomes can emerge. A legislature struggling to balance its budget or pursue other fiscal objectives may defer contributions to the retirement system, placing it in an underfunded position when benefits become due. In the United States, Illinois is an acute case of this, but systems in other parts of the world have a similar affliction.

Addressing shortfalls will require new taxes, reductions in benefits or diversion of funds intended for other uses. None of these will be favorable for economic growth. Data show a shocking fraction of citizens will be heavily reliant on government benefits in retirement, which will make reform even more challenging.

It doesn’t help that the historically low levels of interest rates are limiting returns to retirement plan assets. (The fraction of government debt carrying negative yields recently set a multi-year high.) Some administrators have increased the riskiness of their investments in an attempt to close gaps, but that could prove costly.

The approach and arrival of retirement has other important economic effects. Workers nearing retirement age are much less likely to change jobs, reducing the dynamism of the labor force. Workers who pass retirement age typically become thrifty, to avoid outliving their savings. And the elderly use more government-provided health care, increasing the burden on sovereign finances.

Older populations living on fixed incomes are more sensitive to tax increases, and they vote in far higher concentrations than younger cohorts. This will make fiscal policy debate more difficult at a time when government indebtedness is rising rapidly. At a local level, the elderly are less likely to support investments in education (their children having long since graduated), hindering efforts to enhance human capital formation.

“People are working longer, but there are limits to this trend.”

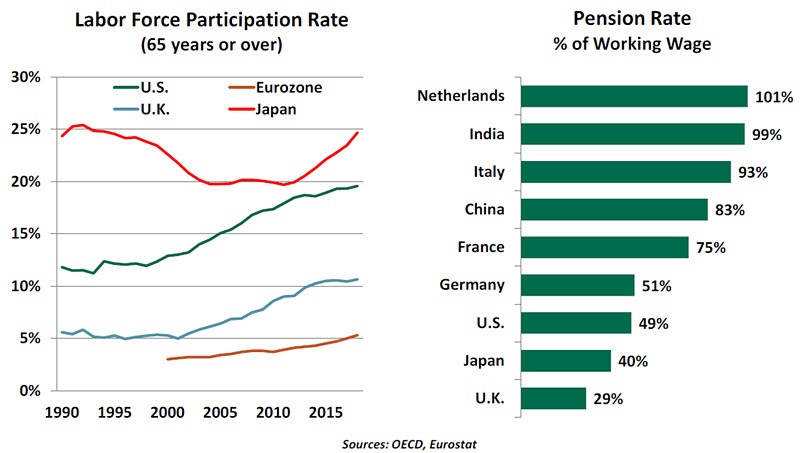

One clear solution to all of this would be for workers to remain in the labor force longer. And in fact, a trend in this direction has been underway for some time. As people are healthier at advanced ages and more commonly work with their minds than their backs, longer careers are within reach. This development could be extended with a stick (raising retirement ages) or a carrot (offering incentives to remain in place).

But studies are showing that productivity declines with the age of workers, who become progressively less able or willing to adapt to new technology. (It takes me six months to get used to all of the features on a new mobile device.) Employers may therefore not encourage baby boomers to stick around. And some countries offer generous retirement benefits, which can be alluring.

Demographic transition in developed countries could also have implications for asset markets. In the United States, baby boomers aspired to be suburban homeowners. The generations that followed them preferred to rent in urban settings. Some of this is the product of financial considerations: the financial crisis and student debt caused young people to view homeownership differently than their parents. This will leave a geographic mismatch between supply and demand that has implications for commercial real estate (especially for retail), as well.

Academic work on the potential impact of aging on equity prices has been mixed. In theory, more sellers (baby boomers) than buyers (Generation X) would depress prices, all else equal. But studies examining this impact have not found a strong causal link.

Conclusions

In one sense, the population problem in developed markets is temporary. In the United States, the millennial generation is already larger than that of the baby boom, and projections suggest labor force growth will begin increasing again within the next ten years. The ratio of those working to those retired should eventually begin to recover, to the benefit of pension and health systems.

But in the meantime, slow labor force growth will limit economic growth. During this interim, the global mismatch of old and young has the potential to sustain nationalist spirits that are also hesitant about trade. Deprived an avenue to prosperity, young people in emerging markets will be restless, making the world a less secure place. The support for international coordination will be waning just as it is needed the most.

“Once you fall behind the aging curve, it is very hard to catch up.”

The march of demographics may be slow, but it is sure. And while the consequences of aging may seem far off into the future, they will be substantial. Unless we address them now, they will become much less manageable later.

And now, if you will excuse me, it is time for my vitamins.

Author

Northern Trust Economic Research Department

Northern Trust