ECB round-up: Could Draghi’s QE extension fail to materialise?

The ECB announced no changes to its policy at this month's meeting, which was expected by the market. While President Draghi's introductory statement offered no further insight to the ECB's future decisions regarding interest rates and QE, his response to the journalist Q&A was more interesting. He said that there had been no discussion of an extension to the current QE programme when it expires in March, however he dismissed the idea that that the Bank would stop QE without tapering first.

This information is not as hawkish as it first seems, since Draghi also went on to make a defence for negative interest rates, using the latest ECB Bank Lending Survey as evidence that the pace of lending activity is picking up in the currency bloc as a result of the Bank's current policy. The Bank also said that current policy is necessary to target a 2% rate of inflation. The latest price data from the currency bloc showed some pick-up in prices last month, with Spain and Italy exiting deflation, however the core rate of inflation remains stubbornly below the 1% level, even with the ECB's current QE programme.

Will Balance sheet fear tie the ECB's hands?

Although we believe that deflation risks in the Eurozone are receding, we still don't think that the Eurozone economy is out of the deflationary woods yet, so QE is unlikely to end anytime soon. We do expect the ECB to announce that it will lengthen its asset purchase programme when it ends in March 2017, market expectations are for an announcement at its next policy meeting in December. However, we think that there is a small but significant chance that the ECB may hold off from expanding its QE programme, or it may only extend it in the short-term, as the ECB's whopping EUR 3.5 trillion balance sheet creates a liquid monetary environment even if QE stops.

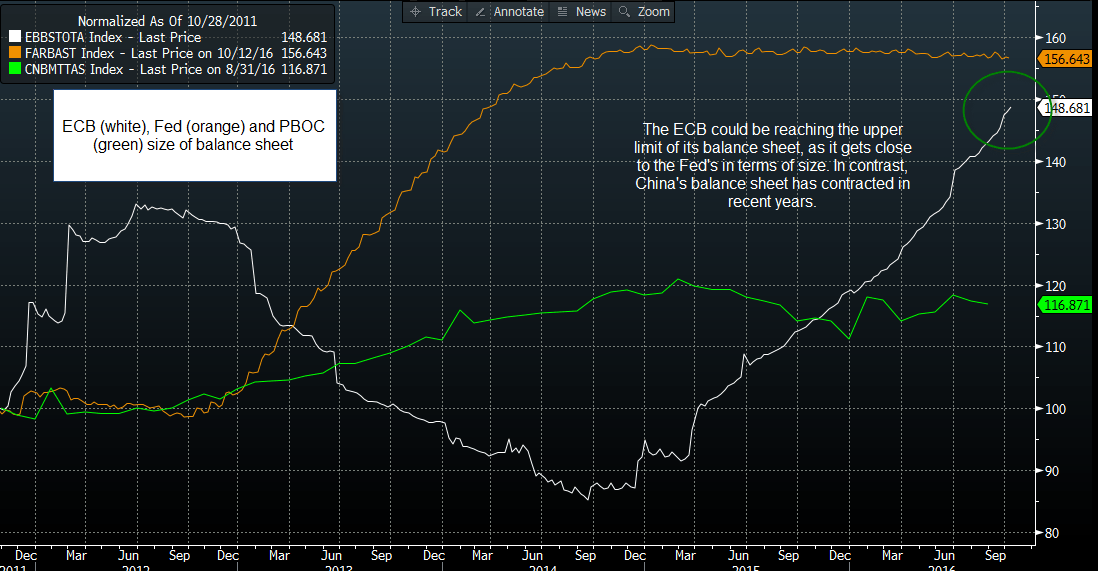

Is the ECB balance sheet reaching its upper limit?

For now, it is business as usual for the ECB, but we are aware that the size of the Bank's balance sheet could be reaching its upper limits. Figure 1 below shows the ECB, Fed and PBOC balance sheets. This chart has been normalised, to show how they move together. The Fed's balance sheet is still the largest, however, its balance sheet has been stable since 2014. The PBOC's balance sheet has actually fallen in recent years as Beijing has sold FX reserves to boost the value of the renminbi. In contrast, the ECB's balance sheet has surged in size, which could make some of the more hawkish elements of the ECB concerned about extending its QE programme next year.

FX market takes Draghi literally

The market impact from this meeting has been EUR negative, as Draghi's dovish tone weighed on the single currency. EUR/USD has backed away from 1.10, and is currently at its lowest level since June. If we get below 1.0913 – the low from 23rd June – then we could see a sharp move back towards 1.08 in the short term for this pair. One of the key drivers of the ECB-inspired euro weakness, has been a sharp decline in German bond yields, the 10-year yield has fallen seven basis points since Draghi has been talking, and is now a mere 0.01%. If German 10-year yields fall back into negative territory this could trigger another wave of selling pressure on the EUR.

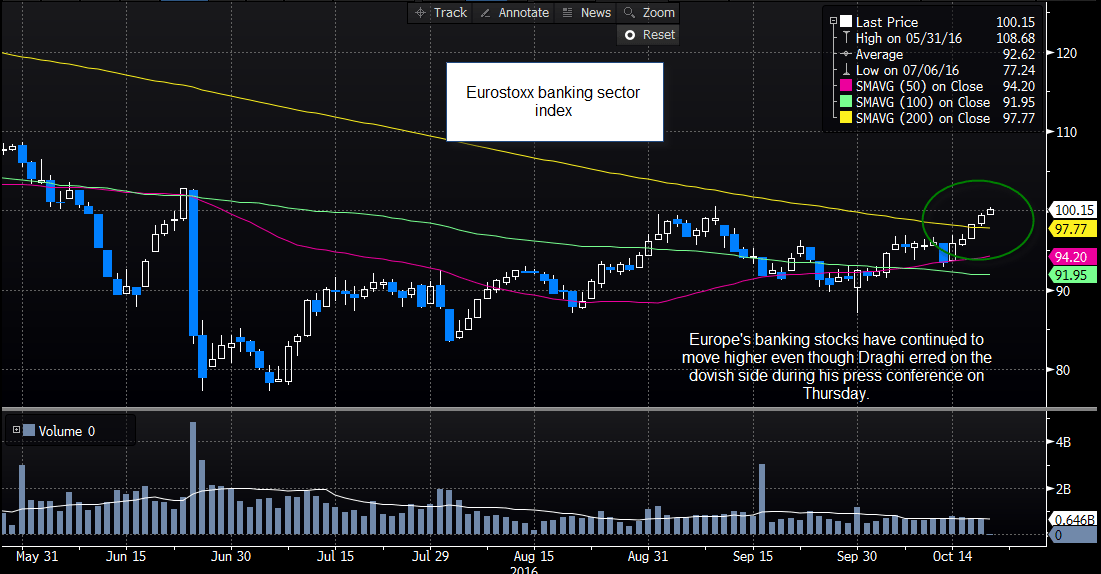

Bank stocks see signs of hope in Draghi's speech

In contrast, European stocks are eeking out a gain, the Eurostoxx index is currently up 0.2% (at the time of writing). More interesting is what is happening in the banking sector. Even though German bond yields and the euro appear to be pricing in the prospect of an extension to the ECB's asset purchase programme, the Eurostoxx banking sector index has actually risen since Draghi started speaking (see figure 2). This index has come under pressure since the ECB announced its QE programme back in March 2015, however, this index has staged a decent recovery so far this month. QE and negative interest rates are perceived as bad news for the banking sector, as they weigh on the profitability of banks' lending activities. The fact that European banking stocks appear to be resilient to Draghi's dovish message, suggests that some investors may also believe that the ECB cannot extend its QE programme too far, and anyone looking for a long-term increase to the ECB's asset purchase programme could be disappointed. This is worth watching, and we wait for more info from the ECB in a couple of months' time.

Figure 1:

Figure 2:

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.