ECB Preview: Between Putin's rock and hard inflationary place, the deck is stacked against the euro

- The European Central Bank is set to raise rates by 75 bps to battle rising prices.

- Investors will eye signals for October's move and comments on the energy crisis.

- A speech from Fed Chair Powell during ECB President Lagarde's presser could add to EUR/USD volatility.

Choosing the least worst option – that is the dilemma for the European Central Bank as it convenes in September, after a summer of soaring energy prices. A mix of hints about the near future, new forecasts, President Christine Lagarde's comments about electricity bills are all set to shape EUR/USD's reaction. A speech by Fed Chair Jerome Powell scheduled to coincide with Lagarde’s press conference could add fuel to the fire.

Here is some background and three factors I consider critical to the euro's response.

Inflation is up, up and away

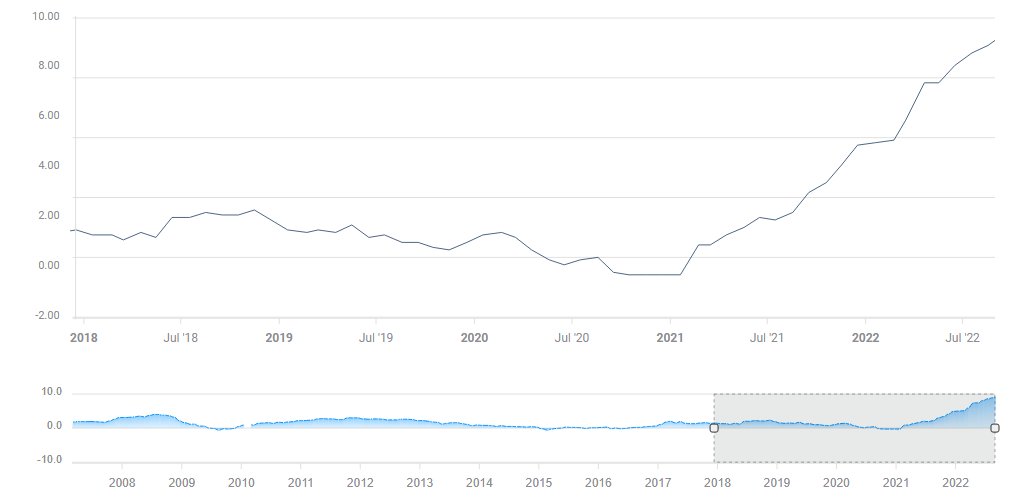

The ECB’s mandate is to achieve a 2% headline annual inflation rate. Its "single needle in the compass", though, is feeling the heat. The Consumer Price Index (CPI) has hit 9.1% in August.

Source: FXStreet

The bank has already taken its initial step – aka the "liftoff" to battling rising prices. It increased the main lending rate from 0% to 0.50% in July and set the deposit rate at 0%, a welcome change for lenders after years of punishing banks for parking money with the ECB. The era of negative interest rates ended, and lending has become dearer in the eurozone. Back then, the bank also promised to continue raising rates.

Will higher interest rates push energy prices lower? No, but I will get to that shortly. The Frankfurt-based institution has several good reasons to increase borrowing costs. The economy grew by 0.8% QoQ in the second quarter, the unemployment rate dropped to 6.6% – low in European standards – and Core CPI is elevated as well.

Excluding food and energy, prices are up 4.3% YoY as of August, showing that inflation has propagated to other parts of the economy. It is essential to remember that unionization is higher in the EU than in the US – collective bargaining raises wages and consumer prices.

The Russian factor

High energy prices propagate to other areas – but also leave less money in consumers' pockets. Gazprom's latest decision to leave the Nord Stream pipeline shut for longer added to the angst. While gas depots are nearly full in Europe, current storage capabilities are insufficient to pass the winter without any cut in demand – and that would be painful for Europe's largest economy.

Germany is not only dependent on gas to heat homes, but also to keep its industry humming along. The chemicals, steel and glass sectors are energy hungry. Restricting supplies to them could cause significant economic pain, on top of high bills. In turn, that would leave less money in consumers' pockets, easing price pressures and bringing inflation down.

In such a scenario, the ECB would unnecessarily add to economic pain. That is the bank's dilemma.

What will the ECB do?

Economists see the ECB as having a small window to raise rates in the goal of keeping core inflation from becoming entrenched while the broader economy is still hot. It would later need to halt its tightening cycle or reverse it, depending on energy prices. But for now, there is room to raise rates.

Since the last weekend of August, officials at the central bank have been drumming up their hawkish intentions, signaling a 75 bps rate hike. That talk has helped EUR/USD stabilize – the weaker exchange rate has added to higher costs of imported goods, including fuel.

That has now become the base case, and the first factor to watch.

Three factors to watch

1) Rate hike

As just mentioned, money markets are expecting the ECB to raise rates by 75 bps – the main lending rate from 0.50% to 1.25% and the deposit rate from 0% to 0.75%. In such a scenario – which is the most likely one – the focus will swiftly shift to the next factors.

In case the bank is wary of the energy crisis and raises rates by only 50 bps, the euro would tumble down, and the other factors would do little to change this downward dynamic. It would be hard to believe any hawkish promises from policymakers if the bank fails to deliver on expectations it created.

In the unlikely scenario of a 100 bps hike, the euro would experience a positive shock and surge. It would be "un-European" to act with so much determination.

2) October and beyond

Markets are currently pricing a 50 bps hike in October and another such increase in December. The ECB is unlikely to lay out its full plans – which it probably doesn't have, at least for December – in the statement. Nevertheless, President Lagarde will surely be asked about it by reporters.

A determined message to raise rates by at least 50 bps in October and beyond would help the euro, while refusing to convey a hawkish message would restrain the common currency.

The ECB publishes new growth and inflation forecasts at this juncture and these could serve as hints to where policy is headed. If the bank foresees a recession, it would lower the chances of further rate hikes and send the euro down. A denial of such an outcome would indicate that the ECB is focused on bringing prices down, raising rates. That would boost the common currency.

3) What the ECB says about Russia

Lagarde will likely say the future is uncertain mostly due to energy prices, and that the bank has no preset path and will act according to its best judgment. That would amount to dodging the question, but markets hate uncertainty and it could hurt the euro.

If she says the ECB will do whatever it takes to bring inflation down, the euro will surge despite the potential economic damage. Yet she might want to say something like this to shore up the exchange rate and thus contribute to lowering inflation.

The other scenario would be painting a gloomy picture about the future, acknowledging damage has already been done and signaling the ECB's tightening cycle is drawing to an end. That would send the euro tumbling down.

Conclusion and the Powell factor

EUR/USD will first respond to the rate decision, with a 75 bps hike being the base case scenario. A 50 bps move will hurt the euro. Showing determination about raising rates, especially two 50 bps moves in the remainder of the year, will be positive, while hestiance will weigh on the common currency. Comments about the impact of energy will also be closely watched.

Around 25 minutes after Lagarde takes the stage in Frankfurt, Federal Reserve Chairman Jerome Powell addresses a conference in Washington. Both are lawyers in training and the head of the Fed will also likely advocate for higher rates. While he is unlikely to offer up any surprises, any comments regarding inflation will likely keep the dollar bid.

Reporters could relay Powell's comments to Lagarde, adding to the choppy price action, but probably not changing the big picture for the Fed.

Final thoughts

The ECB is stuck between a rock and hard place. Any hike, any hawkish message, and any pledge will likely support the euro only temporarily. I see a greater chance of EUR/USD ending the event at a lower spot than where it starts.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)