ECB keep pedal to the metal, time to pep up Britain

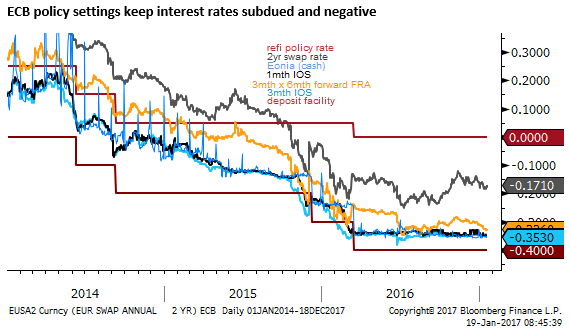

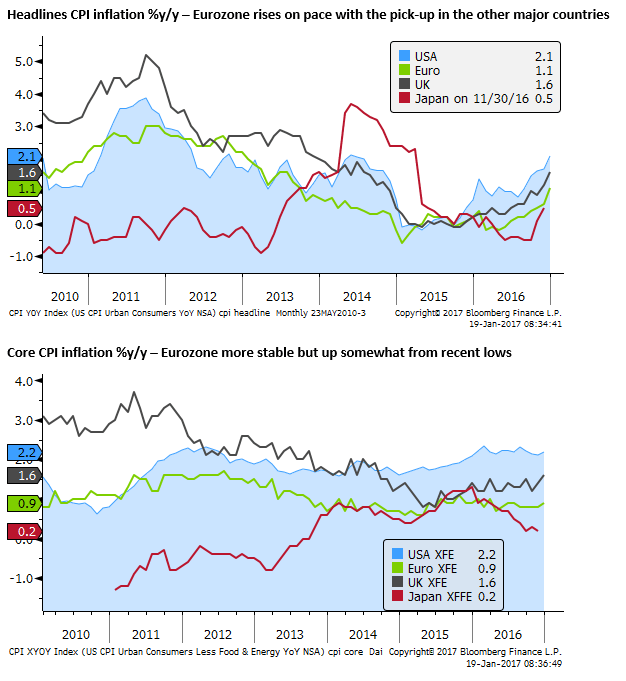

ECB maintained its aggressive accommodative monetary policy to drive home the advantage now that its economic growth and inflation outlook have improved. ECB President Draghi struck a dovish tone seeing the recent rise in headline inflation as transitory and remaining focused on the more subdued core inflation, remaining excess capacity and ongoing financial sector repair. The low negative interest rates and the prospect of falling real interest rates should keep the EUR relatively weak.

The UK press continues to view Brexit uncertainty as a glass half-empty, handwringing over the how the UK will cope without the comfort of the single market; in a typically British manner. As such we see scope for the mood to improve and confidence to build in the optimistic and inclusive open trade vision offered by UK PM May. EU export growth to the UK has grown much more than UK trade to the EU in recent years, leaving the UK with a growing goods trade deficit with the EU. UK trade volume with the EU will decline, but surely it will also rise with the rest of the world, providing an offset. Fear is paramount in the financial services sector, but global financial services firms are unlikely to rush to the door until they have a very good reason. In the meantime, the UK economy appears to be benefiting from the weaker GBP, generating robust growth and higher inflation expectations. Should the EU attempt to punish the UK in negotiations, they too will suffer, suggesting calmer minds will prevail in the end.

Draghi Drives home the advantage

The ECB left unchanged its policy levers; continuing with its NIRP ad QE purchases that are slated at 80bn per month until March and 60bn until December. It acknowledged the pick-up in headline inflation, but said “underlying inflation pressures remain subdued.”

The statement also said, “The Governing Council will continue to look through changes in HICP inflation if judged to be transient and to have no implication for the medium-term outlook for price stability.”

The ECB has not always considered a rise in headline inflation driven primarily by higher energy prices as transitory. Several times in its current NIRP/QE policy easing cycle, the ECB spoke of the negative long-term impact lower energy prices appeared to have on inflation expectations, suggesting lower energy prices were a factor contributing to policy easing. As such, the ECB is taking a relatively dovish position by its standards.

The statement also continues to say that the ECB could ease further if required. It does not say that policy easing could be wound back earlier if conditions improve. Draghi continued to call this a “high-quality problem.” This continues to suggest that the ECB sees the bigger risk as a slower recovery in inflation towards its target, and perhaps is willing to risk inflation running above target at some point in the future.

The market was not looking for any policy changes or shift in the key parts of the statement at this policy meeting. Nevertheless, economic growth and inflation have picked up or look more promising in recent months, and the risk, if anything, was that the ECB might sound less dovish. In contrast, the ECB appears more interested at this stage of driving home the advantage of its policy easing, maintaining its vigor and helping raise inflation expectations, and lower real interest rates.

Time to pep up on Brexit

Most commentators, in particular, those in much of the British media, continue to look at Brexit as a glass half-empty. There continues to be much handwringing and a proclivity to criticize PM May and her plans for Brexit.

There is no doubt there is considerable uncertainty at this early stage of a multiyear process, and the possibility to see much downside. However, the market is yet to really consider that outside of the shackles of EU membership the UK may be able to prosper.

The EU continues to face its own significant problems that will also take many years to resolve with uncertain outcomes. It is far from clear that it is flexible enough to cope with political and economic divergence within Europe.

As May pointed out during her speech on Tuesday, the UK has not clearly benefited as a trading partner in Europe. Perhaps it has less to lose from broadening its focus from intrinsically EU focused trade and investment to viewing the EU as just part of its global market. She noted that, since joining the EU, trade as a percentage of GDP has broadly stagnated in the UK.

Leaving the EU will presumably diminish UK trade with the block, but we do not know by how much. EU leaders have frequently observed that Britain should not expect to get out of the EU without paying some price. They want existing members to see benefits of membership. But equally, they stand to lose if they treat the UK with contempt. EU exports to the UK have growth more significantly than UK exports to the EU, resulting in a widening UK trade deficit with the EU. Germany is the UK’s top import partner; the USA is the UK’s top export destination.

The harder EU deals with the UK, the more likely the UK will move more of its trading volume to the rest of the world. In any case, we might expect trade with the rest of the world to increase as a result of Brexit and serve as an offset to lower trade volume with the EU.

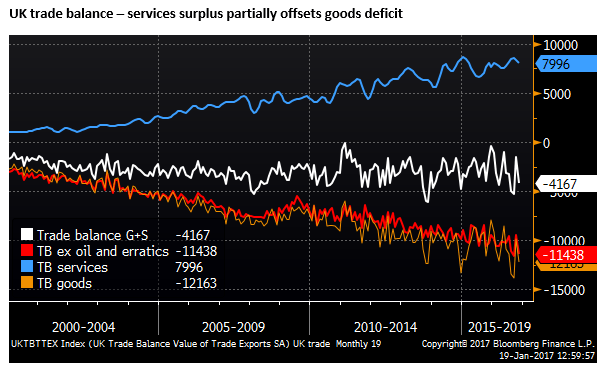

Of key concern is the UK financial services sector. As the charts below show the UK has enjoyed a growing services trade surplus. In Q3-2016, financial services (GBP11.0bn) was 44% of the total services surplus (GBP25.1bn).

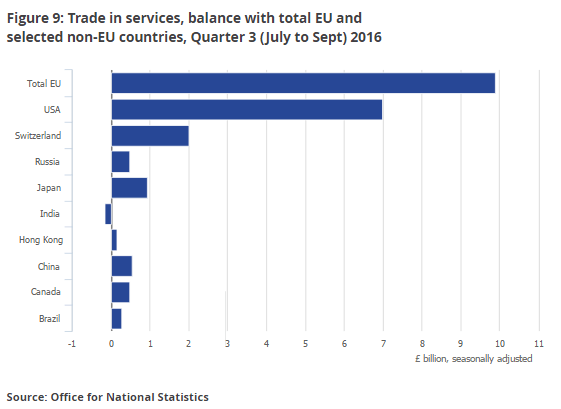

The chart below shows that the EU accounts for more than half of the services surplus, followed by the USA.

Much of the Brexit fear relates to the potential loss in the UK’s net export of financial services. Some of this activity is naturally going to be transferred to the EU. How much remains unclear. A good deal of the financial services conducted in the UK are not generated by demand for European financial products or are financial products sold to Europeans. The UK has historically enjoyed a position as a global financial center; if the UK works hard to maintain strong global trading relationships and achieves a reasonable basis on which to be able to conduct business with European entities, the UK financial sector may not be too badly undermined.

The following article in the FT attempts to gauge the mood of global financial firms operating in the UK. Consistent with the uncertainty, it suggests that large US banks are likely to be slow at first in moving jobs from London, waiting for more information on how Brexit negotiations unfold, in contrast with some more alarming recent media reports. It is a costly and difficult process moving people from the UK to Europe. There needs to be a very good reason. Banks may shift some jobs to European branches, but they will need convincing that it is necessary to move the staff that participate in global markets.

Author

Greg Gibbs

Amplifying Global FX Capital

Greg has had a long career in foreign exchange. He began his career at the Reserve Bank of Australia in 1989 and in the early 1990s he was the first economics graduate at the Bank to be assigned to the foreign exchange dealing desk.