Durable Goods Orders continue to showcase weak capex demand

Summary

Durable goods orders rose again in May, but the data are still consistent with a sector struggling to find its footing. Our read on the monthly volatility is that the industrial space is stabilizing and remains some time off from a true recovery.

Similar durables volatility

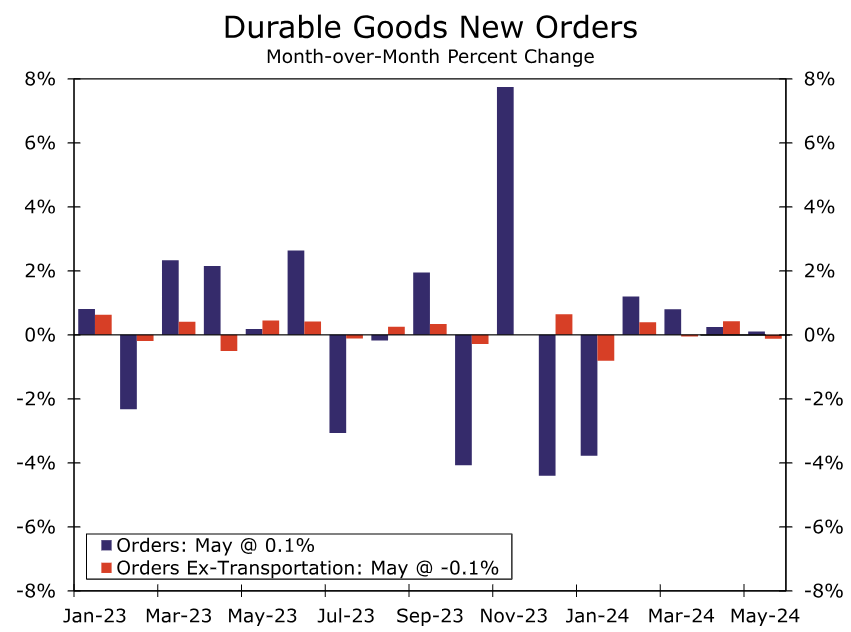

In what was a better-than-anticipated outturn, new orders for durable goods rose 0.1% in May (chart). We were bracing for overall orders to be constrained by nondefense aircraft based on a relatively low number of orders reported by Boeing during the month. In actuality nondefense aircraft orders slipped 'only' 2.8% in May, and defense and motor vehicle orders were up, offsetting some of the weakness. It has been particularly challenging to get a clean read on the volatile aircraft component lately. When we exclude broader transportation, orders were weaker, slipping 0.1%, and underlying activity was muted across major items.

To that end, while overall orders revealed a bit of an upward surprise, the report was consistent with a fairly-weak demand environment as capex conditions remain constrained by elevated costs and uncertainty generally. Consider the monthly pattern of core capital goods orders has flip-flopped between negative and positive growth since the start of the year. Orders slipped 0.6% in May after rising 0.3% in April and are now down a modest 0.2% over the past year, a clear sign that while the manufacturing sector has shown some recent signs of stabilization, a recovery remains some time off.

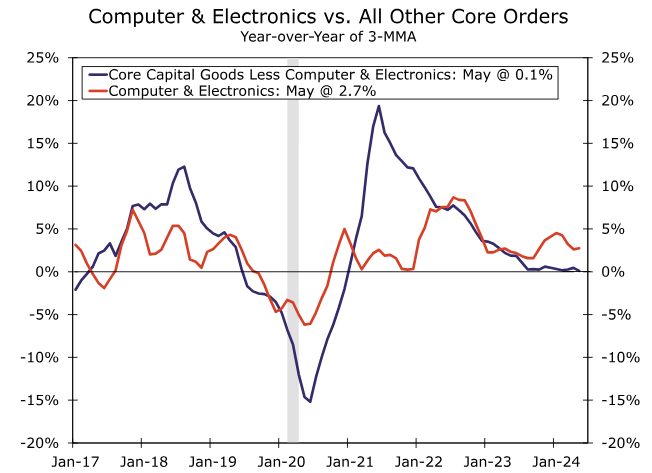

The lone area of strength in this release continues to come from computers, where orders leaped 1.3% in May and are now up north of 14% over the past year—the fastest of any category. Computers continue to be a standout area in an otherwise lackluster demand environment (chart).

Source: U.S. Department of Commerce and Wells Fargo Economics

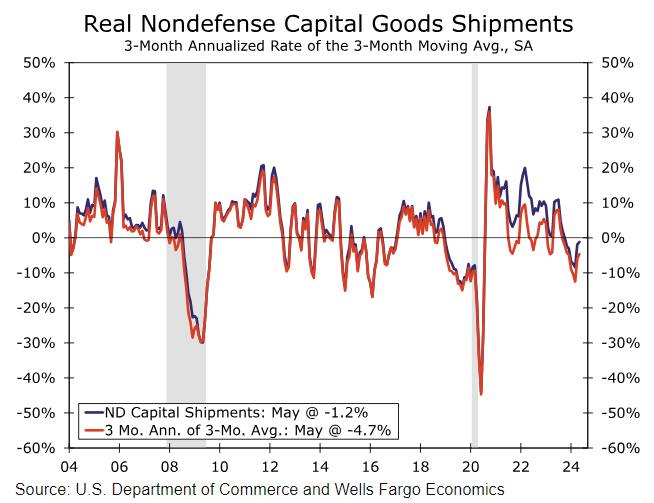

Production activity also appears weak as durable goods shipments slipped 0.3% in May. While the orders data give the latest indication on demand conditions, it is shipments activity that ultimately flows into calculations of equipment spending in GDP accounting. Specifically, the capital goods components are a useful gauge for current quarter equipment investment. Core capital goods shipments (including aircraft) slipped 1.5% during the month, which was a bit weaker than we had penciled in (chart). This, combined with upward revisions to first-quarter equipment investment separately released in the third estimate of GDP growth this morning, suggests some downside to our estimate for real equipment spending to advance at around a 5% annualized rate in Q2.

We're ultimately braced for a dull second half of the year in terms of capex demand and look for the industrial side of the economy to progress within its recent narrow range over the course of the year. Capex conditions are unfavorable, and even if the Fed is able to lower rates later this year, we're unlikely to see a reprieve in terms of borrowing costs until next year. Some further clarity in the post-presidential election environment will likely also be more supportive of demand come 2025.

Author

Wells Fargo Research Team

Wells Fargo