Drastic shift in natural gas outlook

European gas prices have collapsed over the Northern Hemisphere winter. Mild weather and weak industrial demand have ensured that gas storage has remained strong. The region should get through this winter comfortably and prospects also look better for the 23/24 winter. While we have cut our forecasts, significant risks to the upside remain.

European storage to finish heating season well above average

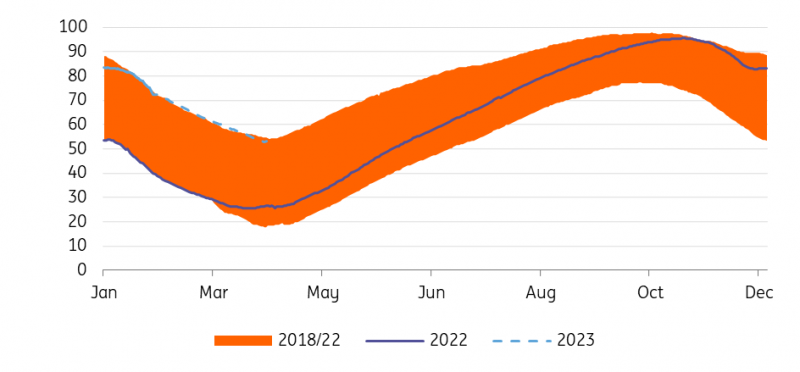

A late start to the 2022/23 heating season saw Europe building gas storage almost until mid-November. At a little over 95% full, storage was essentially maxed out. This was far above the target of 80% by 1 November 2022 set by the European Commission. While there have been some cold spells in the current heating season, it has been largely mild, which has meant storage levels have held up well. In fact, there have been days this winter when storage has seen net increases. Storage at the moment is 72% full, well above the five-year average of 54% for this time of year.

Assuming Europe does not experience a prolonged cold spell in the current heating season, the region should exit the 2022/23 winter with storage above 50% full. This is significantly higher than the 26% seen at the end of the last heating season and above the five-year average of 34%.

Ending this winter with very comfortable inventories makes the job of refilling storage over the injection season and hitting EU inventory targets of 90% by 1 November 2023 easier. Between 1 April and the end of October last year, the EU added in the region of 67bcm to storage. If we were to see similar storage levels at the start of the next heating season, the EU would only need to add around 43bcm of gas this year.

EU storage to exit this winter comfortably (% full)

Source: GIE, ENTSOG, Eurostat, ING Research

Aggressive demand cuts

The level of demand destruction seen in recent months has been considerable. The latest numbers from Eurostat show that EU demand was 25% below the five-year average for October 2022 while Germany’s weekly data shows declines in the first two weeks of 2023 in excess of 30% from the 2018-21 average. However, it is important to note that demand in the third week of January was only around 9% below the 2018-21 average. Splitting it out, household demand was down 8.8% while industrial demand was almost 10% lower than the 2018-21 average. We will need to keep an eye on this, but it could suggest that demand is starting to respond to the lower price environment.

The reduction in demand in recent months has far exceeded the Commission’s target of 15% below the five-year average between August 2022 and the end of March 2023. As a result, the level of demand destruction that will be needed from April through until March 2024 is more modest than initially expected. Our numbers suggest that a 10% decline from the five-year average is needed between April 2023 and March 2024 to meet the European Commission’s 90% storage target by 1 November 2023. The requirement for lower levels of demand destruction suggests that prices do not need to go as high as initially expected.

However, two key assumptions behind this are that remaining Russian daily gas flows stay unchanged and that LNG import volumes into the EU grow marginally year-on-year in 2023. The big uncertainty over LNG flows into Europe is how strong a demand recovery we see from China this year.

LNG market still tight in 2023

A well-supplied European market has meant that we have seen some shifts in regional spreads. Most noticeable is the spread between TTF and Asian spot LNG. For the bulk of last year, TTF was trading at a premium to Asian LNG in order to pull in cargoes and make up for Russian supply losses. However, since mid-December, TTF is trading at a discount to Asia. This should support the redirecting of LNG cargoes towards Asia.

Admittedly looking at the forward curves, TTF’s discount to Asia is only in the prompt market, and further along the curve there is little between the two markets. Clearly, there is little aggressive competition between the two regions for cargo at the moment, but this could change as China returns from its Lunar New Year holidays.

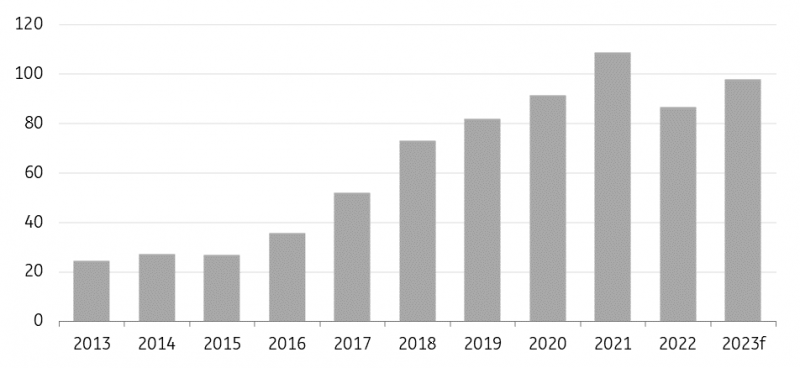

Weaker Chinese demand through 2022 offered relief to Europe. Last year, China imported 87bcm of LNG, down 20% year-on-year and the weakest annual import volume since 2019. However, the relaxation of Covid measures and several support measures to help the domestic property sector could drive a recovery in demand this year. China also has a larger volume of contracts with fixed destination clauses this year (100bcm vs 88bcm last year according to the IEA).

Ultimately though, Chinese demand is a big uncertainty for the global LNG market. While we are likely to see an increase in demand, it is difficult to gauge exactly how much stronger it could be this year. We are assuming for now that Chinese demand will not return to 2021 levels. Instead, we are expecting more modest growth of a little over 10% YoY.

The restart of the Freeport LNG plant (20bcm per year) could provide some relief to a tight LNG market, particularly if we see stronger-than-expected Chinese demand. There appears to be some progress on the regulatory front for the restart of the plant, but the market may have to wait a while longer for exports to resume.

Chinese LNG imports to see partial recovery in 2023 (bcm)

Source: China Customs, ING Research

The highs are behind us

The more comfortable storage situation does put Europe in a better position to handle the 2023/24 winter. It certainly isn’t looking as dire as it did just several months ago. Therefore, prices do not need to go as high as originally expected going into the next heating season. We expect TTF to average in the region of EUR60-65/MWh over the first half of 2023, increasing to EUR75-80/MWh over the second half of the year. The assumptions around this are that there are no further declines in remaining Russian gas flows, that we see a small increase in EU LNG imports over 2023 and that Europe experiences a normal winter in 2023/24. This should allow the EU to start the next heating season with storage exceeding the European Commission target of 90% by 1 November, and the region should get through the winter months in a fairly comfortable manner. However, Europe will rely more on storage in the 23/24 winter than it has in the current winter.

ING natural gas price forecasts

Source: ING Research

What are the upside risks to our forecasts?

There are two key upside risks to our new forecasts. Firstly, the bulk of Russian gas flows to the EU have already been halted. However, there is still the risk that flows via Ukraine and possibly even through TurkStream are stopped. If this was to occur, Europe could lose 15-20bcm of gas on an annual basis, which is still a sizeable volume. This would need to be made up either by further LNG imports or through higher levels of demand destruction. Both would likely require prices to move higher from current levels.

The second key risk is related to Chinese LNG demand. We are assuming only a marginal recovery in Chinese import demand this year (a little over 10%), rather than returning to 2021 levels. If Chinese demand surprised to the upside, this would mean a tighter-than-expected LNG market, increasing the need for Europe to compete more aggressively with Asia for supply. This would also mean higher-than-expected prices.

Read the original analysis: Drastic shift in natural gas outlook

Author

Warren Patterson

ING Economic and Financial Analysis

Warren Patterson is a commodities strategist at ING. He joined the bank in April 2016 and covers the entire commodities complex. Previously, he worked at a commodities trade house in London.