Don’t get carried away by North Korean market vol

A low-probability but high-impact event for markets

This week, tensions have escalated between North Korea and the US. The recent chain of events started after the United Nations Security Council last weekend hit Pyongyang with new sanctions as punishment for North Korea's aggressive missile testing programme. This triggered aggressive comments from North Korea followed up by a statement by US President Donald Trump on Tuesday, in which he said that the country's threat would be ‘met with fire and fury like the world has never seen'. The North Korean regime responded by threatening to attack the US's Pacific territory of Guam by launching four intermediaterange missiles which would land about 20 miles offshore and could be launched as soon as next week. On Thursday, President Trump said that his statement on Tuesday ‘maybe wasn't tough enough'.

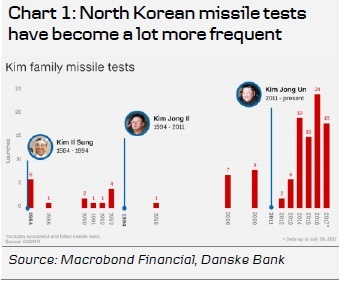

The driver behind the escalation is North Korea advancing fast in developing an Intercontinental Ballistic Missile (ICBM) that could reach the US with a nuclear warhead. North Korea conducted its first ICBM test on 4 July and followed up with a second ICBM test on 28 July which led to the recent UN sanctions. How close North Korea is to posing a nuclear threat to the US mainland is difficult to say, but the Pentagon's Defence Intelligence Agency announced on Tuesday that they believe North Korea will be able to field a reliable, nuclear-capable ICBM as early as next year. North Korean tensions have gradually risen since Kim Jong Un came to power in 2011 and the current situation is probably the most tense it has been for many years. (See Chart 1). Still, the most likely scenario is that the current escalation of events does not lead to a military confrontation as both parties will have too much to lose from such an outcome. However, it is also difficult to foresee a sudden improvement in US-North Korean relations and recent events may increase long-term frictions in US-China relations.

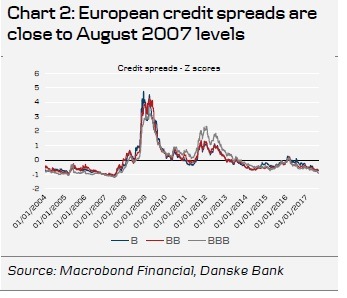

Markets have reacted as expected this week with yields of US and German government bonds declining, equities selling off and safe-haven currencies like the Swiss Franc (CHF) and the Japanese yen (JPY) strengthening. Although Japan is close to the epicentre of the crisis, the JPY typically strengthens during North Korean tensions as Japan is a creditor nation and local investors typically ‘bring money home' when they face a crisis. Despite a slight pick-up in market volatility, risk premiums are very low across asset classes. For example, VIX volatility and European credit spreads have only edged modestly higher from August 2007 lows (See Chart 2).

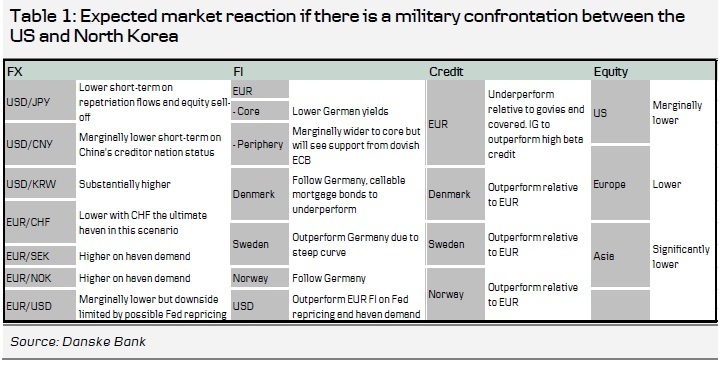

Military confrontation between the US and North Korea is a low-probability but highimpact event for markets. That naturally makes it difficult for markets to price it. In recent years, geopolitical tensions have had a brief, albeit sharp, impact on markets as central banks have come to the rescue. In our base case, in which the North Korean situation does not escalate into a military confrontation, we would expect the current risk aversion to be temporary although it is likely to be bumpy and very much headlinedriven. In the risk scenario, where the current tensions escalate sharply, we would expect an acceleration of this week's price action, i.e. a sharp rise in risk premiums across asset classes, substantial falls in US and German government bonds yields, significant JPY and CHF strength and a massive sell-off in equities, particularly in Europe which is more linked into the global cycle. (See Table 1 at the bottom of p. 1 for more details).

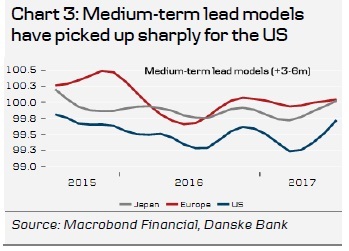

Looking beyond North Korea and assuming that the situation does not escalate, the world economy is looking strong. Our quantitative business cycle model, MacroScope, signals that the global recovery will remain intact in H2 and that the US economy is gaining speed (see Chart 3). This is positive for equities, especially for the US. The positive cyclical outlook for the US also supports our view that US yields will head higher in coming months. In terms of EUR/USD, we expect the recent sharp move higher to fade heading into the Jackson Hole conference 24-26 August and the ECB meeting on 7 September. We believe the ECB president Mario Draghi will be cautious in not sounding too confident given the recent sharp rise in the effective EUR which has risen to its highest level since Q4-2014. We forecast EUR/USD at 1.17 in 1M and 3M before the next leg higher towards 1.22 in 12M.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.