Dollar coming under pressure as risk appetite falls

Market Overview

The bullish outlook for the dollar is coming under pressure as a reduction in risk appetite and further concerns over tax reform are weighing on Treasury yields. The yield curve flattening resumed again with the 2s/10s spread down at 67 basis points and whilst this flattening is nothing new, it has been a sharp fall in the 10 year yield which is hitting the dollar. Concerns over tax reform continue to feature and are helping to flatten the curve, with a fall at the longer end key. Having been previously above 2.40% the 10 year has dropped back to 2.35%. The biggest reaction has been seen on EUR/USD which has gained the most in almost five months as the yield spread of German Bunds and US Treasuries has tightened. This drop on the US 10 year is also impacting on Dollar/Yen which is being dragged lower on the positive correlation again. The yen strength is coming as markets are taking on less risk amidst corrections on equity markets which are concerned over the implications of a flattening yield curve. Positive Japanese growth data overnight has also helped to bolster the yen.

Wall Street closed lower on the session but way above the intraday lows however there is a corrective theme developing now. The S&P 500 fell -0.2% to 2579, whilst Asian markets were also broadly weaker (Nikkei -1.6%). European markets are again starting the session on the back foot. In forex, there is a dollar weakness that continues to come through after yesterday’s declines, whilst the Aussie dollar is the chief underperformer after weaker than expected Australian wage growth overnight questioned the RBA’s expectation of wage growth. In commodities the reduction in risk appetite is supportive of gold. However there is also a decline seen on the oil market after the EIA questioned the expectation of global demand growth yesterday, with a forecast supply glut of 600,000 barrels per day in Q1 2018.

There are a number of key tier one data releases for markets to move on today. Starting in the European morning with UK unemployment at 0930GMT which is expected to remain at 4.3%, however the main focus will be on the average weekly earnings which on an ex-bonus basis is expected to improve marginally to +2.2% (from +2.1%). With the UK CPI data coming in flat and below estimates yesterday there is a chance for the size of negative real wages to decline. However the main focus will be in the US tier one data with US CPI at 1300GMT. The headline CPI is expected to drop back to +2.0% (from +2.2%) with core CPI expected to stay at +1.7%. It is unlikely that this would do little to help the flattening US Yield curve. There is also US Retail Sales at 1330GMT which are expected to grow by +0.2% for the month on an ex-autos reading (last month +1.0%). The New York Fed Manufacturing is also at 1330GMT and is expected to remain strong at +26.0 although this is slightly below last month’s +30.2. The EIA oil inventories are at 1530GMT and are expected to show last week’s surprise crude stocks build may have been a one off, with a drawdown of -3.1m barrels expected (+2.2m barrels last week). Distillates are also expected to drawdown by -1.8m barrels (-3.4m last week) with gasoline expected to drawdown by -1.5m barrels (-3.3m barrels).

Chart of the Day – AUD/USD

Having previously highlighted the key support around $0.7620 which was creaking on the Aussie dollar and looking ready to give way. The market withheld the pressure last week but overnight on the disappointing Australian wages data, the support has now given way. The support was already breaking early this week but without a closing breach. Unless the bulls stage a significant recovery into the close this looks to be a decisive breach. This closing breakdown would come as the momentum indicators all remain in negative configuration but also with downside potential with the RSI falling in the mid-30s. Turning back from $0.7695 last week continued the sequence of lower highs which left key resistance at $0.7730 and continues a downtrend. Rallies subsequently remain a chance to sell, with resistance now $0.7620/$0.7650. The next supports to test come in at $0.7560 and $0.7530 but a retreat to $0.7500 is likely in due course. The hourly chart unwinding moves into 50/60 on the hourly RSI are a chance to sell.

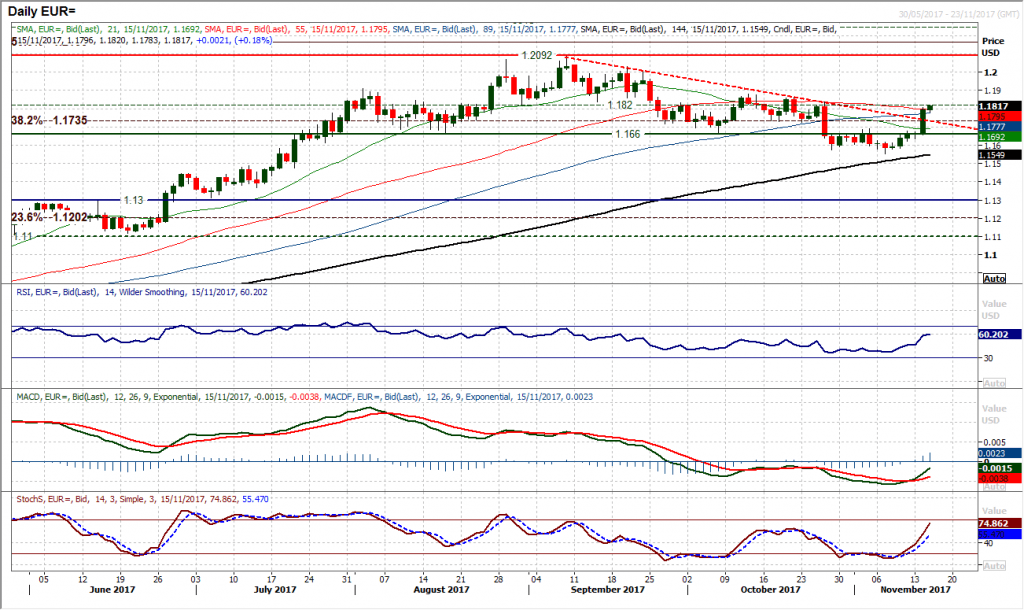

EUR/USD

The euro staged a significant rally yesterday, rising around 130 pips on the day, posting the largest one day gain since late June. The move has significantly changed the outlook too, breaking a two month downtrend. However, most of all, this now begins to seriously question the head and shoulders top pattern. The RSI has risen to its highest level since mid-September whilst the MACD and Stochastics are advancing strongly. The reaction today could tell us whether there is something sustainable in this rally. Another positive close today would suggest so. Initial resistance is $1.1820 with $1.1880 key. Support is now $1.1730/$1.1740.

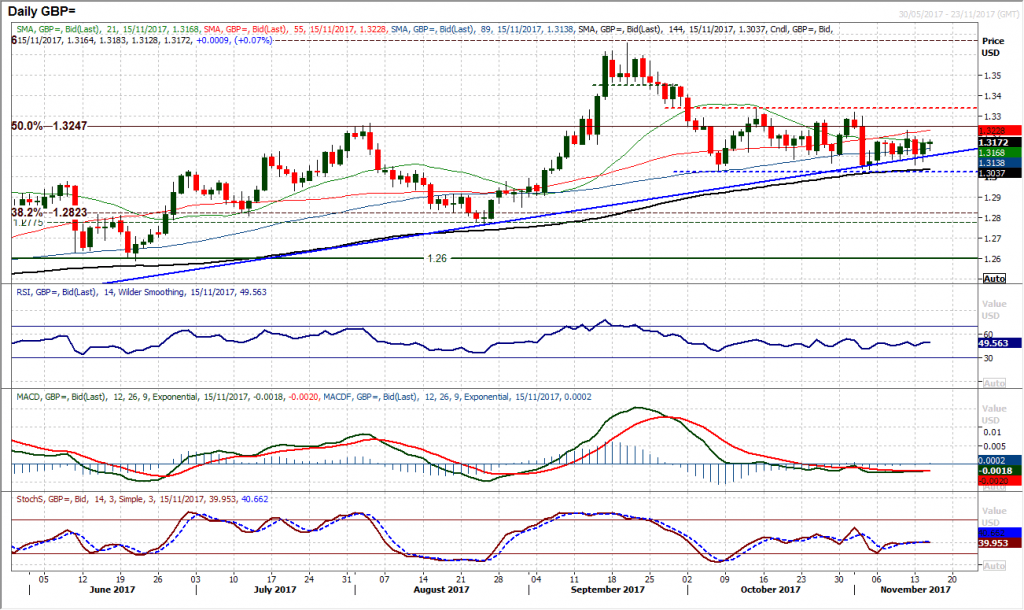

GBP/USD

The market has rebounded again to close above the long term uptrend support. This maintains the range support between $1.3025/$1.3335 and the series of mixed signals continues. There is still very little to really be gleamed from the daily momentum indicators although there is still the slightest of negative biases which suggests an ongoing gravitation towards the range lows. The hourly chart shows a near term pivot at $1.3130 is a basis of support initially whilst yesterday’s spike high at $1.3185 is now resistance under another old pivot at $1.3230. Hourly indicators suggest continuing to play the range and using the classic overbought/oversold signals of the hourly RSI to do it.

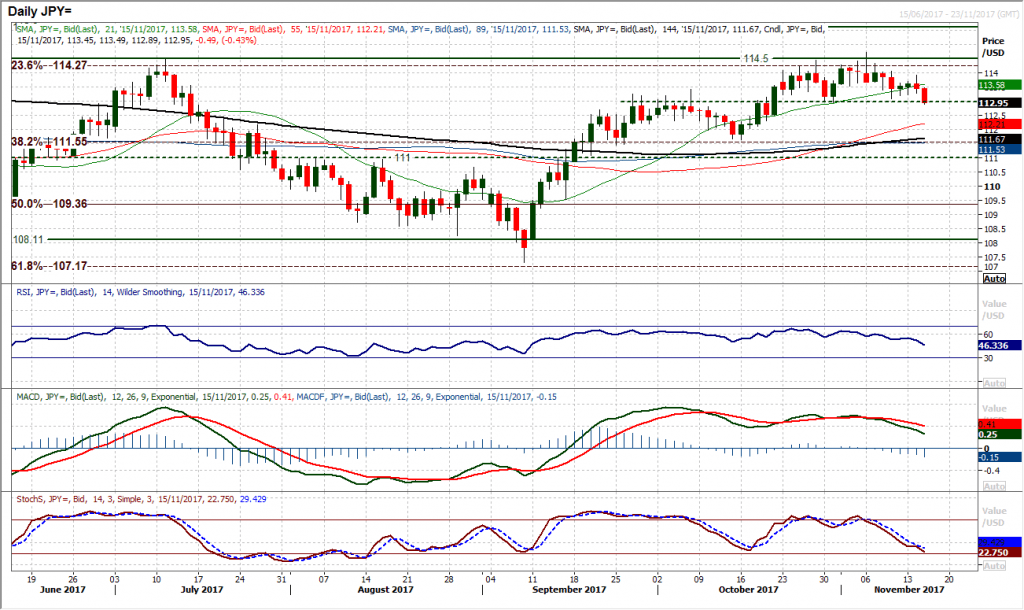

USD/JPY

The weakening dollar and positive Japanese growth data overnight have increased the downward pressure on Dollar/Yen. Momentum has been deteriorating in the last couple of weeks and the prospects of a near term top pattern are growing. The support at 112.95 has been key recently but is coming under increasing pressure. Having bounced from 113.08 last week, yesterday’s negative candle has been exacerbated overnight and the market is having another look at 112.95 again. A closing breach would complete a three week top pattern and imply around 150 pips of further correction. That would mean a retreat to the 38.2% Fibonacci retracement at 113.55. Yesterday’s high at 113.90 is now near term key resistance. The momentum indicators are now corrective with the RSI falling below 50, MACD lines accelerating lower and the Stochastics negatively configured. The hourly chart reflects the negative configuration and that rallies are a chance to sell now.

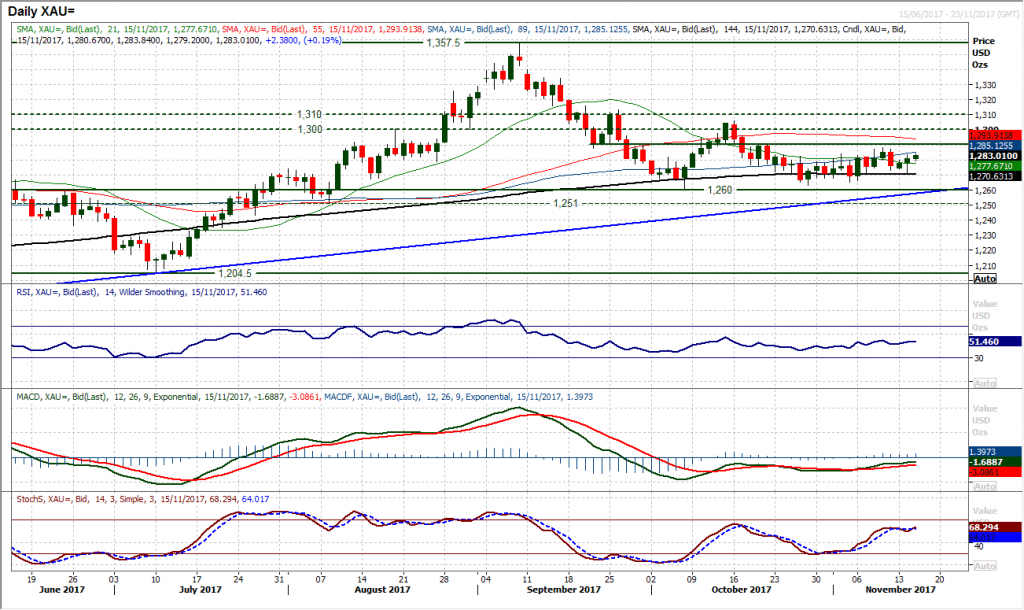

Gold

There has been a subtle reduction in risk appetite in the last session that has enabled another bounce on gold. However, so far the move is well contained within the recent range. A second consecutive positive session has left support at $1270.50 and it will be interesting to see if the bulls can now start to pressure the resistance again. In this consolidation there is a mild trend of higher lows and higher highs and this could mean a pull towards the $1290 resistance. Momentum indicators are mildly drifting higher but on a medium term basis are simply unwinding negative configuration. Realistically, the RSI needs to move into the 60s and MACD lines sustainably above neutral to suggest the bulls are making a valid attempt at a recovery. The long term pivot at $1300/$1310 remains key resistance overhead. The hourly chart suggests move needs to be done with indicators still with ranging configuration.

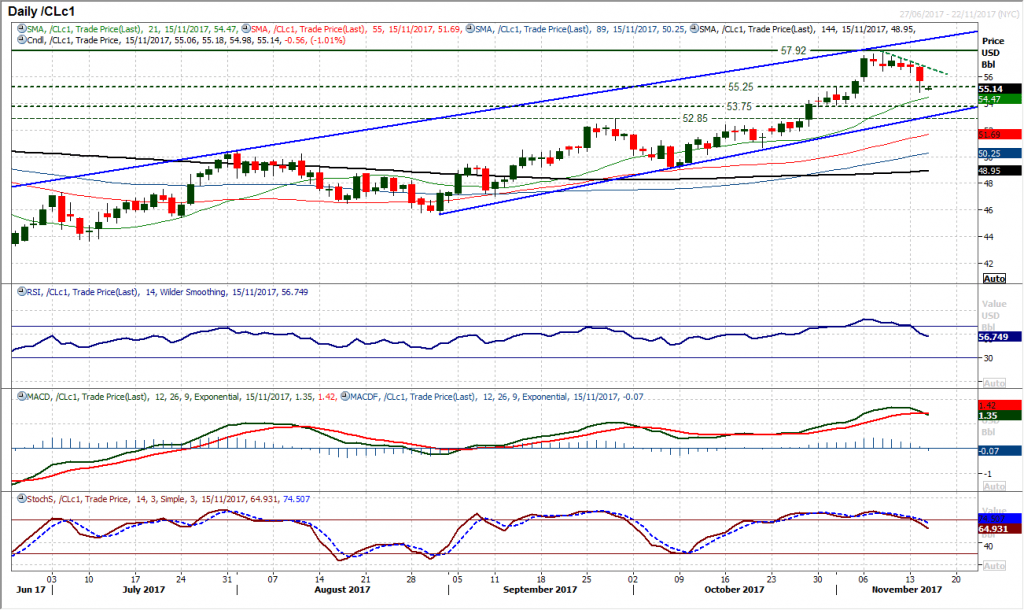

WTI Oil

The consolidation has turned into a correction as oil has gone into reverse. A strong bear candle completed yesterday has decisively broken below $56.40 to pull the market below the old 2017 breakout of $55.25. The market is now in correction mode and the momentum indicators are flashing warning signs that suggest further downside could be seen now. The RSI has crossed back below 70 in a basic sell signal, whilst the MACD and Stochastics have also both completing crossover sell signals. The market is in retreat within an uptrend channel, the bottom of which comes in around $53 today. However the breakout supports between $53.75/$55.25 will likely be seen as an area where the bulls will look to form support again so will be interesting to see how the market reacts here.The old support at $56.30/$56.40 is now initial resistance.

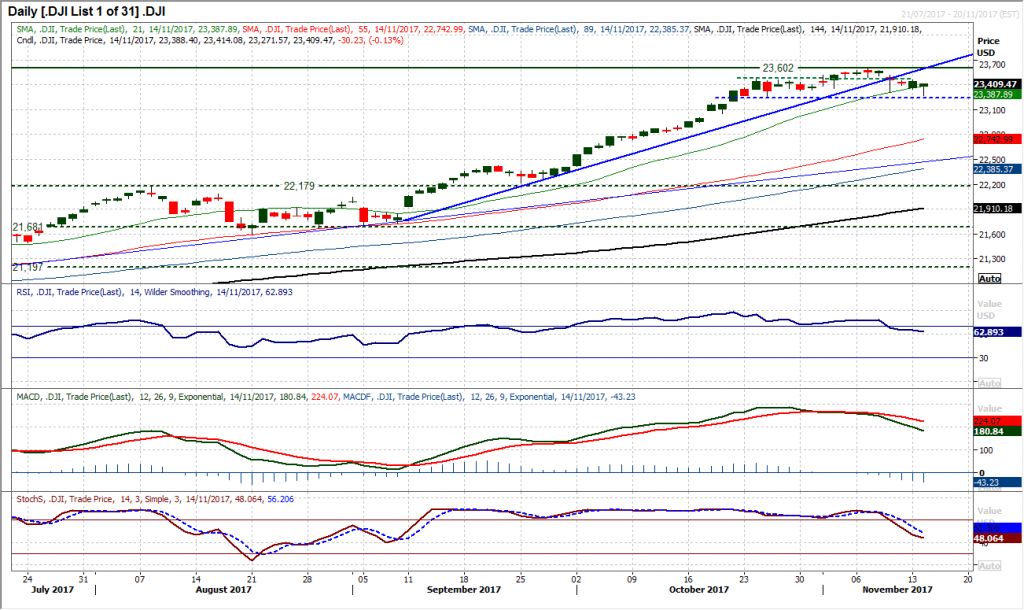

Dow Jones Industrial Average

The Dow is starting to form a new trend lower. Having topped out last week at 23,603 the market is now forming lower highs and lower lows. The rebound candle on Monday has left resistance of a lower high at 23,461 and support is being tested. An intraday breach of Thursday’s low at 23,310 now means that the market is eyeing a challenge of the key near term support at 23,251. However it is interesting to see that initial selling pressure during recent sessions is tending to be bought into the close. This could be a case of the bulls still hanging on, so the configuration of daily candlesticks could be increasingly telling now. This is the point at which a break of 23,251 would complete a near term top pattern that would imply a further 350 ticks of further correction. The momentum indicators are already into correction mode, with the RSI below 60 at a 9 week low, whilst the MACD and Stochastics are both accelerating lower. Rallies are now being seen as a chance to sell. Initial resistance is at 23,397 with a pivot now at 23,485. Below 23,250 the support is at 23,173 and then 23,058.

Author

Richard Perry

Independent Analyst