“Default is unthinkable”: The US will raise the debt ceiling come hell or high water

Outlook: We are all driving in the dark without headlights, lacking hard information about the political scene and trying to read the Fed’s mind. That puts today’s Fed minutes on the map even though there is far too much water under the bridge for the sentiments at the last meeting to be relevant now. The last time out, Fed chief Powell seemed to favor a pause for the June meeting. Chandler cleverly speaks of a ”skip” instead of a pause, or a “hawkish hold.”

Reuters’ Dolan reports that “Fed hawks are in full voice and senior bankers, such as JPMorgan boss Jamie Dimon, this week mulled risks that rates could get above 6% before peaking, a level some had feared they might reach before the banking stress hit in March. ‘Five percent's not high enough for Fed Funds - I've been advising this to clients, and banks, you should be prepared for six, seven,’ Dimon said on Monday.

Monday? This is out of date. Further, “Rates futures are not in the 6% range yet by any stretch, but they put a one-in-three chance of another quarter-point Fed rate hike next month and have priced out the likelihood of multiple rate cuts by year-end.”

We think this is wrong, a real surprise from Dolan. The CME FedWatch tool shows the cumulative probability of Fed funds less than today by the Dec meeting at a combined 80.8%. They have not given up rate cuts by year-end by any means. The probability of one more hike by December is a mere 3.2%. This is up from zero a week ago.

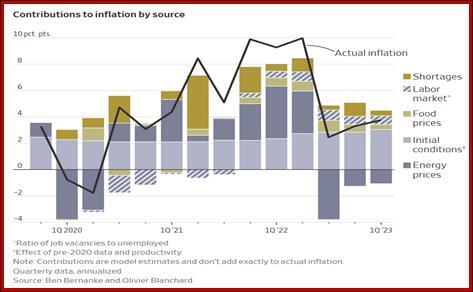

Ahead of the PCE inflation data on Friday, yesterday former Fed chair Bernanke and IMF chief economist Blanchard released their report on inflation. It’s titled “What Caused the U.S. Pandemic-Era Inflation?,” it contains a model, and it runs to 50 pages. Bloomberg and the WSJ wrote lengthy pieces on it already and more will surely be coming.

In a nutshell, the WSJ Fed-watcher Ip writes “Pandemic-related supply shocks explain why inflation shot up in 2021. An economy overheated by fiscal stimulus and low interest rates explain why it has stayed high ever since. The conclusion: For inflation to fade, the economy has to cool off, which means a weaker labor market.

… “That stimulus wasn’t the inflation culprit it is often made out to be doesn’t entirely absolve the Fed and Biden. Arguably, they should have anticipated supply disruptions would amplify the risks of stoking demand…

“Bernanke and Blanchard conclude that because inflation today reflects a too-hot labor market, the solution is to cool it off. To bring inflation back to the Fed’s target, they estimate unemployment would have to rise above 4.3% from its current 3.4% assuming vacancies remain difficult to fill. But, they say, inflation could drop without a significant increase in unemployment if the ease of hiring returns to prepandemic norms. The good news: There are tentative signs that is happening.”

As we have been harping on for some time, making the labor market the center of things is conventional, old-fashioned thinking and neglects to factor in new conditions like the gig economy and demographics that no economist has modelled before. Even so, the B&B model estimate of 4.3% unemployment is not all that sizeable. It’s nowhere near the 6-7% that some economists have said might be needed. This is, indeed, good news.

Forecast: The US will raise the debt ceiling come hell or high water and default is not going to happen. We may have to wait until votes next week to get the outcome, but that will be the outcome. As former TreasSec Rubin said his day, “Default is unthinkable.”

Therefore, the doom-and-gloom crowd that undervalues Biden’s insider capabilities are in for a comeuppance when yields retreat and the stock market rallies. Pres Biden is simply smarter and saner than the Republicans and starts off with a set of far bigger and more important arguments, plus the nuclear arrow in his quiver of the 14th Amendment. As Bloomberg’s Authers notes today, aside from credit default swaps, there is no evidence markets believe in default. US equities kept on trucking until yesterday. “Investors are treating the whole distasteful Washington spectacle as political theater that can be safely ignored.” Hilariously, once the 2011 debt ceiling issue was resolved and after the credit agencies downgraded the US rating, “Treasuries enjoyed the most counterintuitive rally in history. The news that they were no longer AAA-rated prompted investors to take sanctuary — in Treasuries. The 10-year Treasury yielded more than 3.0% just days before the ceiling was raised. By October, the yield had settled below 2.0%.”

Also, “Rising yields show that investors think the chances of a soft landing are improving, and that regional banks’ problems will not prove fatal to the economy. If the Treasury were issuing debt as usual, rather than resorting to desperate measures to push back the X-date, yields might be even higher.”

A genuine unknown is whether the Fed may skip the June hike but not the trajectory of hikes after that, and today’s minutes are not going to answer that question. On the whole, we suspect that Bullard and Company, aka the hawks, are going to prevail in the longer run and Fed funds can go up another 25 bp (at least) before year-end, regardless of the PCE inflation read on Friday. This is not yet priced in to Fed funds futures and offers real dollar support when the lightbulb comes on. Remember that we get another Atlanta Fed GDPNow on Friday, too.

Bottom line, we can’t find any reasons to sell dollars.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat