DAX ticks lower, risk appetite under pressure after IMF forecasts

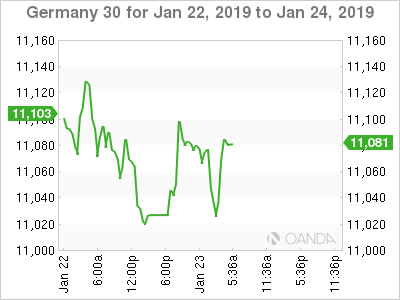

The DAX index has posted small losses in the Wednesday session. Currently, the index is at 11,078, down 0.10% on the day. In economic news, the eurozone will release consumer confidence, which is expected to post a second straight decline of -6 points. On Thursday, Germany and the eurozone release PMI reports and the ECB will set interest rates and ECB President Mario Draghi will follow with a press conference.

With the global trade war continuing to take a bite out of the eurozone economy, it is no surprise that growth forecasts for 2019 have been revised downwards. On Tuesday, the International Monetary Fund lowered its global and eurozone growth forecasts. In October, the IMF projected global growth of 3.7% percent, but this has been revised to 3.5 percent. IMF head Christine Lagarde said that the world’s economy continues to expand, but “it is facing significantly higher risks”. The forecast for Germany was lowered to 1.3%, down from 1.9% in December. The IMF said that German growth had been dampened by weak consumer demand and lower factory production, notably in the car industry. The grim forecast follows a soft Chinese GDP, which dropped to 6.6% in 2018, its weakest level since 1990.

With dark economic clouds on the horizon, the ECB will is unlikely to make any moves at today’s policy meeting. Growth forecasts have been revised lower for the three largest economies in the bloc (Germany, France and Italy). The U.S-China trade war, which shows not signs of being resolved anytime soon, has taken a bite out of the eurozone export and manufacturing sectors have slowed. If the trade war worsens or the U.S. economy slows down in 2019, the eurozone could lapse into a recession. Given these weak economic conditions, the ECB, which finally terminated its massive stimulus program last month, is unlikely to raise interest rates before the fourth quarter of 2019. Just a few months ago, analysts were predicting a rate hike in the third quarter. Lower rates should be bullish for the equity markets, which will be more attractive to investors than the bond markets.

Economic Calendar

-

10:00 Eurozone Consumer Confidence. Estimate -6

-

3:15 French Flash Manufacturing PMI. Estimate 50.0

-

3:15 French Flash Services PMI. Estimate 50.6

-

3:30 German Flash Manufacturing PMI. Estimate 51.6

-

3:30 German Flash Services PMI. Estimate 52.2

-

4:00 Eurozone Flash Manufacturing PMI. Estimate 51.5

-

4:00 Eurozone Flash Services PMI. Estimate 51.5

-

7:45 ECB Main Refinancing Rate. Estimate 0.00%

-

8:30 ECB Press Conference

Previous Close: 11,090 Open: 11,036 Low: 11,008 High: 11,085 Close: 11,078

Author

Kenny Fisher

MarketPulse

A highly experienced financial market analyst with a focus on fundamental analysis, Kenneth Fisher’s daily commentary covers a broad range of markets including forex, equities and commodities.