DAX rally takes pause on China concerns

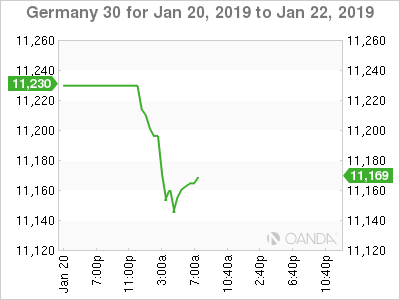

The DAX index has lost ground in the Monday session. Currently, the index is at 11,154, down 0.53% on the day. In economic news, there are no major German or eurozone releases. German PPI declined by 0.4%, the first decline since February 2018. On Tuesday, Germany releases ZEW Economic Sentiment.

The DAX has jumped out of gates in 2019, climbing 6.4% in January, as risk appetite remains strong. However, the index has started the trading week with losses, as investors gave a thumbs-down to soft GDP data out of China. The economy grew 6.6% in 2018, marking its lowest level since 1990. GDP for the fourth quarter dipped to 6.4%, compared to 6.5% in the previous quarter. The soft GDP release comes on the heels of soft trade and manufacturing data, as China is experiencing a slowdown due to the ongoing U.S-China trade war. The Trump administration has threatened further tariffs if a deal is not reached by March 1, but the markets are hopeful that the sides will reach an agreement. A second round of negotiations between U.S. and Chinese officials is scheduled for the end of the month in Washington. Chinese officials will be under pressure to show more flexibility in the talks, in order to stem the economic bleeding.

Is the eurozone headed for a recession? Growth forecasts have been revised lower for the three largest economies in the bloc (Germany, France and Italy). The U.S-China trade war, which shows not signs of being resolved anytime soon, has taken a bite out of the eurozone export and manufacturing sectors have slowed. If the trade war worsens or the U.S. economy slows down in 2019, the eurozone could lapse into a recession. Given these weak economic conditions, the ECB, which finally terminated its massive stimulus program last month, is unlikely to raise interest rates before the fourth quarter of 2019. Just a few months ago, analysts were predicting a rate hike in the third quarter. Lower rates should be bullish for the equity markets, which will be more attractive to investors than the bond markets.

Economic Calendar

Monday (January 21)

-

7:00 German PPI. Estimate -0.1%. Actual -0.4%

-

11:00 German Buba Monthly Report

Tuesday (January 22)

- 10:00 German ZEW Economic Sentiment. Estimate -18.8

Author

Kenny Fisher

MarketPulse

A highly experienced financial market analyst with a focus on fundamental analysis, Kenneth Fisher’s daily commentary covers a broad range of markets including forex, equities and commodities.