Daily Market Update

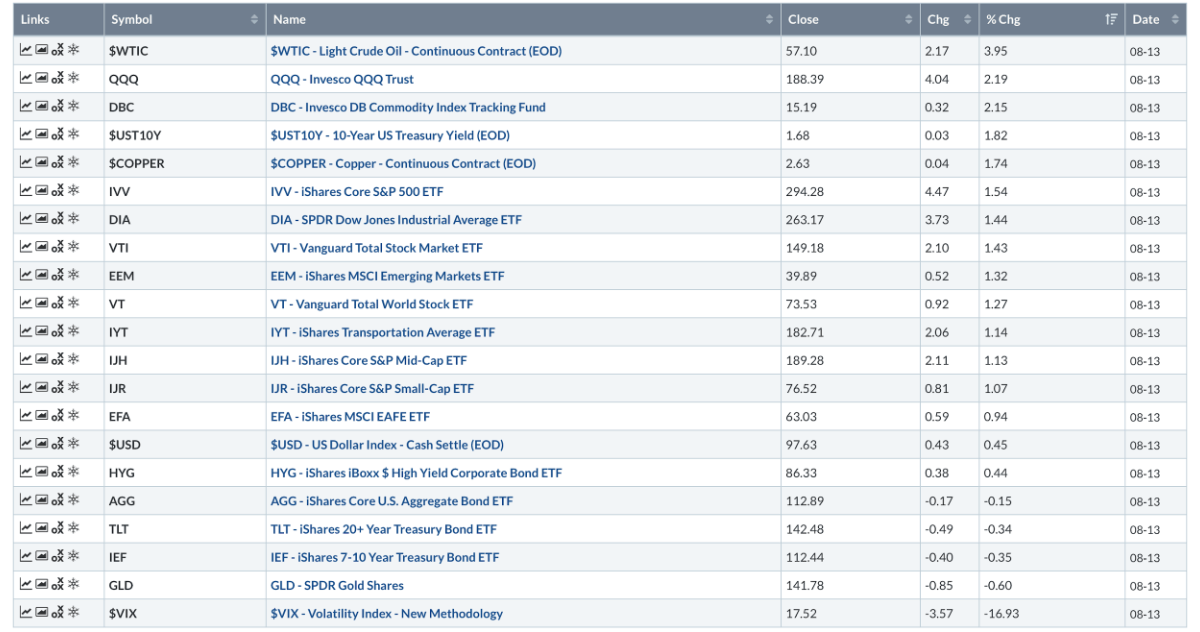

Market Recap: Stocks rallied yesterday as news was released that tariffs were going to be delayed against China, and that certain goods would be removed from the list. The S&P 500 (IVV) moved up by 1.54%. Oil was the top gainer, up 3.95%. The U.S. Dollar was up 0.45%. U.S. 10-year yields rose 3 basis points.

Economic Data: Inflation ticked up to 1.81% year-over-year. Inflation has slowed considerably from the peak in 2018.

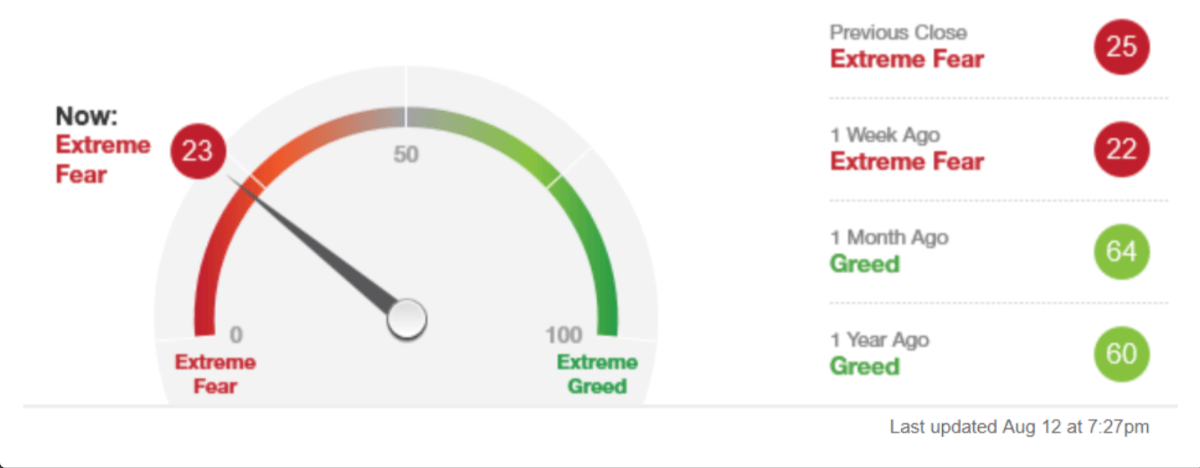

Sentiment: The CNN greed and fear index is still showing fear. This does not mean that markets can’t continue to drop. However, sentiment has shifted quite pessimistic after only a short correction in equities markets.

Another Inversion: The commonly watched (although not our favorite) yield curve in the U.S. inverted this morning. The 2-year yield is higher than the 10-year yield now. This means that the Fed remains too tight and will need to continue to cut interest rates.

-637013824552470196.png)

Futures Summary:

-637013825163880175.png)

News from Bloomberg:

China posted the weakest industrial output growth in 17 years in July, while retail sales and fixed-asset investment rose less than forecast. Output expanded 4.8%, missing the 6% estimate. In a conciliatory move toward the U.S., the People's Bank of China set the daily yuan reference rate stronger than expected.

It's not looking good for Germany either. The economy shrank last quarter, piling pressure on Angela Merkel to consider fiscal stimulus as factories were hit by the trade war and exports slumped. GDP fell 0.1% from the previous period, matching forecasts. Merkel yesterday hinted her reluctance to respond is softening. In the wider euro area, second-quarter growth was confirmed at a tepid 0.2%.

As for the trade war, Chinese negotiators will still visit Washington in September, people familiar said. But they're unlikely to make concessions before Oct. 1, the 70th anniversary of the People's Republic, one person said. Optimism over the delayed tariff hikes rings false to Morgan Stanley. A way to lower existing levies is elusive and the new ones will probably still be imposed, its strategists wrote.

U.S. equity-index futures fell and Treasuries gained as signs of a global slowdown overshadowed trade optimism. The U.S. 10-year yield fell below the two-year rate for the first time since 2007. The dollar was steady as the onshore yuan rallied with the yen. WTI crude fell more than 1%, while most industrial metals declined. Gold was little changed.

Hong Kong's airport returned to normal after a night of chaos in which protesters beat and detained two suspected infiltrators. The airport got an interim injunction barring further protests. China's local liaison office blasted the violence as akin to terrorism, fomenting fears that it may send in troops.

Author

Clint Sorenson, CFA, CMT

WealthShield