D-Day for the Fed

What to expect from the Fed statement today?

Note: There is no press conference and the Fed minutes in a couple of weeks will provide fuller details.

Today’s statement is likely to provide the following signals on three issues:

1. Caution ahead

Recent rhetoric from many of the voting members would suggest that on the U.S economic outlook that they are more cautious and a tad less confident about the strength of the economic recovery, pointing to headwinds to both higher growth and inflation.

The ‘big’ dollars recent demise is expected to help out on both accounts, but not enough to offset the concerns about Trumponomics (pro-growth policies that include tax reform and infrastructure spend).

2. Rates – to maintain a tightening bias

Despite the cautious tone, the Fed is not prepared to abandon its tightening bias theme any time soon – expect them to reiterate at least one more hike in 2017 (consensus expects December). But, this is expected to be quantified – more sensitive and more data dependent.

3. Balance Sheets: Prepping the market.

The Fed will continue to prepare markets for the beginning this year of a gradual shrinkage in their balance sheets through a reduction in its holdings of U.S Treasury and mortgage securities.

Expect them to downplay the potential impact on the market by signalling that the reduction will be very slow.

1. Stocks mixed results

Global equity markets are mixed after yesterday’s lackluster session with the focus on today’s Fed statement.

In Japan, strong earnings supported the Nikkei (+0.5%), rising for the first time in four sessions, but gains were capped by profit taking ahead of Fed decision.

In Hong Kong, shares rallied despite profit taking, helped by energy stocks. The benchmark Hang Seng index finished +0.3% higher, while the Hang Seng China Enterprises Index was up +0.5%.

In China, blue-chip stocks fell for a second consecutive day overnight on investor fears of further regulatory tightening. The blue-chip CSI300 index fell -0.4%, while the Shanghai Composite Index was little changed, up +0.1%.

In Europe, indices trade higher following generally positive earnings out of Europe. The Swiss SMI, FTSE and CAC are outperforming.

U.S stocks are expected to open little changed (+0.1%).

Indices: Stoxx600 +0.5% at 382.8, FTSE 0.6% at 7476, DAX +0.4% at 12306, CAC-40 +0.6% at 5190, IBEX-35 0.3% at 10550, FTSE MIB 0.2% at 21509, SMI +0.7% at 9002, S&P 500 Futures 0.1%.

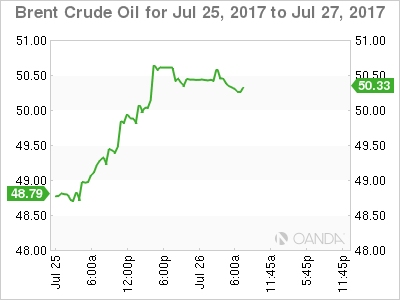

2. Oil prices are firmer on optimism of declining stocks

Oil prices again firmed overnight, holding atop of their two month highs hit on Tuesday, on expectations of a drawdown in U.S stocks and as a rise in shale oil production shows signs of slowing.

Brent crude has rallied +41c, or +0.8%, to +$50.61 a barrel, after rallying more than +3% in yesterday’s session. U.S West Texas Intermediate futures have climbed +49c, or +1%, to +$48.38 a barrel.

Data from the API yesterday showed that U.S crude stocks fell sharply last week as refineries boosted output, while gas inventories increased and distillate stocks decreased.

Crude inventories declined by -10.2m barrels in the week ending July 21 to +487m, compared with expectations for a decrease of -2.6m barrels.

Prior to yesterday’s inventory report, crude prices had been supported by Monday’s OPEC announcement by the Saudi’s that they would limit its crude exports to +6.6m bpd next month, almost -1m bpd below the levels of a year ago, while Nigeria voluntarily agreed to cap or cut its output from +1.8m bpd, once it stabilizes at that level – up to now, Nigeria had been exempt from the output cuts.

However, current price levels may be soon capped, as it’s a level that could attract increased U.S shale oil production.

Next up is this morning’s EIA inventory report at 10:30 am EDT. Consensus is looking for a drawdown of -3.3m barrels.

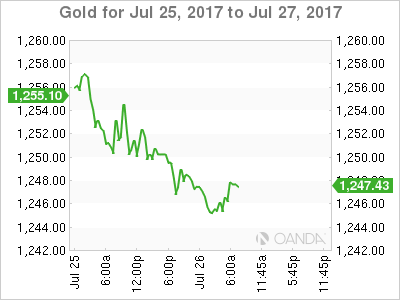

Gold prices are steady (fell -0.1% to +$1,246.94 per ounce) as investors await U.S Fed policy statement. The market is looking for any comment regarding inflation for directional guidance.

3. Yields await Fed

U.S government bonds pulled back for their second consecutive session yesterday, signalling an end to its recent rally amid continued focus on a possible shift by G7 members towards a tighter monetary policy.

Putting further pressure on prices is a large volume of new Treasury notes being sold this week, and the Fed’s pending policy statement (2:00 pm EDT). U.S policy makers are not expected to hike rates, but the market is looking for any change in tone from policy makers, especially since they have leaned towards being a little ‘dovish’ in recent weeks. U.S 10-year yield is trading atop of +2.31%.

Note: The U.S Treasury will sell +$34B 5-year notes today and +$28B 7-year notes Thursday.

Elsewhere, Germany’s 10-year Bund yield has fallen -2bps to +0.55%, while U.K Gilts yield has declined -3 bps to +1.232%.

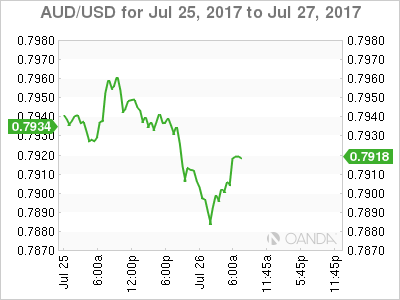

Down-under, Australia’s Q2 CPI data overnight showed that core inflation remains well below the +2-3% targeted by the RBA, which suggests that rates should be kept on hold for some time. Aussie futures suggest that there is +54.5% chance that the RBA will keep rates on hold until May 2018.

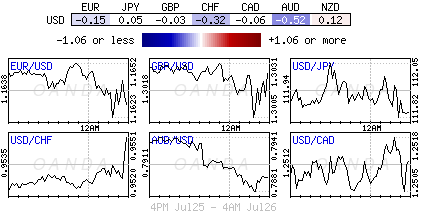

4. Dollar tame ahead of Fed statement

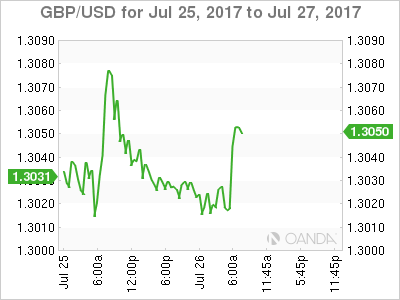

Sterling (£1.3016) has dipped after data this morning showed the U.K. economy expanded at a meager pace (see below). EUR/GBP trades at €0.8928.

Australia’s muted inflation is being attributed to weaker wages and lower fuel costs. The AUD has fallen -0.5%, trading atop of its overnight lows of €0.7892. RBA Governor Lowe warned that there could be financial stability risks from “additional easing.” He also reiterated preference for a weaker currency.

The EUR has inched lower in early U.S trade, down -0.14% to €1.1630. On the release front, there are no events out of the eurozone. Markets are waiting for the Fed’s rate announcement.

5. U.K economy posts lackluster growth

Data this morning showed that U.K economic growth remained subdued in Q2, expanding at a +0.3% q/q pace, as weak performances from the manufacturing and construction industries offset an improvement in services.

It’s a slight improvement on the +0.2% growth rate of Q1, but still less than half the pace of growth at the end of 2016.

Note: The headline print was in line with consensus and the data covers the first three-months of the two-year Brexit negotiation period.

On an annualized basis, growth accelerated to +1.2%, from +0.9% in Q1.

Digging deeper, the expansion was driven largely by an improvement in services, which grew +0.5%.

Author

Dean Popplewell

MarketPulse