Czech inflation to hover above the target

Consumer prices maintain solid growth, with persistent core inflation outweighed by softer food price dynamics. Both headline and core inflation may hover close to the 3% upper bound of the tolerance band around year-end, which should foster a hawkish stance by the Czech National Bank. Pro-inflationary scenarios take the stage for now.

Food prices are a drag, while broad price pressures remain

Czech consumer prices rose by 0.5% month-on-month and 2.7% year-on-year in July, according to a preliminary estimate. Annual core inflation is likely to have eased only marginally to a range of 2.7% to 2.8%, which is in line with our view of continued price pressures driven by solid wage growth and consumer spending. Meanwhile, food prices were the main drag for the headline figure, as the surveyed decline in potato prices was recorded in the CPI statistics, as we have suggested. That said, food prices are notoriously volatile during the summer months and hard to predict. In contrast, fuel prices likely drove consumer price growth somewhat more forcefully than we assumed. We must wait for the full CPI breakdown to assess the impact of likely lower electricity prices on the regulated segment of the consumer basket.

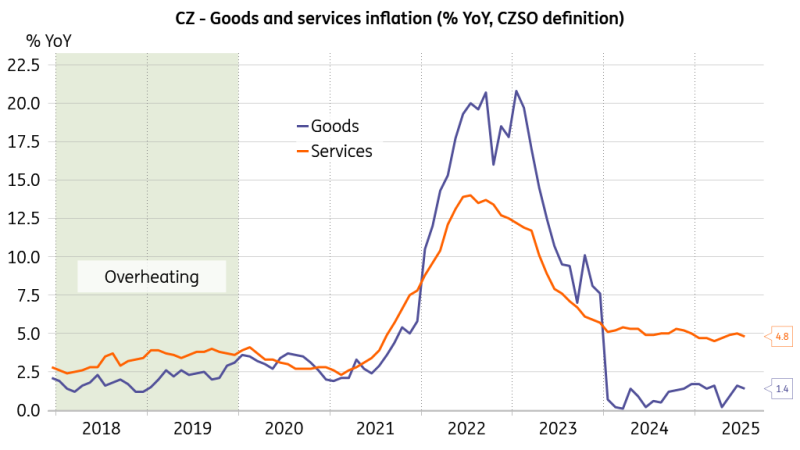

Services inflation is potent and the recovery has just started

Source: CZSO, Macrobond

Annual price dynamics for services eased to 4.8% and for goods to 1.4% in July, both coming in 0.2 percentage points softer than the previous reading. The monthly price increase of 1.4% in the services segment was below the 1.7% average of the preceding three years, providing some hope that prices are at least not accelerating in the carefully watched component of the consumer basket.

No more rate reductions to keep things safe

Still, the preliminary estimate and its limited breakdown confirm our story of a pro-inflationary environment, which holds both headline and core inflation above the inflation target throughout the remainder of the year and underpins the rate-setters' hawkish stance. The reading cements the outlook for policy rate stability on Thursday’s CNB vote and beyond. We are anxiously awaiting the summer CNB forecast to see whether it will introduce a fundamental revamp.

The upcoming CNB forecast will be supervised by the new projection chief, Petr Sklenar. We perceive him as reasonably hawkish and believe that he can accurately read the economy. His mandate also includes overhauling the CNB’s forecasting framework, so we anticipate changes in two key macroeconomic variables: the exchange rate and the policy rate. Specifically, the forecast should no longer persistently imply a depreciating koruna and a declining base rate over the forecast horizon. We will see on Thursday how this plays out, but it may be the case that more time is needed to push ahead with the change.

Our inflation forecast goes up a bit

We revised our own inflation forecast to incorporate the latest data on both foreign and domestic variables into our projection model. As a result, the weaker koruna against the dollar suggests somewhat stronger fuel inflation when looking ahead, as the exchange rate effect is only partially offset by the relatively low Brent crude price. Add the relatively strong monthly CPI dynamic for July published today, and you end up with slightly higher projected headline and core rate profiles for this year and next.

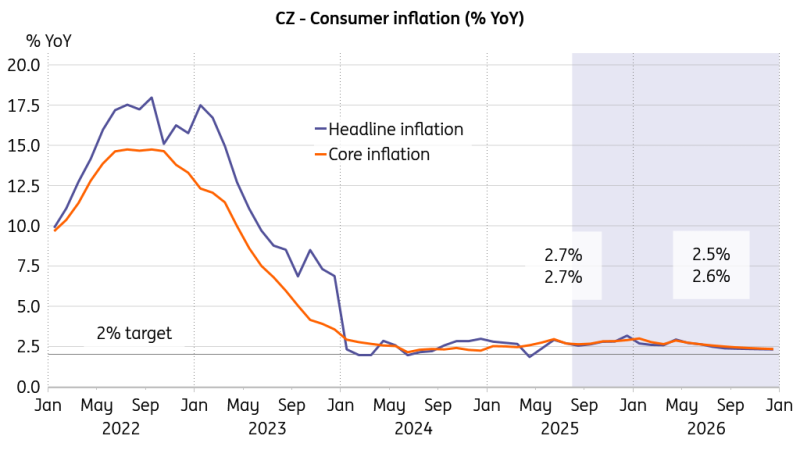

Both headline and core rates to get close to 3%

Source: CNB, ING, Macrobond

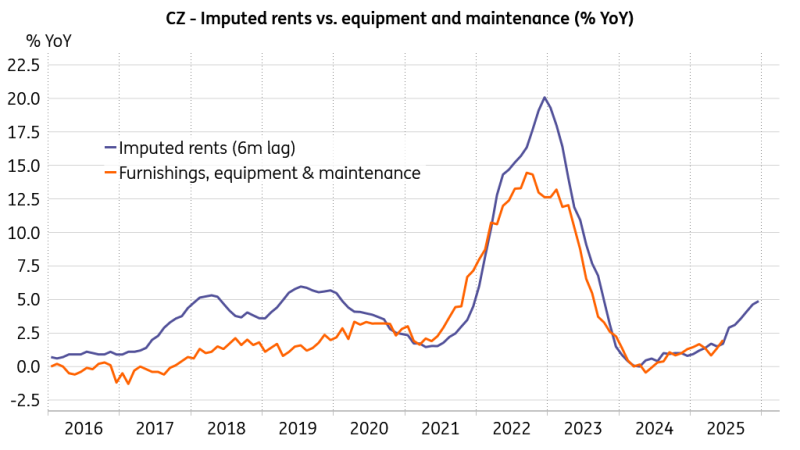

The thing is, there are some almost mechanical upward pressures for core inflation in the pipeline. In conversations with customers, for instance, we came across a very close relationship between two segments of the consumer basket. Look at imputed rents (No. 4.2 basket item) vs. equipment and maintenance (No. 5.0 basket group): if you take a six-month lag of the first series, you see that the second is set to follow suit. That’s only an eyeball test on yearly dynamics; however, if you compute cross-correlations on a monthly growth basis, you end up with a pretty significant relationship between the two again.

Almost a mechanical connection

Source: CZSO, Macrobond

Further statistical inquiry confirms that the two series are cointegrated, showing strong long-term common dynamics. Granger causality exploration clearly confirms that changes in imputed rents precede and can predict changes in equipment and maintenance prices. These two time series simply show a textbook case for this type of strong relationship that would definitely be worth including in econometric exercises. Moreover, there is a straightforward economic reasoning to the relationship: you build more and acquire more properties during a booming housing market, you buy more equipment and request more maintenance, and prices of both rise as demand exceeds supply, at least temporarily. Ergo, the likelihood of even more potent core inflation than in our projection is not negligible.

In any case, we reiterate our two pro-inflationary alternative scenarios: (i) a surge in the Czech property market that fuels core inflation, and (ii) a German economic rebound driven by fiscal stimulus, generating positive spillovers for Czech growth, the labour market, and wage dynamics. While both remain alternative scenarios, it is often prudent to keep a range of possibilities in view.

Read the original analysis: Czech inflation to hover above the target

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.