Czech growth revised slightly upwards, while PMI remains gloomy

September’s manufacturing PMI came in weaker than in the previous month, in line with market expectations. Czech quarterly real GDP growth was revised slightly upward in the second quarter, suggesting no pause in the rebound.

Economic rebound remains intact in 2Q

The aggregate real household income in the second quarter of 2024 declined 0.1% from the previous quarter. Real per capita consumption rose by 0.8% quarter-on-quarter. The savings rate rose 0.3ppt to 18.7%, remaining elevated, as compared to an average savings rate of around 11% in the years before the pandemic. The investment rate of non-financial corporations added 0.6ppt from the previous quarter and reached 26.5% in 2Q24, compared to an average of 26.3% recorded between 2016 and 2019.

The profit rate in 2Q24 was 46.5%, up 0.2ppt from the previous quarter. Total labour costs of non-financial corporations rose by 5.9% year-on-year. The investment rate increased 0.6ppt from the preceding quarter to 26.5%. The estimate of real GDP growth in 2Q24 was revised upwards by 0.1ppt to 0.4% QoQ, yet it remained unchanged in annual terms at 0.6%. This outcome aligns with our base-case scenario of a gradual economic recovery of around 1% for the year as a whole.

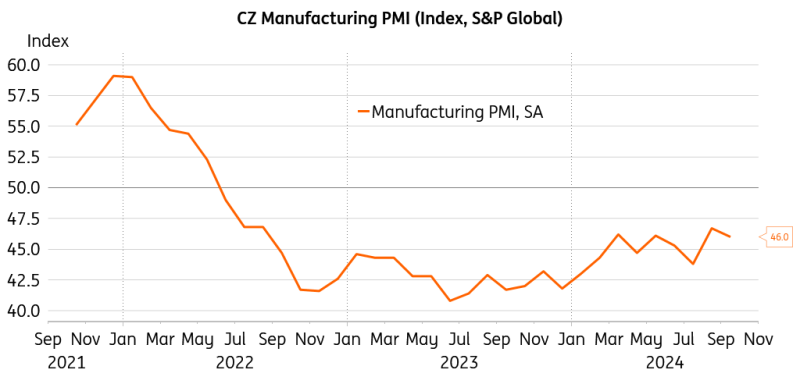

PMI closes 3Q in contraction zone

Czech manufacturing PMI weakened to 46.0 in September, correcting the previous improvement in line with market expectations. It has remained in contractionary territory since mid-2022 though the figures this year are a bit less disappointing than in the previous one. Still, the tepid demand across European trading partners is the foremost hurdle to any expansion. Due to the prolonged challenging environment, the reduction of employees has accelerated to its fastest pace in nearly a year. Output and new orders fell faster than in preceding months, adding to the softening in overall sentiment. Nonetheless, dum spiro spero. Companies have expressed hope when it comes to a rebound in demand going forward.

Less gloomy than in 2023, but still under pressure

Source: S&P Global, Macrobond

Rising transportation costs and longer delivery times due to strikes at ports in Germany are driving overall operating costs higher. Czech manufacturers passed on the increasing costs to end prices in September, increasing selling prices for the first time since June. However, overall producer price inflation has remained moderate due to the intense price competition resulting from the lack of demand.

The dichotomy between solid consumer spending and the underperformance in industry continues. The question is when the reduction in factory employment will trickle down to a tighter aggregate budget constraint and start limiting household consumption expenditures. Given the elevated savings rate, getting the timing right is a challenging task.

Read the original analysis: Czech growth revised slightly upwards, while PMI remains gloomy

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.