Crude oil tumbles as output soars; USD buoyed tax reform optimism

Market Recap

|

Market Recap |

% |

Close Price |

|

USDSEK |

0.88% | 8.4229

|

|

USDCAD |

0.77% |

1.2789 |

|

USDRUB |

0.75% |

59.1962 |

|

GBPUSD |

-0.37% |

1.3393 |

|

Nikkei 225 |

-1.81% |

22,200 |

|

WTI Crude Oil (Jan.2018) |

-2.88% |

55.96 |

-

The Bank of Canada left interest rates unchanged at 1.0%. USDCAD closed 0.77% higher as the BoC communicated a cautious approach towards future rate hikes.

US businesses added 190,000 jobs in November versus an expected 185,000. The dollar index gained 0.25%, closing at 93.610. -

Bitcoin surged to new highs yesterday, closing at $13,347. An increase in demand by Koreans, who have been paying premiums of around 20%, was believed to have lifted prices higher. In addition, another milestone was reached in the implementation of the lightning network, which smooths the path for instant transactions at close to zero fees.

-

WTI crude oil closed 2.88% lower at $56 a barrel as gasoline stocks rose more than expected. US crude inventories dropped to 5.6 million barrels but output soared for the week ending December 1st. Gold traded down 0.19% to 1,263.37, while copper recovered some of Tuesday’s losses by rising 0.55% to 293.65.

|

Thursday December 7, 2017 CET Time |

Forecast |

Previous | ||

|

09:30 |

GBP |

Halifax House Prices (Nov; MoM) |

0.2% |

0.3% |

|

11:00 |

EUR |

GDP (3Q; QoQ) – Final |

0.6% |

0.6% |

|

14:30 |

USD |

Initial Jobless Claims (Dec 2) |

240K |

238K |

|

16:00 |

CAD |

Ivey PMI (Nov) |

62.5 |

63.8 |

|

17:00 |

EUR |

ECB’s Draghi speaks | ||

We start the day with looking at housing prices in the UK at 9:30 CET. The Halifax index is expected to rise 0.2% month-over-month from 0.3%. The final reading of eurozone’s GDP is expected to remain unchanged at 0.6% quarter-over-quarter and unchanged year-over-year at 2.5%. Initial jobless claims in the US for the week ending December 2nd are forecasted to rise to 240K from 238K.

Canada’s Ivey PMI for November (16:00 CET) is forecasted to fall to 62.5 from 63.8 in October. Draghi closes the day at 17:00 CET by holding a press conference in his capacity as GHOS chair.

The Swedish Krona surrendered gains on Wednesday, and was one of the worst performers after forex investors seemed to have misunderstood comments by Riksbank Deputy Governor Jansson, who said substantial interest rate rises are required to subdue financial imbalances. Jansson said persistent, expansionary policy brings up inflation and said policymakers must not lose sight of inflation expectations. USDSEK was up 0.88% and EURSEK up 0.62%

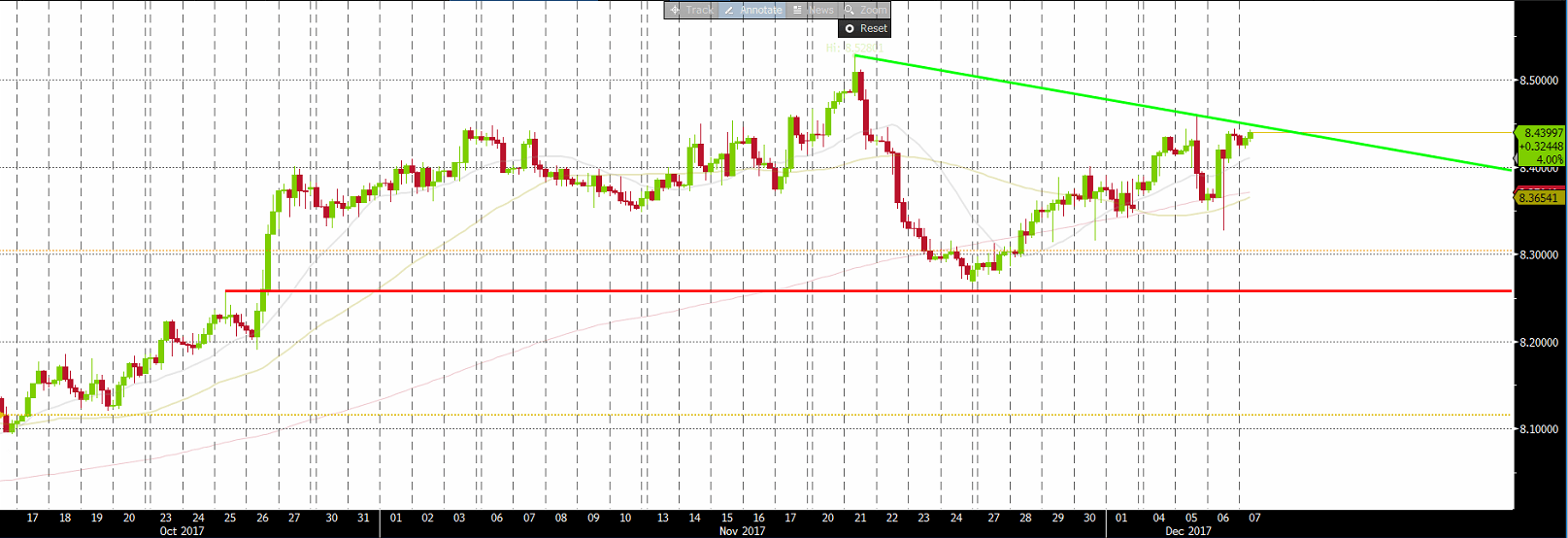

Chart of the day

USDSEK (4-Hour timeframe)

USDSEK plunged to 8.32755 but recovered to 8.44276 near recent highs. The pair is testing a downward trend line off November and December highs, and a break here could see the pair challenge 8.5000 or 8.5280. Intraday support lies at 8.4000 with 8.2580 serving as a key level in the medium-term.

Technical Analysis

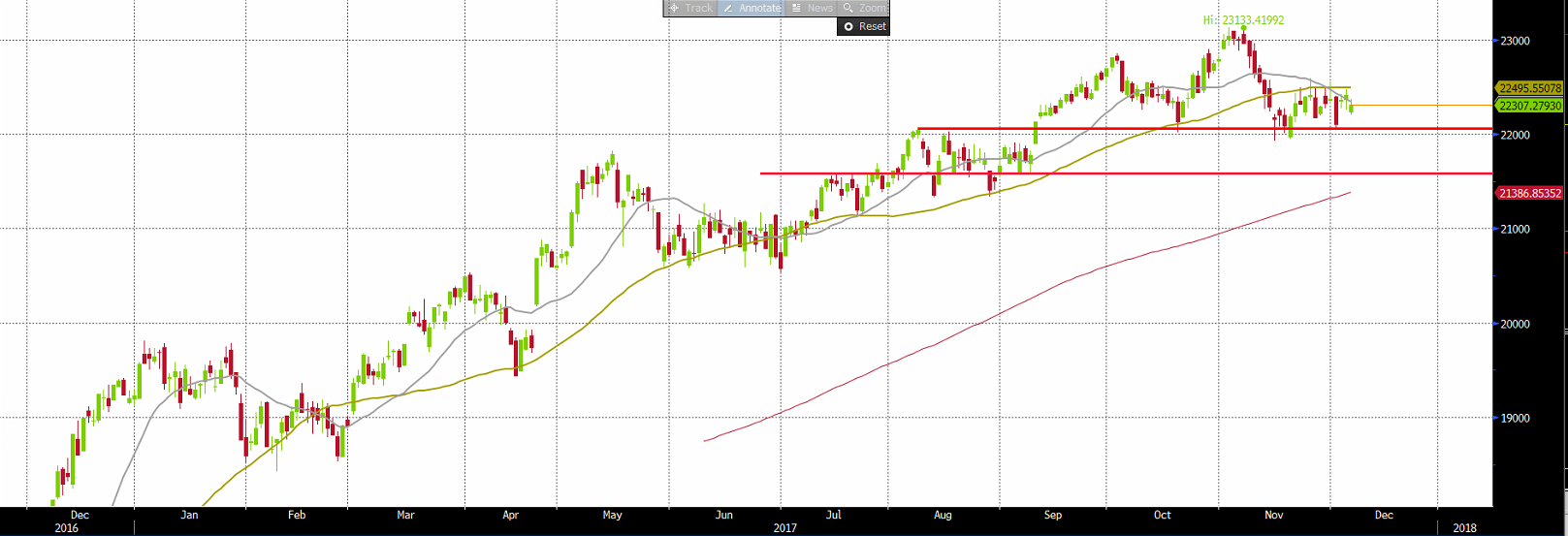

FTSEMIB (Daily timeframe)

FTSE MIB index stays above key support level just above 22000, which could possibly be the neckline of a potential head and shoulders reversal pattern. A break lower would trigger weakness towards 21500, with the H&S target around 21100 level. A break above the 55-day moving average around 22500 would delay this bearish scenario.

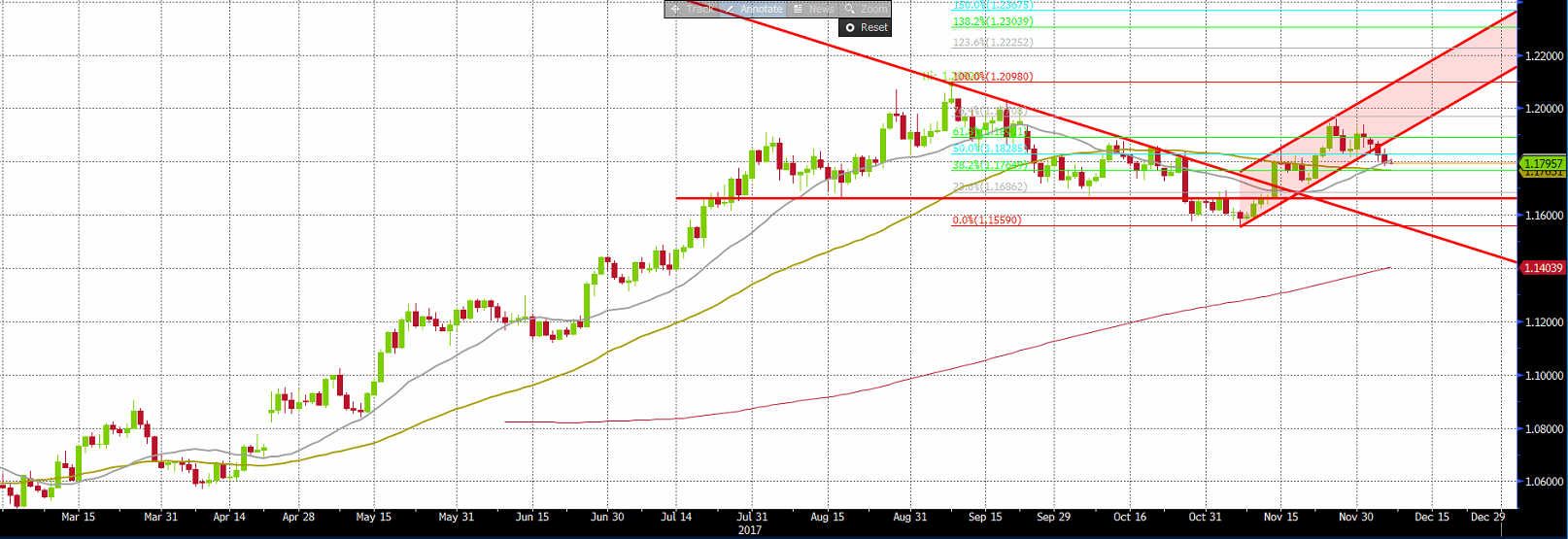

EURUSD (Daily timeframe)

EURUSD broke out of a rising channel from the lows to highs of November and trades at the 1.1800 levels. Further weakness, with a break of the daily moving average by 1.1767 could lead to accelerated losses 1.1662. A break back above 1.1880 is needed to relieve the bearish pressure.

USDRUB (Daily timeframe)

USDRUB rose to 59.32 overnight as it looks to extend its bullish run in the near-term above 60. A break of 60 would expose the recent highs July and August highs by 61.0188. Intraday support is found at 58.75.

Author

ALB Team

ALB Forex Trading

ALB Research Department is the research department of ALB Forex Trading Ltd.