Corporate Finance Part I: Thinking Long Term

How do we interpret the interaction of the real and financial sectors of the economy to determine real investment? What about the demand and supply of credit for non-financial corporations?

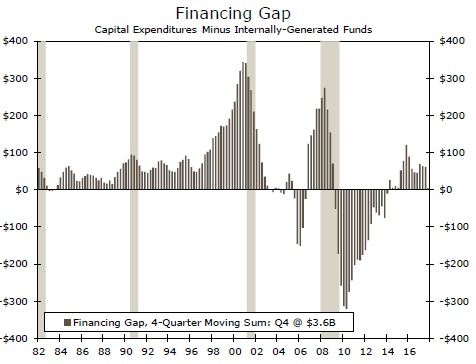

Interaction of the Real Economy and Finance

Real investment demand (e.g., equipment spending) is a major focus of current economic policy. Fundamentals dictate that the demand for investment capital depends on the real economy and the cost of capital. Increases in expected real final sales will lead to an increase in business investment. Increases in the cost of financing will diminish business investment. However, as illustrated in the top graph, the balance between the demand for funds to finance capex and the internal funds available is seldom in balance. Capex tends to rise dramatically at the end of each expansion (1990s, 2000s) relative to the internal funds of corporations. This would tend to put upward pressure on interest rates.

These interactions have created a dynamic pattern over the past year. Initially, when Donald Trump was elected, the NFIB survey jumped upward and capital goods orders grew as well. Both reflected a rise in expected real final sales. Equipment spending followed a traditional "accelerator" principle when business investment accelerates to meet the higher pace of final sales going forward. However, recent months have witnessed an increase in the financing costs of doing business, as the Fed raised rates, and thereby, we have witnessed a slowdown in capital goods orders. This is a cycle within a cycle as alternative factors (expectations and financing costs) exert their influence.

Demand for Credit: Pro-Cyclical

How can we monitor the demand for long-term credit for nonfinancial corporations? Corporate bond issuance has a pro-cyclical pattern as issuance rises with the economic expansion (1985-1988, 1993-1998) and most vividly and not yet restrained, in the current expansion. However, there is a noticeable reaction of bond issuance to an increase, even modest, in interest rates (AA yield). Late in the 1980s, 1990s and certainly in 2006-2008 there were noticeable declines in bond issuance even though the extent of the interest rate increase appeared modest.

Suppliers for Credit: Who Is Buying?

Meanwhile, on the supply side, there was a noticeable pro-cyclical pattern of increasing demand for corporate debt in the 1980 and 1990 expansions. However, this behavior ended abruptly in mid-2004/2005.

The pattern of net purchases seems to follow the pattern of gross and net issuance for the corporate bond market. The spike of purchases in Q3-2016 reflected a surge in issuance for a number of special one-time factors.

On net, these purchases are demand driven as corporations demand credit and supply comes from life insurance companies.

Author

Wells Fargo Research Team

Wells Fargo