Copper tariffs confirmed – The question is not so much about the Fed’s next meeting

50% tariff on Copper confirmed

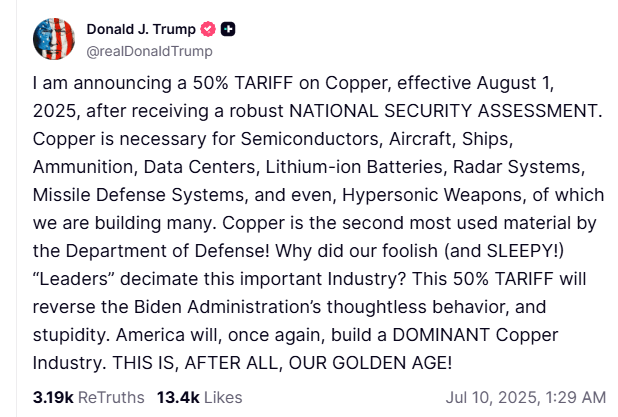

On the trade front, following US President Donald Trump’s threats on his Truth Social platform yesterday about imposing a steep tariff on copper, a crucial base metal for the US industry, today he proceeded to announce that 50% tariffs on copper imports would come into effect on 1 August, following a robust ‘NATIONAL SECURITY ASSESSMENT’.

It's interesting that the US reportedly imports about 50% of its copper needs, mainly from Chile. Considering it can take up to 30 years from discovery to production to open a new copper mine, and unless recycled copper or old mines are used to offset this, a 50% import levy is unlikely to help inflation or the manufacturing industry. US copper futures prices remain elevated, hovering around recently formed all-time highs near US$6.00 per pound.

Despite the ‘firm, but not 100% firm’ comment from Trump regarding the new tariff deadline on 1 August, he recently vowed that no extension will be granted beyond this. I find that very unlikely at this point; while a couple of preliminary agreements may make it across the line during this short time period, I expect little else to materialise from this. Investors are likely to remain complacent regarding Trump’s approach to policy setting for now, and US equities are expected to continue finding a bid.

Following 14 letters sent to various countries on Monday, including 25% levies on Japan and South Korea, essentially notifying them of their new tariff rates that will take effect on 1 August, Trump upped the ante yesterday and put pen to paper once again, sending seven more letters. Countries on the hit list varied, with the Philippines at a 20% rate, along with Sri Lanka, Algeria, Iraq, and Libya at 30%, as well as a 25% levy on Moldova and Brunei, all of which will take effect on 1 August.

Fed Minutes

The minutes from the 17-18 June US Federal Reserve (Fed) meeting – where the central bank left the target rate on hold at 4.25% - 4.50% – showed that there are only a ‘couple’ of Committee members open to a rate cut at the next meeting on 30 July. This should not raise too many eyebrows, as markets are also pricing in such an outcome (with a 93% probability).

I think it is clear at this point that the question is not so much about the Fed’s next meeting, but rather whether we will get a rate cut at the remaining meetings this year. The minutes showed that ‘some’ members see no rate cuts materialising this year, with ‘many’ officials highlighting that it will take time for tariffs to impact and a gradual softening of labour market conditions is expected. Consequently, the Committee seems to be directing more of its near-term focus to the labour side of the dual mandate.

For now, the central bank remains in wait-and-see mode: ‘well positioned to wait for more clarity on the outlook for inflation and economic activity’, but the future trajectory of rate cuts is divided amid Trump’s policy settings. This was demonstrated through the Fed's latest projections, with seven of the 19 members now pencilling in no rate cuts, up from four in March.

In terms of the economic picture, the US has so far remained relatively resilient. The jobs market has clearly begun showing signs of softening, but not enough for the Fed to act, and key inflation measures are hovering just north of the central bank’s 2.0% target. Near-term data, however, may show a very different story.

Market snapshot in early Europe

European equity markets are higher this morning, driven by the mining sector rebounding from yesterday’s drop.

US equity index futures are weaker this morning, following a positive cash session across the board yesterday, with the Nasdaq chalking up a fresh record high. Nvidia (NVDA) also refreshed all-time highs of US$164.42 and briefly reached a market capitalisation of US$4 trillion during the session, becoming the first company in the world to do so.

In the bond space, the US fixed income market saw a solid 10-year Treasury auction that was well received by investors, snapping a five-day streak of losses and sending yields lower across the curve.

Across the FX market, the US Dollar Index closed off best levels yesterday, ending pretty much unchanged, with the EUR/USD (euro versus the US dollar) echoing a similar picture, only off worst levels.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,