Considering inflation in context

With the latest year-over-year increase in the consumer price index (CPI) hitting a four-decade high, inflation has achieved a new prominence in today’s headlines. These data notwithstanding, my sense is that most people’s reaction to inflation stems not from the headlines, but rather from their visits to gas stations and grocery stores. In fact, year-over-year food price increases have been slightly smaller than the overall CPI increases (6.3% vs. 7.0%), but energy prices have gone through the roof. As of December, the price of gasoline, for instance, was up 49.6% from a year earlier. I wouldn’t be surprised if this statistic, on its own, was singularly responsible for making the pain of inflation real for virtually every US household.

Besides energy, the other big price moves this past year were for cars and trucks — particularly used vehicles. These increases appear to have been largely due to supply chain interruptions for computer chips, which sharply curtailed the availability of new cars. Those disruptions, however, appear to be easing. Moreover, while these price effects have clearly contributed to the rise in the overall index, purchases of cars and trucks may be thought of as single-event occurrences affecting a relatively small portion of households. In contrast, food and energy are staples that involve ongoing purchases across all households.

For economists, perhaps the most worrisome inflation measure is for core inflation — i.e., inflation on all items excluding food and energy. Economists generally view core inflation as a preferred policy indicator relative to the broader CPI (inclusive of food and energy), recognizing that the volatility of food and energy prices may foster spurious indications. Still, this measure more than tripled during 2021, with the year-over-year price change hitting a high of 5.5% in December. Scary.

Undoubtedly, if food and energy price increases are sustained at the current pace of increase, the sense of higher inflation could end up become embedded in our nation’s psyche, fostering a self-fulfilling wage-price spiral. On the other hand, if these price increases moderate — as they very well could — inflationary expectations would likely moderate, as well. Thus, the outlook for expected inflation in food and energy is likely to be central to those formulating economic policies.

With inflation being a kitchen table concern for virtually all of us, rightly or wrongly, it’s a political hot button. A consensus view is that failure to rein it in would probably cost Biden the White House and the Democrats Congress. Unfortunately, inflation is a difficult issue with no quick or easy fix, irrespective of who’s in the White House or which party rules in Congress. Moreover, it’s not at all clear that a change in leadership would be able to affect any dramatic change in the policy direction. In all likelihood, the obstructionist orientation in Congress will likely stymie achieving a consensus, irrespective of who’s in power.

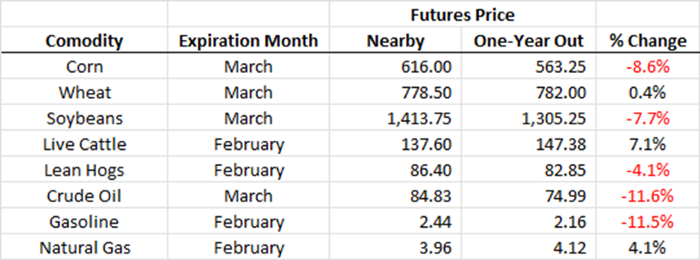

The view that inflationary pressures may soon diminish on their own may be supported based on futures prices for a variety of key commodities. I’ve looked at eight distinct markets, comparing the price of the next-to-expire futures contracts (i.e., nearby futures) with futures expiring one year later. The percent change of these respective prices reflects an approximate consensus view as to the expected inflation for these items over the coming year. These forecasts shouldn’t necessarily be expected to be borne out, but they nonetheless offer a sense of what those who operate in these markets think is a likely prospect.

I chose these contracts as representing broad classes of commodities having reasonably high levels of trading activity within the food and energy groups. Changes shown in the far right-hand column of the table below reflect closing prices as of 12/21/22. Clearly, those prices will be changing throughout any trading day, but year-over-year price differences expressed as percent changes tend to be reasonably stable.

In two out of these eight markets — cattle and natural gas — the consensus appears to be looking for prices to be higher next year. Wheat prices don’t seem to be poised for any substantive change; but price declines are forecasted in the remaining five commodities (corn, soybeans, hogs, crude oil, and gasoline).

My reading of these data is that the inevitability of expected continued inflation at current levels or higher is certainly not baked in. Of course, things can change, but that door swings both ways. Given that, to my mind, the Fed has gotten it right by only modestly reining in the pace of expansion of the money supply and waiting for more data to come in before committing to more aggressive anti-inflationary measures. Designers of our fiscal policy ought to be equally circumspect.

The typical fiscal policy solution for fighting inflation calls for reducing aggregate demand — i.e., taking actions that would lower spending by consumers, businesses, and governments at all levels. It should be understood, however, that such policies would retard the economic rebound that we’re currently enjoying — if not stall it altogether. A demand side anti-inflationary policy would in all likelihood dampen inflationary pressures, but it would do so at the cost of reducing the pace of economic growth and fostering higher levels of unemployment. It’s an open question as to whether to go down that path. The medicine could prove worse than the disease.

A less typical policy prescription would seek to increase aggregate supply. In fact, much of the Build Back Better bill would do just that, in that many provisions incentivize greater participation in the labor force. A larger labor pool would likely ameliorate upward wage pressures and improve productivity — both effects having moderating influences on inflation. At a minimum, these elements of the program deserve to be enacted. At some point, we may be forced to pivot and turn to fight inflation more aggressively; but we’re not there yet, and at this point, that adjustment would be premature.

In the meantime, blaming Biden — or anyone else, for that matter — for our current level of inflation or failing to rein it in reflects a naïve and unnuanced understanding of how the economy works. Coping with inflation requires a balancing act involving other economic considerations besides inflation by itself; and assessing the success or lack thereof in dealing with inflation needs to be considered within this broader context.

Author

_XtraSmall.jpg)

Ira Kawaller

Derivatives Litigation Services, LLC

Ira Kawaller is the principal and founder of Derivatives Litigation Services.