CNY at a glance: A surprise post-US election outperformer

Efforts from the People's Bank of China have kept the Chinese yuan relatively steady since Trump’s election in spite of a strong dollar backdrop.

Trump’s win derailed the CNY recovery but CNY has fared relatively well since

Donald Trump's election victory last November unsurprisingly sent significant shockwaves through the market, setting up a strong dollar backdrop, with the ICE US Dollar Index up 4.4% from the election as of the time of writing. This has added to depreciation pressure on numerous emerging market currencies, with the Chinese yuan as no exception.

Many investors viewed China as one of the main losers from a Trump return, with the 60% tariff scenario as the primary consideration. The market movement seemed to back this up, with the CNY moving weaker, Chinese equities selling off, and Chinese government bond yields moving lower post-election. Given the current mainstream narrative on renminbi depreciation pressure and our discussions with various market participants, one might easily assume that the CNY has been on a huge slide since the US election.

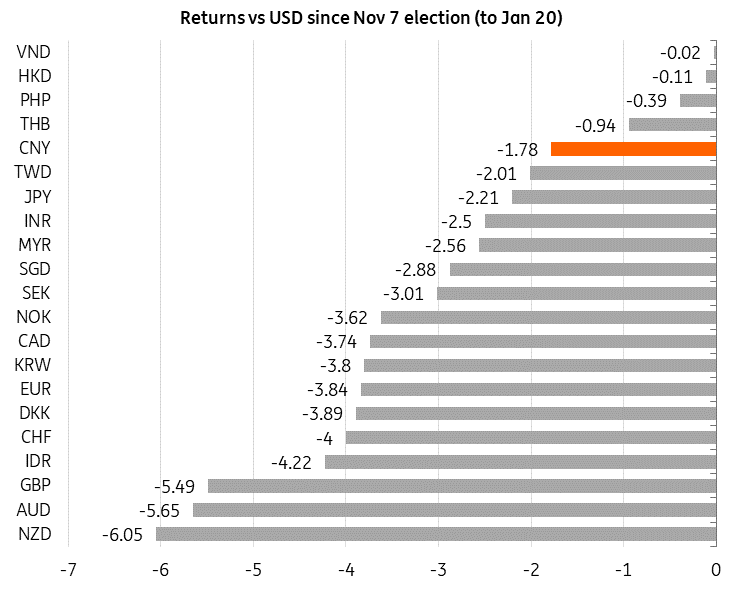

We can see that the CNY has indeed weakened by -1.78% since 8 November. However, zooming out a little we can see that the CNY has actually held up quite well compared to most other currencies. The -1.78% decline places the CNY as one of the strongest performing currencies in our basket.

This is also confirmed by looking at the trends in the CFETS RMB Index, which is up 1.8% since the November election.

CNY has actually outperformed most of the pack since the US election

The PBOC continues to hold the line in the face of mounting pressure

The recent outperformance of the CNY despite rising concerns on China’s outlook in Trump’s second term can largely be attributed to the People Bank of China's continued efforts in maintaining currency stability.

After a brief reprieve in September and October, the PBOC found itself pushing back against depreciation once more.

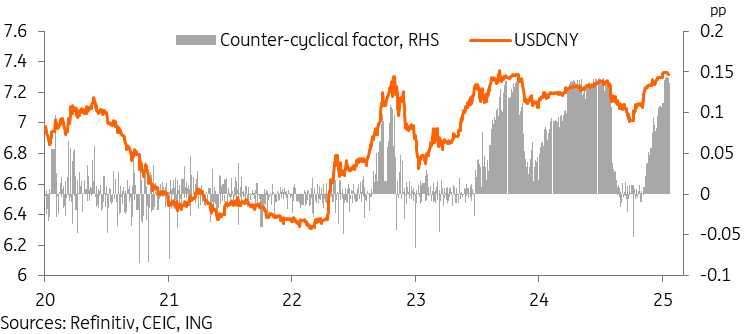

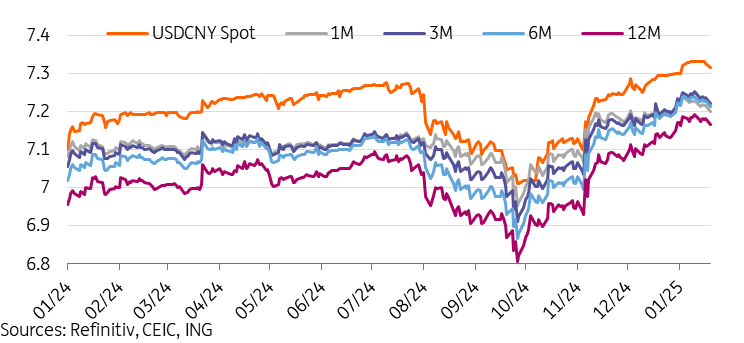

The PBOC’s primary channel for managing the CNY is through its daily fixing (otherwise known as the central parity) rate, where the USDCNY is allowed to move +/- 2% from every day.

The base fixing is based on a weighted average of market maker prices from the previous close, but is adjusted via a counter-cyclical factor, which is a manual adjustment to the base fixing level to offset cyclical volatilities driven by market sentiment. This counter-cyclical factor is the main mechanism used to express the PBOC’s stance on CNY movement; in a neutral state, the counter-cyclical factor should be at zero.

The counter-cyclical factor hit a new record high in January, implying the PBOC has strongly resisted further CNY depreciation. Markets have been watching for a fixing above 7.20 – this would be a key psychological barrier, as further upside would allow for the USDCNY pair to move above 7.35 level, which has basically marked the weakest levels for the CNY tolerated across several cycles since 2007.

This defense of the CNY looks likely to continue, at least in the near-term. The PBOC stated that it intended to keep the CNY “basically stable at reasonable levels,” and while this doesn’t mean there will be no movement at all, it’s likely that these efforts will keep the CNY as a low volatility currency this year.

Countercyclical factor shows strong PBOC pushback on depreciation

Yield spreads widened as policymakers finally allowed yields to move lower

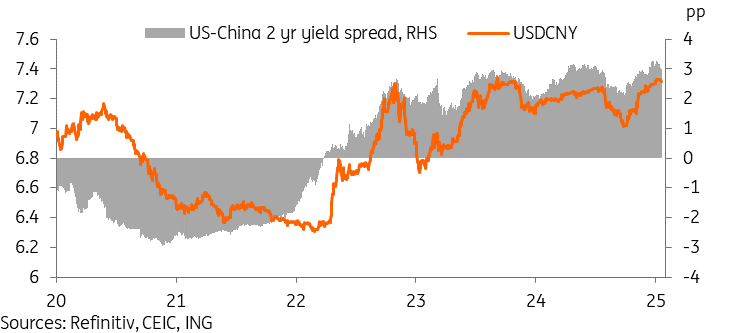

US-China yield spreads have tracked very closely with the USDCNY trajectory in the past few years. Yield spreads widened through the last few months before pulling back slightly in mid-January, as US yields climbed with expectations for a more hawkish Federal Reserve and rising government debt, while Chinese yields continued to fall.

The biggest recent development in China was policymakers quietly ending intervention in the 10-year CGBs, allowing yields to fall below 2% at a much faster pace than anticipated.

Furthermore, recent communication signalling a “moderate loose” monetary policy stance also implies that we will see further PBOC easing this year. This also pressures yields lower.

At the time of writing, 2 and 10 year China government bond yields fell 15bp and 44bp respectively since 7 November, widening our preferred 2-year US-China yield spread to around 300bp, which is up 20bp from the level seen before the US elections, and up 90bp from the lows seen last September. We expect that this spread should narrow in later months and reduce some of the depreciation pressure on the CNY.

US-China yield spreads widened once more in the last few months

Recent CNY-CNH spreads implied more depreciation speculation

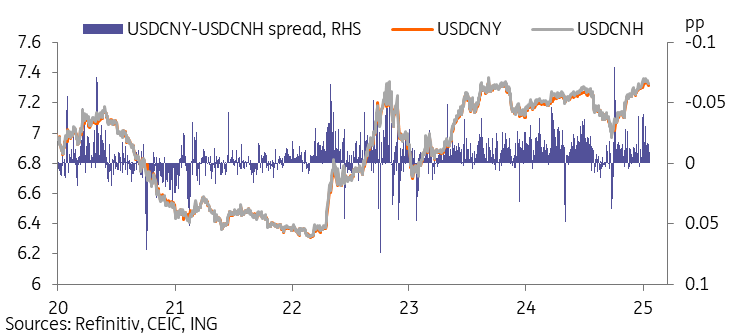

We also monitor CNY-CNH spreads, which can illustrate appreciation or depreciation pressure beyond the basic spot movement. Typically, the CNH and CNY pairs track very tightly as arbitrage opportunities typically quickly close any significant spread. However, the CNH tends to move a little more in either direction when there is momentum as it is not as tightly managed as the onshore CNY.

CNY-CNH spreads widened toward the end of December and in early January as speculative activity on CNY depreciation strengthened, but were still within a relatively normal range.

On 13 January, the PBOC announced that it would be greatly increasing FX reserves in Hong Kong, which could potentially open up room for direct intervention in the CNH market in the future. The CNY-CNH spread narrowed following these comments.

In the last few weeks, momentum has turned around, with the USDCNH actually trading at a lower level than the USDCNY pair on multiple days. Aside from several one-day spikes, this is the first time since 2022 we've seen this, and it generally reflects offshore investors positioning for a yuan recovery.

CNH-CNY spreads widened in recent weeks amid depreciation speculation

NDF market continues to imply CNY appreciation

The non-deliverable forward (NDF) market has generally been implying a CNY appreciation since late 2022. This has not changed in recent months, with NDFs still pricing appreciation across the 1, 3, 6, and 12 month tenors.

Currently, NDFs indicate that the market is pricing in the USDCNY falling to 7.17 level on a 12-month horizon, which is considerably more yuan bullish than most market forecasts, and at first glance looks somewhat conflicting with what the CNH-CNY spread story tells us.

Rather than being a sign of bullish speculation, it’s likely that amid the depreciation trend since 2022, the NDF market has been primarily reflecting corporates hedging for a potential CNY appreciation scenario.

NDFs still implying a modest appreciation in coming months

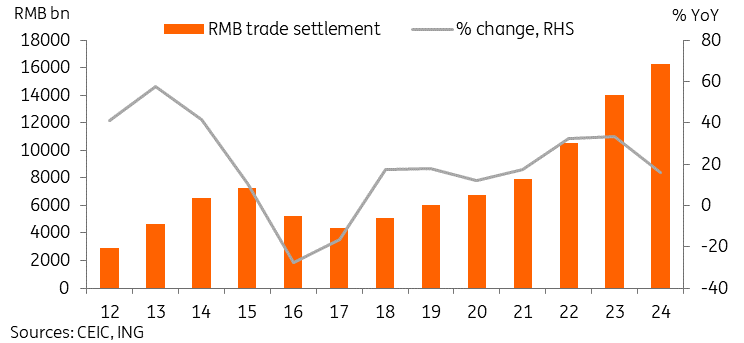

Settlement data a positive sign for long-term RMB internationalisation goals

The PBOC released 2024’s RMB trade settlement data earlier this month. In 2024, there was RMB 16.3tr of trade settlement, which marked a 16% year-on-year increase, pulling back from the rapid pace from the last two years but nonetheless maintaining a healthy pace. RMB trade settlement has nearly tripled since 2017.

While geopolitical factors have certainly played a role in the uptick, the growth in RMB trade settlement may also be in part due to China’s currency stability priority from the past few years; a stable currency is naturally more attractive for companies seeking to minimise exchange rate risk.

This longer term focus is one of the reasons that we think policymakers will continue to try to maintain currency stability.

RMB denominated trade settlement continues to grow a robust pace

Our outlook for the CNY

We outlined our three key calls for the CNY in 2025 in our China outlook piece published at the start of December.

-

No intentional devaluation to try and offset tariffs.

-

PBOC won’t abandon the currency stability objective.

-

USDCNY will remain a low volatility pair.

In the early going, these calls appear to be on track, but the true challenges may still lie ahead, especially once tariffs start coming into play – not to mention the possibility of any further surprises.

Our baseline scenario looks for a USDCNY fluctuation band of 7.00-7.40 this year. Risks to the scenario are balanced toward additional CNY weakness, with some key elements to watch below:

-

Monetary policy trajectory: how fast will the Fed & PBOC ease?

-

Tariff developments: can tariffs be delayed, reduced, or averted?

-

China domestic developments: how strong will China’s domestic policy rollout be this year? Will we see a normalisation of risk appetite?

Heading into the Lunar New Year break, it’s likely that Trump’s initial wave of policy announcements as well as any early negotiations between the US and China will play a leading role in the CNY’s trajectory. The Two Sessions in early March will also shed light on this year’s policy direction and magnitude, and is likely to be another major catalyst ahead.

Read the original analysis: CNY at a glance: A surprise post-US election outperformer

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.