CNB Rusnok: should the koruna dramatically weaken

Headlines

CNB Rusnok: should the koruna dramatically weaken after the (koruna) exit, we can sell EUR from FX reserves

CNB’s offensive in Czech media has continued in recent days and hours. The key figure, who is making headlines, is definitely CNB Governor Jiří Rusnok, who has already given several interviews to Czech economic dailies explaining the central bank strategy following its exit from the current intervention regime. From the market point of view the most interesting Rusnok words have been printed this morning in E15 daily. While Jiri Rusnok confirmed that the exit could easily be put off until 2018, he also repeated the current CNB mantra that the use of the exchange rate (targeting) would probably be discontinued in mid-2017 (while the CNB would keep its promise to defend the EUR/CZK 27.0 floor until the end of 2017Q1). The most interesting Rusnok’s statement was, however, his answer to a question whether the CNB might actually sell its euros (from huge FX reserves), if the koruna unexpectedly weakens after the exit. Rusnok said the CNB had a lot of FX reserves (mainly in euros), so if the koruna dramatically weakened, the central bank could appear on the market and sell some euros to make a profit.

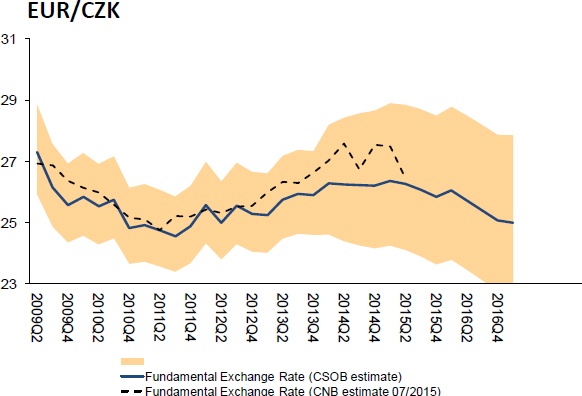

Is such a situation realistic? Actually, we think that the most probable scenario is that the koruna will strengthen on an exit-day. However, the exchange rate is likely to be very volatile, and we cannot even rule out temporary depreciation of the Czech currency. However, we doubt that there could be a swift intervention on the other side from the CNB. In our view should the CNB be involved (motivated to sell EUR) the EUR/CZK pair would have to trade somewhere above the 29.0 level – or the koruna should be weaker by around 8% from the current levels. From the fundamental point of view such a CZK weakening would be not warranted as we see the EUR/CZK equilibrium rate much lower (see the chart ).

| Currencies | % chng | |

| EUR/CZK | 27.01 | 0.0 |

| EUR/HUF | 308.1 | 0.3 |

| EUR/PLN | 4.32 | 0.1 |

| EUR/USD | 1.09 | -0.4 |

| EUR/CHF | 1.08 | 0.3 |

| FRA 3x6 | % | bps chng |

| CZK | 0.28 | 0 |

| HUF | 0.68 | 0 |

| PLN | 1.73 | -2 |

| EUR | -0.30 | 0 |

| GB | % | bps chng |

| Czech Rep. 10Y | 0.41 | 0 |

| Hungary 10Y | 2.92 | -3 |

| Poland 10Y | 2.95 | 0 |

| Slovakia 10Y | 0.49 | 2 |

| CDS 5Y | % | bps chng |

| Czech Rep. | 41 | 0 |

| Hungary | 122 | 0 |

| Poland | 76 | 0 |

| Slovakia | 42 | 0 |

Author

KBC Market Research Desk

KBC Bank

KBC's Market Research Desk publishes a number of short-term reports.