CNB review: Continued absence of forward guidance amid a soft cut

We got another 25bp rate cut from Czech policymakers - in line with market expectations - with the monetary policy stance remaining in the restrictive zone. However, real interest rates will likely get below 1.5% over the coming months, as inflation remains above the target and the reduction in rates is set to continue in November.

Easing of monetary policy conditions set to carry on

Czech policymakers reduced the base rate by another 25bp, bringing it to 4.25% at the late-September meeting. We see the Czech National Bank press conference message as neutral, with the governor citing many reasons for a cautious approach during his speech, as mentioned in our CNB preview. What we perceive as new was the firmer stance that has somewhat discounted the imminent impact of changes in foreign conditions on Czech monetary policy, be it the market view or rate reductions by foreign banks. Ales Michl stressed that things could move in any direction every half-year in financial markets while the CNB rhetoric remains unchanged and focuses on maintaining price stability. The need for a more relaxed monetary policy was also addressed, mainly due to the soft economic recovery and inflationary risks assessed as balanced when looking ahead.

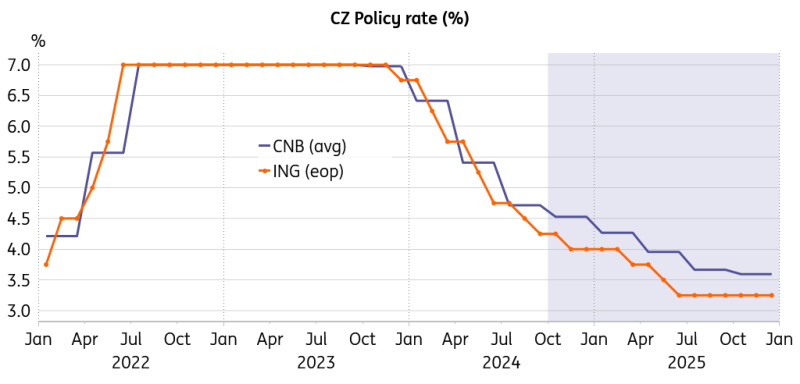

Policy rate has already moved below the CNB outlook

Source: CNB, ING, Macrobond

We maintain our view of another 25bp rate cut in November, followed by a pause in December. The December pause-or-not-to-pause dilemma must be perceived as a close call, given that any forward guidance is absent. That is except for the somewhat outdated summer forecast, with the CNB just getting below their outlook when it comes to the policy rate. The easing cycle could carry on in early spring, bringing the rate to 3.25% by mid-next year, unless there are upward surprises in January's core inflation, such as a spike in the market and imputed rents, reflecting the renewed growth in residential property prices. A downward risk to the Czech base rate is represented by the potential adverse scenario of a synchronous global economic slowdown that would bring the Czech economic rebound to a halt, and likely result in policy rates falling elsewhere.

Services and core inflation do not back off

With headline inflation just above the target and inflationary risks perceived as balanced, policymakers have turned their attention to more support for the lukewarm recovery and the never-ending underperformance of industry. However, price growth in the services sector remains elevated and persistent, resulting in core inflation remaining above CNB expectations. We see core inflation remaining elevated until mid-next year ceteris paribus, i.e. in conditions of continued gradual recovery amid softly declining policy rates.

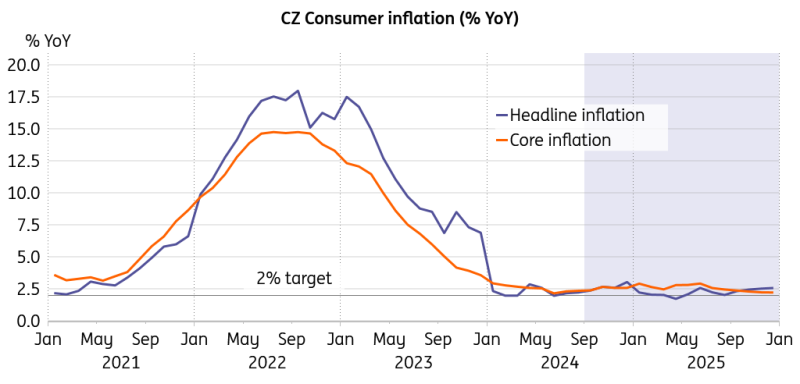

Headline inflation could increase to 3% in December

Source: CNB, ING, Macrobond

Headline inflation is set to reach 3% in December, partially due to a low comparison base of the preceding year. At the same time, the announced reduction in end prices of electricity and natural gas announced for September and December by major energy distributors could hold headline inflation in check, with either of these price reductions resulting in a 0.2pp downward effect on the overall dynamic of consumer prices. Still, there is quite some uncertainty about how pronounced those price reductions will be and how they will be recorded by the statistical office regarding the impact and timing.

Level of policy restrictiveness set to decline further

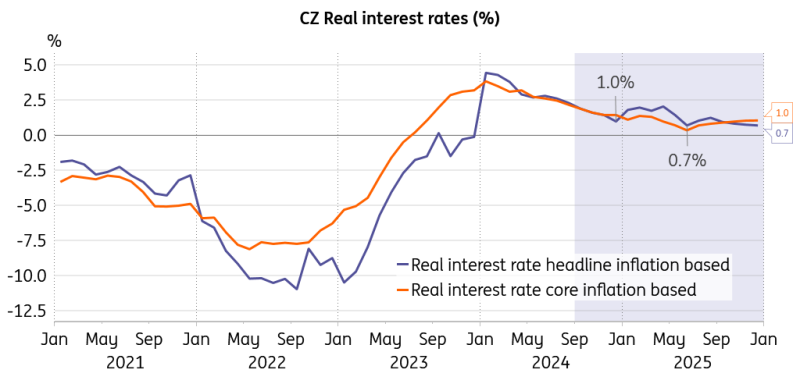

Headline inflation potentially at 3% in December and the base rate at 4% implies a real interest rate of 1%, which is still restrictive as compared with the historical standard of sub-zero real rates. The question is whether the real rates below 1.5% as measured by core inflation are enough to hold core inflation on a short leash, break the stubborn price growth in the service segment, and temper the accelerating credit growth.

Real interest rates close to 1% as measured by core inflation

Source: ING, Macrobond

No forward guidance was provided at all, except that the easing could stop at any time. It is interesting that simultaneously the governor proclaimed that they are looking more ahead. Providing adequate guidance to the markets is one of the key instruments for any central bank, as both sides can benefit from a well-defined symbiosis. We must conclude that the CNB is not particularly strong in this fine but powerful discipline, to put it mildly. This is not an emergency situation when conditions could change on a weekly or even daily basis. Inflation is close to the target, the economy is gradually expanding, so there are not many reasons to be overly reticent.

The fine art of forward guidance has been lost

To be fair, the CNB is not alone. It seems that many other central bankers have lost their telescopes to watch the horizon and be able to call: “Land!” Instead, the new normal is mostly represented by bouncing from one meeting to another, repeating that they are data-dependent. I mean, who is not? Consider the uninspiring European Central Bank communication. Yet there are exceptions, such as the Swedish Riksbank with clear statements and transparent commitments. Indeed: ars longa, vita brevis. Information is appreciated in communication, carrying the potency to form either views or expectations, which contrasts with simple data description. Advisors of the policymakers should perhaps consider obtaining a powerful stereo for the next meeting to play Led Zeppelin’s song Communication Breakdown with the volume knob turned to the right.

Read the original analysis: CNB review: Continued absence of forward guidance amid a soft cut

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.