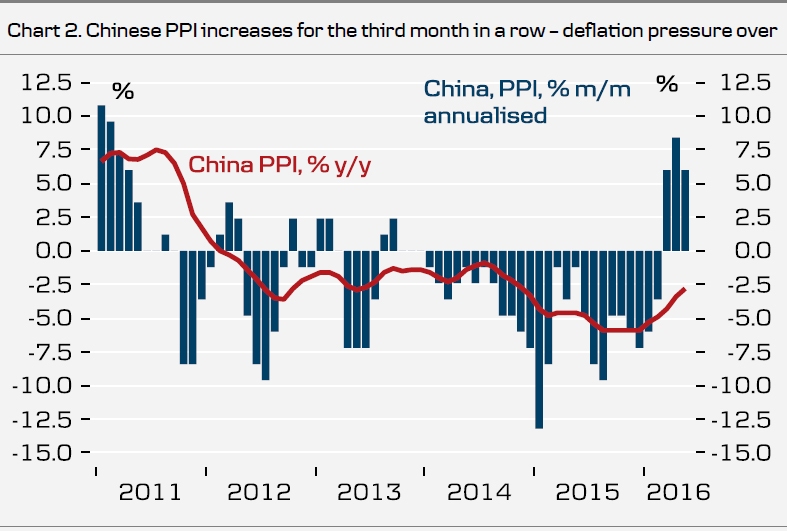

Chinese PPI inflation continues higher

-

Chinese inflation data showed a further increase in producer prices in May (Chart 2). PPI increased 0.5% m/m in May, the third monthly increase, driving the annual rate up to -2.8% (consensus -3.2% y/y) from -3.4% y/y in April. Deflation pressure has thus changed to inflation pressure at the producer level.

-

As we have highlighted before, Chinese producer prices are driven mainly by commodity prices with a small lag (see chart overleaf) and the increase in PPI is a mere reflection of higher metal prices at the beginning of 2016. Metal prices moved sideways in April and May and, in our view, PPI m/m changes should come down in June.

-

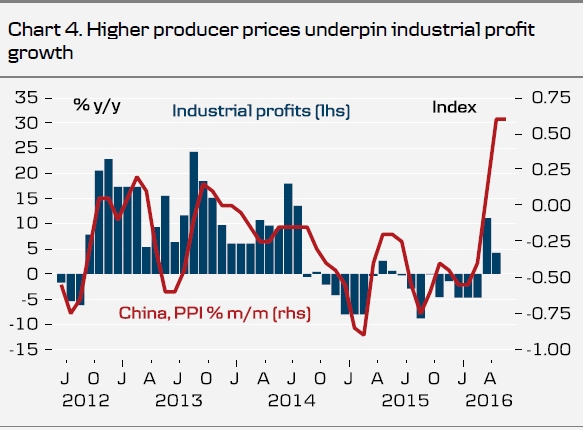

The rise in producer inflation is positive for industrial profits (Chart 4) and we estimate profit growth stayed positive in May.

-

CPI inflation surprised on the downside in May, moving down to 2.0% y/y, from 2.3% y/y in April. This is driven by lower food prices, as inflation in vegetable prices has moved lower. Inflation excluding food was unchanged at 1.1%; thus, it still points to very subdued inflation pressure. The inflation target for 2016 is 3%.

-

The main takeaway is that deflation pressure in the industry has changed rapidly due to higher commodity prices. As we look for a further gradual rise in commodity prices on the back of the pickup in Chinese construction, we expect producer price deflation to be over for now and see moderate inflation at the producer level. It has little implication for monetary policy, which is currently guided mainly by economic activity.

Author

Allan von Mehren

Danske Bank A/S