China’s trade surplus shrinks in October

A continuation of weak exports could weigh on the contribution of trade to GDP growth in the fourth quarter, though there could be a more positive story emerging about domestic demand buried in the import data. At this stage, it is too difficult to draw firm conclusions and more data is needed.

Trade figures raise more questions than they answer

China's October trade surplus shrank to CNY405.47bn from CNY558.74bn in September. The cause was a combination of weaker exports (-3.1% year-on-year in Chinese yuan terms, down from -6.2% in September) and stronger imports (+6.4%, swinging up from -0.8% in September).

Ordinarily, the weaker export figure would not bode too well for the contribution to GDP from net exports, and it certainly indicates that overseas demand for China's exports remains weak.

Conversely, the import figure suggests that domestic demand may not be as weak as indicated by, for example, the recent run of PMI numbers. Though this raises the question, which data do you put more weight on?

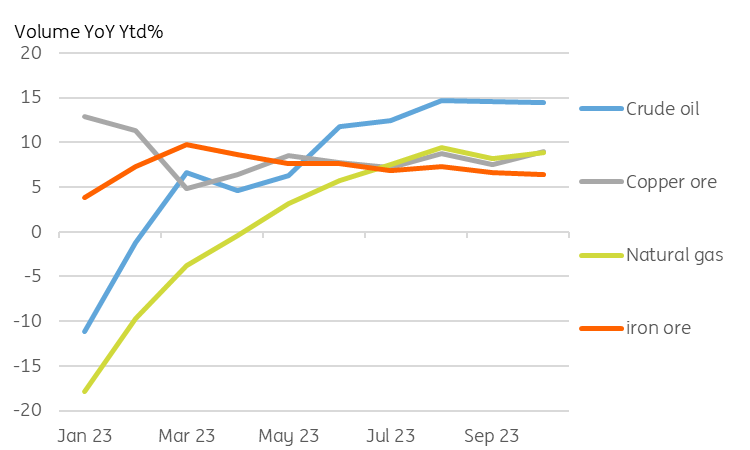

China commodity imports (YoY YTD %)

Source: CEIC, ING

Data distortions make interpretation difficult

It is tempting to try to dissect these trade figures to try to figure out what is actually going on. But even using year-on-year cumulative figures runs the risk of distortions caused by lockdowns at the end of last year in China, and our best advice at this stage is to reserve judgment on what is happening and wait to see what next month's data bring before conjuring up some fanciful explanation for what happened this month. Even looking at the figures in terms of volume levels runs risks as these numbers are also highly seasonal.

For those who are prepared to stomach these problems, the chart above of imports of crude materials suggests that in fact, this month, nothing particularly exciting took place.

In year-on-year year-to-date terms, the chart shows that imports of iron and copper ores and concentrates, together with crude oil and natural gas are all growing, though not trending particularly strongly.

Earlier inventory building for crude may account for some of the current strength in oil, and the same is also probably true for natural gas as we head into the colder winter months.

Imports of copper and iron ore and concentrates have held fairly steady in these terms at about 8.5% YoY YTD in recent months, which is probably a bit more than the state of manufacturing or construction would indicate, so there may be a more positive story brewing here. However, we think it is too soon to draw any firm conclusions in the face of such conflicting numbers, and this month's figures aren't really out of the ordinary compared to recent months either.

Not shown here are imports of refined petroleum, which are running at a 95% rate of growth, though mainly due to increases in export quotas for similar products, and coal imports are also running strongly, though the rate of increase looks to be slowing.

No change to our GDP forecasts for now

Until we get a better idea of what is happening here, we are not going to be revising our GDP figures for the year, which we recently revised higher to 5.4% for full year 2023. Whether there are the beginnings of a trade-off building between a weaker external environment and a firming domestic economy is an appealing hypothesis, but one that does not have enough support for now to run as a central forecast. Further data is needed.

Read the original analysis: China’s trade surplus shrinks in October

Author

Robert Carnell

ING Economic and Financial Analysis

Robert Carnell is Chief Economist and Head of Research, Asia-Pacific, based in Singapore.