China’s July activity data slump shows additional stimulus needed

Chinese economic activity slowed across the board in July, with retail sales, fixed asset investment, and value added of industry growth all reaching the lowest levels of the year. After a strong start, several months of cooling momentum suggest that the economy may need further policy support.

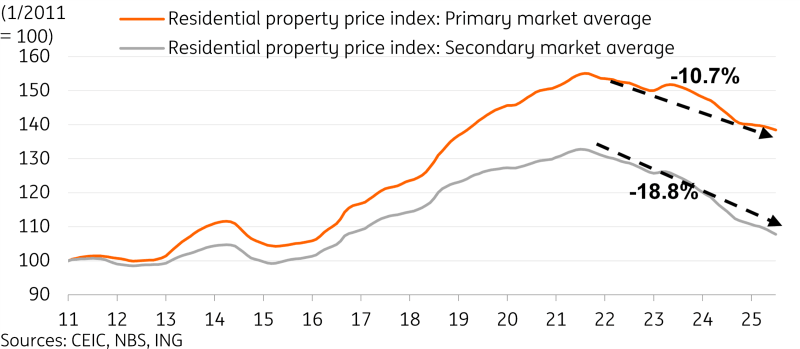

Downward pressure on property prices persisted in July

China's 70-city property price index showed that prices continued to decline. From the peak, new home prices are now down -10.7%, while used home prices are down -18.8%.

New home prices slid by -0.31% month on month, a little steeper than the -0.27% MoM decline in June, for a fourth consecutive month of steep declines. Used home prices fell -0.55% MoM, a slightly smaller drop compared to the -0.61% MoM slide in June. Neither number is likely to inspire much optimism.

The breakdown at the city level showed widespread weakness. Only 10 of 70 cities saw new home prices stabilise or pick up, the lowest number in nine months. Only 2 cities (Taiyuan and Xining) saw used home prices stabilize or pick up.

The accelerating downturn in property prices in the past few months signals that further policy support is needed. Given the high exposure of Chinese households to real estate, establishing a trough on prices is one of the most important factors to restoring confidence and generating a sustained consumption recovery. This is particularly important as domestic demand is targeted to become an increasingly important economic driver. It’s difficult to expect consumers to spend with greater confidence if their biggest asset continues to decline in value every month.

The good news: after a bit of a lull period, we could soon be seeing more support rolling out. There have been some reports of renewed efforts for government acquisitions of unsold properties. This process has had limited uptake given tight local government finances and a reluctance to make purchases, especially in regions with heavy excess supply.

Steeper price declines in past few months have dampened the cautious optimism from the start of the year

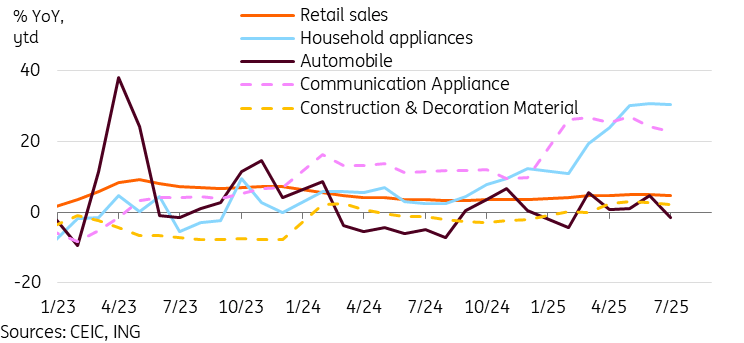

Retail Sales growth slumped to the lowest level of the year

Retail sales slumped to 3.7% year on year, down from 4.8%, and coming in well below market forecasts for a milder slowdown 4.6%. The 3.7% YoY read is so far the weakest for retail sales this year.

Most subcategories softened on the month, with continued outperformance of trade-in policy beneficiary categories. We wrote in last month's data comment that we could soon be nearing the peak for the policy-driven boost for retail sales. July's data supports this thesis, as household appliances (28.7%) and communication equipment (14.9%) sales grew more slowly than their respective year-to-date growth levels. These beneficiaries will likely continue to outperform for the rest of the year. But without new stimulus, momentum could slow.

Fortunately, supporting consumption remains one of the important goals for Chinese policymakers. Earlier this week, policymakers announced plans to roll out consumer loan subsidies for a one-year period, starting in September. Consumers borrowing up to 50k RMB will be eligible to have 1% of the interest rate on eligible loans subsidised by the government. The central government is set to cover 90% of the interest costs, and local governments the remaining 10%.

We think that this policy will help on the margins, especially to support consumption categories which may have a reliance on consumer loans, such as autos and home appliances. Reducing the interest rate burden will always be welcome news for households. However, the end impact is unlikely to be a game-changer. The real issue facing Chinese household consumption isn’t overly expensive consumer loans, but rather a reluctance to spend amid weak confidence.

Despite a soft July number, we expect policy support should keep consumption growth near mid-single digit growth for the year as a whole.

Retail Sales slumped in July amid signs that trade-in policy boost could be past its peak

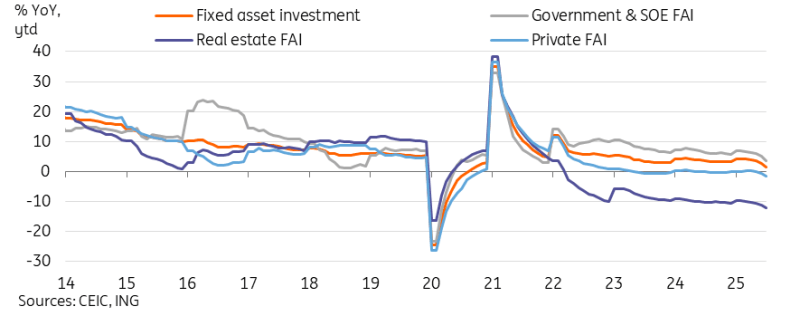

Fixed asset investment growth hits new low amid drag from private sector

Fixed asset investment growth slowed to 1.6% YoY ytd in Jan-Jul, down from 2.8% YoY ytd, and well short of forecasts for a drop to 2.7%. This is the second month of sharp declines in FAI growth, which is relatively rare considering the indicator is reported in year-to-date growth and typically prone to smaller fluctuations. Slowing from 3.7% YoY in the first five months of the year to 1.8% in the first seven months suggests a steep slowdown of investment activity in June and July.

The slowdown of investment growth has been broad-based. Given the slump in property prices, combined with still elevated inventory levels, it’s unsurprising that real estate investment continues to be the biggest drag on investment, down -12.0% YoY ytd. Private FAI has now fallen to -1.5% YoY ytd. This is the steepest decline since pandemic-impacted 2020. Manufacturing FAI, which has been a major outperformer over the last few years amid the hi-tech manufacturing upgrade demand, softened to 6.2% YoY ytd, the lowest level since 2023.

On the brighter side, on an industry level, FAI into auto manufacturing (21.7%), rail, ships, and aeroplane manufacturing (29.3%), and utilities (21.5%) remain at high levels.

Many corporates have been cautious with new investments amid high levels of uncertainty. With many industries also still in overcapacity, US-China trade negotiations apparently favouring short-term extensions rather than a longer-lasting "grand bargain", and an “anti-involution” push against extreme price competition in progress, investment growth could stay soft for some time.

FAI growth continued to slump across the board

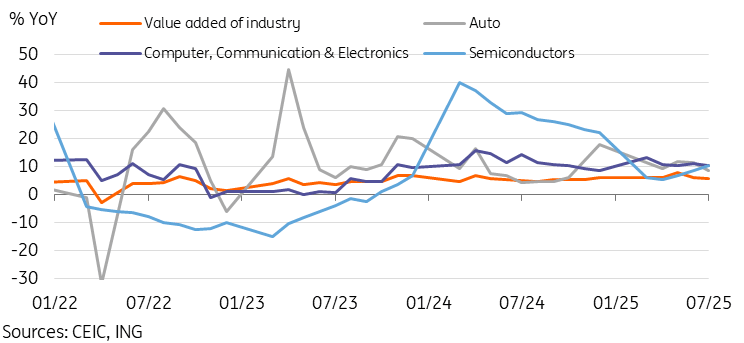

Value added of industry moderated but continues to outperform

China's value added of industry slowed to 5.7% YoY in July, down from the peak of 6.8% in June. This decline was steeper than market expectations. Much like the situation with retail sales and FAI, value added of industry saw the lowest growth year-to-date. With that said, a 5.7% YoY growth remains respectable and continues to outperform the other categories.

Most categories moderated on the month after a much stronger-than-expected June. Manufacturing (6.2%) growth remained solid, with hi-tech manufacturing (9.3%) continuing to outperform.

By industry, autos (8.5%), railway, shipbuilding, and aeroplanes (13.7%), and electrical machinery and equipment (10.2%) continued to outperform headline growth handily. Food (3.8%) and beverage (0.1%) industries, along with export-dependent textiles (1.7%) and non-metallic minerals (-0.6%) have been the underperformers.

By product, we’re seeing strong growth continue in semiconductors (15.0%) and new energy vehicles (17.1%). The burgeoning robotics industry is another outperformer, with industrial robots (24.0%) and service robots (12.8%) both seeing strong production growth.

The resilience of external demand has been an important factor for industrial production this year. With the US-China trade war truce extended another 90 days, and other competitors generally facing higher tariffs from the US from August onward, the backdrop would suggest that demand could remain relatively steady for much of the remainder of 2025.

Value added of industry moderated but continues to outperform

Challenging start to 2H25 shows policy support is still needed

A more challenging second half of 2025 is to be expected, after first-half growth exceeded most forecasts. The slump in July's data was more pronounced than expected. While extreme weather may have played a role, the broad-based slowdown in July comes on the heels of several months of generally slowing momentum. It suggests stimulus support is still needed.

Balancing the short-term growth stability objectives with addressing long-term issues such as extreme price competition remains the main challenge.

Attention has largely been on anti-involution policies rather than new stimulus policies in prior months, possibly as a result of 1H25 growth coming in stronger than expected. However, slowing momentum from the past few months may have been a reason for the announcement of a consumer loan subsidy policy this week, as well as more discussions on resuming property market support.

Chinese policymakers continue to adopt a flexible and supportive policy stance, and we expect more support measures to be announced in the coming months after the recent soft patch. As such, we still think China will remain on track to reach its target growth of "around 5%" this year.

Read the original analysis: China’s July activity data slump shows additional stimulus needed

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.