China: Loan prime rates lowered

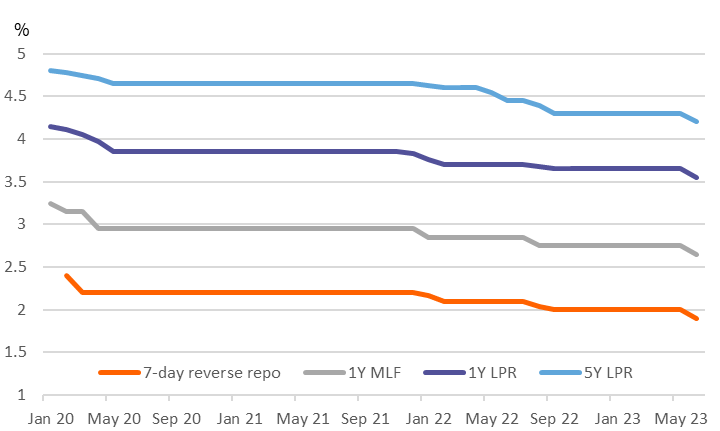

Following the earlier reduction in 7-day reverse repo rates and the 1Y medium-term lending facility (MLF), today was the turn of the loan prime rates (LPR) to be cut by 10bp - more cuts will follow.

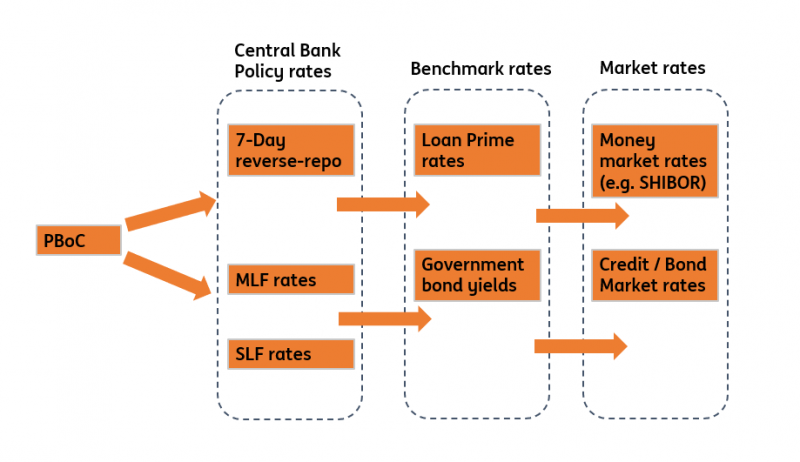

China's interest rate system

Source: PBoC, ING

Rates all coming down

After lowering the window guidance for banks on deposit rates recently, this week has also seen the policy 7-day reverse repo rate reduced, the 1Y medium-term lending facility (1Y MLF) reduced, and today, the 1 and 5Y loan prime rates reduced. This brings to an end this round of formal rate reductions, though more will likely follow in the months ahead as the economy continues to struggle.

China's monetary policy framework is a little tricky to understand if you are used to a single rate like the US Federal funds rate, or the ECB's main refinancing rate as the point around which all other interest rates and bond yields tend to pivot. But in recent years, it has moved in the direction of a more market-based system, as this note, and the amended chart which we have borrowed from the People's Bank of China (PBoC) try to explain.

The 7-day reverse repo rate and the 1Y MLF are set with a view to driving money market rates and credit/bond market rates. Loan prime rates are the rates on which mortgage yields are based. The standing lending facility rate (SLF) is equal to the 7-day repo rate plus 100bp, and is the cap for the interest rate corridor, while the 7-day reverse repo forms the floor. Deposit rates for savers are notionally set by banks but within ranges indicated by the PBoC - the so-called window guidance.

So, there is a market mechanism at play, but the monetary framework is also subject to a lot more direct control by the PBoC than in many economies.

China's interest rates

Source: CEIC, ING

A lot of action, but will it help?

The first point to note is that despite all of the rate-cutting in recent days, we are only talking about 10bp of easing and a bit of increased loan issuance. This isn't going to do an awful lot to boost the struggling economy, though it clearly is better than nothing. Even with further reductions, and we expect more of the same in the coming months, perhaps several iterations of cuts, it is not likely that we will see demand for property swing around strongly, construction will likely remain weak, and local governments will continue to feel the pinch from reduced land sales and tight finances, limiting their ability to pursue expansionary infrastructure projects.

That said, lower mortgage rates will provide a little additional cash flow boost to households and help retail sales and consumer spending to provide some support. And at least China is not having the same spending-power-sapping inflation problems that the rest of the world is suffering from, so there are few impediments to further cuts in policy rates save the political desire not to overdo it and stoke bubbles in parts of the economy. The risk of that happening at the moment seems very low. That said, the current rate of retail sales growth does look to contain a fair bit of pent-up demand following the economy's re-opening at the end of last year, and it is likely to weaken in the months ahead. Further rate cuts may help to soften the adjustment downwards when it comes.

The reduced rate backdrop will likely continue to weigh on the CNY, at least until US Fed policy also turns lower, so we will probably need to make further amendments to our USDCNY profile, keeping it weaker through 3Q23 and maybe softening the turn when it comes.

Read the original analysis: China: Loan prime rates lowered

Author

Robert Carnell

ING Economic and Financial Analysis

Robert Carnell is Chief Economist and Head of Research, Asia-Pacific, based in Singapore.