Central Bank Envy: The ECB and the Bank of Japan are captured by zero rates

Mario Draghi and Haruhiko Kuroda must be envious of Jerome Powell. The US central bank has been raising rates for three years. If the Fed Funds at 2.5% are not as high as the governors might like at least they are sitting on a modest cushion if a recession occurs this year or next. The European Central Bank and the Bank of Japan are seated on bare planks.

Few analysts are currently predicting a global recession. The IMF and others are forecasting slower growth. But there are enough risks in the environment, from a no-deal Brexit to the US-China trade dispute and political discontent in France and Germany that if one or two go wrong a recession becomes a distinct possibility.

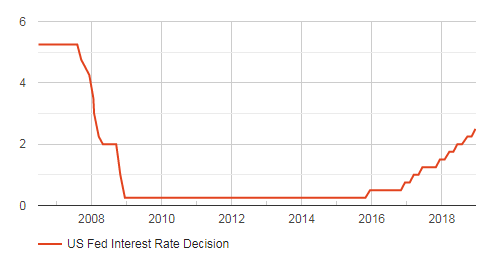

Central banks have essentially one tool for manipulating the economy, interest rates. That is why the Fed has persisted in raising rates since December 2015 even though none of the standard indicators of an overheating economy were evident. It was criticized by some for its actions. If the US faces an economic contraction the Fed can turn to the Fed Funds rate first.

Fed Funds Interest Rate

Chart: FXStreet

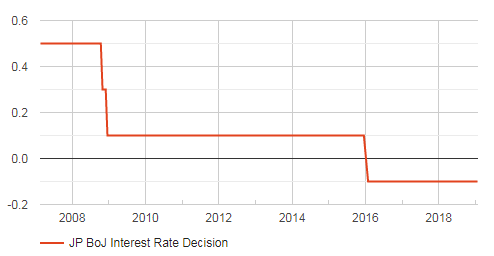

The ECB main refinancing rate was held at 0% on Thursday. A number of sovereign rates in the EMU are already negative. The German 2-year Bund was at -0.58% on Thursday. Its return has been negative for more than four years. The 10-year was at 0.18%. The US 10-year Treasury was at 2.73%, the 2-year at 2.58%. Japan's 2-year JGB was -0.17%. It has been negative for three years. The Bank of Japan’s short term base rate at -0.1% has also been negative for three years.

ECB Main Refinance Rate Bank of Japan Short Term Base Rate

Charts: FXStreet

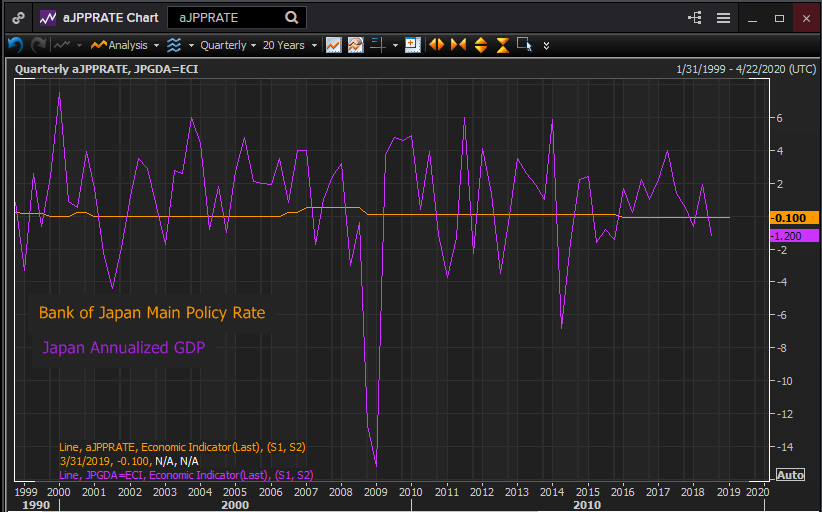

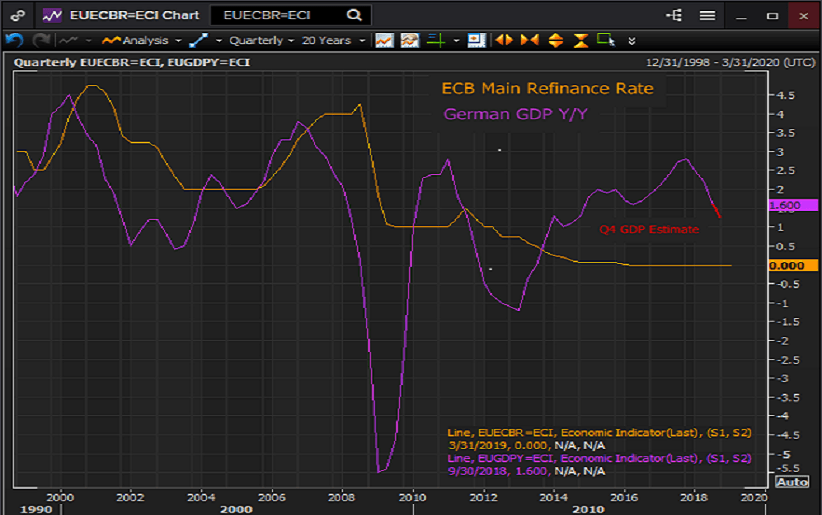

The ECB and the Bank of Japan face a dilemma of their own making. Forced by the exigencies of the financial crisis to enter the nether world of negative rates, they have maintained their policies far longer than sensible, attempting to use interest rates as a palliative for deep seated economic, political and demographic problems. The surface issue addressed by the policy, weak economic growth, has not been corrected by low rates because it is not a temporary situation but an expression of an overall loss of dynamism in the economy and society at large. All that has happened is that their economies have become addicted to low rates and they have foreclosed their own best counter to the next recession.

The effectiveness of interest rate policy is relative, it diminishes as you approach zero. The reviving effect on an economy of a 3% reduction in market rates from 5% is very different than a reduction that starts at 0%. Neither Japan or Germany have seen permanent sustainable economic improvement from zero rates. Their growth seems to have operated independently of the rate environment since the imposition of very low returns.

Charts: Reuters

In the next recession the ECB and the Bank of Japan will find that they have contracted out their recovery to the Federal Reserve and the Bank of China. It will be the Americans and the Chinese who, in stimulating their own economies will provide whatever reviving breath reaches Europe and Japan.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.

![Hyperliquid representatives, Trade[XYZ] meet SEC Crypto Task Force to discuss digital asset regulation](https://editorial.fxsstatic.com/images/i/Hyperliquid_Bull.png)