Caution and profit taking has crept into the market

US equity futures are mixed with modest moves as caution and profit taking has crept into the market following yesterday’s risk on rally. Wall Street surged with gains of over 1.5% on the broader indexes as strong efficacy rates on three vaccine candidates continued to brighten outlooks and increase the potential for a return to normalcy sooner than later. However as the overall outlook remains positive for US futures there seems to be limited appetite to push valuations out further for now, as much of next year’s (expected) recovery is already priced in, while virus developments spell further restrictions for the weeks and likely months ahead.

Expectations that Janet Yellen would be named as Treasury Secretary under a Biden administration was a relief as she’s a known quantity and would likely support hefty stimulus. Treasuries sagged, not surprisingly, on the strength in risk appetite and amid a heavy supply slate this week.

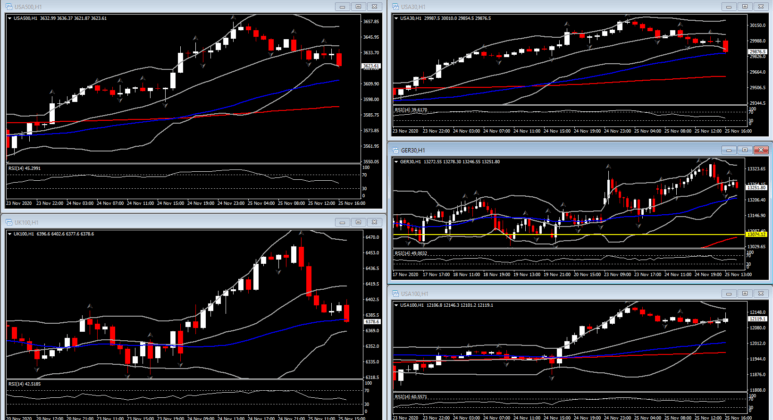

Today features a heavy dose of data ahead of the market closure on Thursday for the Thanksgiving holiday, which could make for choppy action. Of note, Q3 after tax corporate profits came in at a record 27.5% pace, from -10.7% in Q2. The USA30 is off -0.2% but sustained close to 30K area while the USA500 mini has slipped -0.06%. The USA100 mini is 0.3% firmer after underperforming the rally yesterday that saw the USA30 close above 30k for the first time ever.

GER30 and UK100 futures are down -0.1%, and up 0.3% respectively. Governments across Europe are pondering how and if to ease lockdowns over the festive period while the WHO has already warned of a third wave in the winter.

Yields have dipped modestly after disappointing jobless claims data and as stock futures give back some of yesterday’s historic gains. US Advance goods trade deficit widened to -$80.3 bln in October after the unexpected narrowing to -$79.4 bln in September. Advance durable goods orders rose 1.3% in October after climbing 2.1% (was 1.9%) in September. This is a sixth straight monthly gain as orders recover from the pandemic plunge in the spring that saw an -18.3% drop in April, just short of the weakest on record of -18.8% from August 2014. US initial jobless claims rose 30k to 778k in the week ended November 21 after claims gained 37k to 748k (was 742k) in the November 14 week. It is the strongest reading for initial claims in five weeks, as the surge in Covid infections and the consequent increase in restrictions on activity has weighed on the job market. Last the US Q3 GDP growth was left unrevised at 33.1% from the Advance report. Growth has bounced back at an historic pace after cratering at a record -31.4% rate in Q2.

The belly of the curve is outperforming with yields down over 1 bp as the market digests this week’s record supply. The 5-year is at 0.385%, with the 7-year at 0.634%. The 10-year has richened 1 bp to 0.870%, and the bond is flat at 1.60%. The 5s-30s bull steepened to 121.5 bps from 120.8 bps yesterday and 116.7 bps Monday. Bonds should find support from worries over spiking virus cases and more strict lockdowns, along with month-end where Barclays forecasts a 0.16-year extension, the most since 2009.

Attention remains on vaccines and the virus. Additionally, Brexit warnings and comments from central banks suggesting caution on additional rate cuts added to pressures on equities. ECB officials continue to flag the extension of PEPP. Mersch, however, signaled he is not looking to cut the deposit rate further. T

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in