Can the EM rally keep running?

Key points

-

Emerging markets (EM) beat developed markets (DM) in Q3, supported by strong gains in tech-heavy North Asia and stabilizing sentiment in China.

-

South Korea, Taiwan, and parts of Latin America led the rally, while ASEAN markets lagged.

-

The advance was sector-driven by cyclical growth plays such as consumer discretionary, technology, and materials.

-

Earnings expectations remain supportive, but risks from tariffs, dollar strength, and fragile positioning mean outperformance is not guaranteed.

What drove EM’s Q3 surge

Emerging markets extended their edge over developed peers in Q3, with the MSCI EM Index climbing around 11% versus ~7% for developed markets.

Several factors explain the outperformance:

-

AI supply chain tailwind: South Korea and Taiwan benefitted from surging demand in the semiconductor and AI hardware value chain.

-

China stabilization: Easing concerns around growth, coupled with renewed optimism in tech and policy support, helped Chinese equities recover.

-

De-escalation of trade tensions: The U.S.-China tariff pause meaningfully improves the outlook for EM assets.

-

Macro backdrop: Fed’s rate cut removed major drags on EM equities, allowing EM central banks to ease policy to support growth and for flows to return.

-

Dollar weakness: EM’s historical underperformance relative to DM – lagging by an annualized 6% since 2010 – has coincided with a prolonged dollar strength period. With the DXY index down 10% YTD, that headwind may be easing, potentially driving greater EM flows.

-

Positioning and flows: EM equities continue to trade at a valuation discount versus developed peers, which makes them appealing in a late-cycle environment. MSCI EM trades at 12.4x earnings, near its 25-year average. At the same time, US policy risks remain an overhang that could reshape relative performance.

Market standouts: Leaders and laggards

Leaders:

-

South Korea led Q3, boosted by chipmakers and AI exposure.

-

China saw improved performance on stabilization hopes and AI optimism.

-

Latin America benefitted from commodities and credible policy environments.

Laggards:

-

ASEAN markets, such as Thailand, underperformed due to weaker domestic demand and limited tech exposure.

-

India saw rising tariff risks leading to profit-taking and investor caution.

Sector pulse: Where momentum lies

Looking at one-month sector returns (local currency), the EM rally was distinctly cyclical:

-

Outperformers: Consumer Discretionary (+12.6%), Technology (+10.4%), Materials (+10.3%), Communication Services (+8.2%).

-

Mid-performers: Industrials (+3.3%), Energy (+3.3%), Utilities (+2.6%).

-

Laggards: Financials (+1.1%), Health Care (+1.1%), Staples (+0.2%), Real Estate (+0.1%).

This suggests investors are leaning into growth-sensitive sectors tied to AI, consumption, and commodities, while defensives have lagged.

What can propel EMs further?

Several factors will determine whether EM outperformance can be sustained:

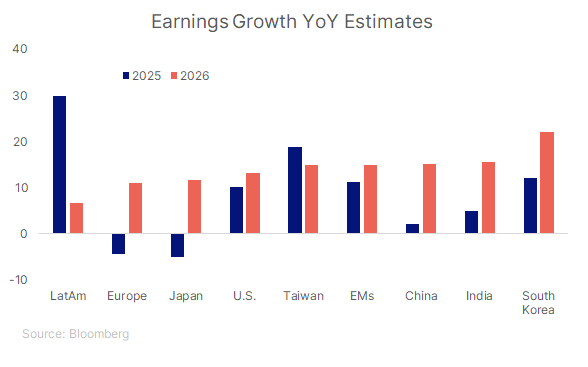

1. Earnings expectations

Bloomberg consensus shows EM maintaining a strong lead: +11.3% in 2025 and +15.0% in 2026, compared to lower U.S. and Europe outcomes. Sustained revision breadth will be important to watch.

2. Valuations and flows

EM equities continue to trade at a discount versus DMs (12.4x forward earnings, near the 25-year average). With global AUM share in EM down to 5% from 8% in 2017, the asset class remains under-owned and could benefit from rotation away from past winners into less favored markets.

3. Trajectory of the US dollar

The trajectory of the U.S. dollar remains critical. A softer or stable dollar historically supports EM performance and flows, while renewed strength could challenge returns. Many EMs also maintain positive real yields, providing scope for selective policy easing.

4. Domestic policy and reform momentum

Structural reforms—from capex incentives and friendshoring policies to improvements in market plumbing—can enhance medium-term earnings resilience. Markets such as India, Mexico, and parts of EMEA have policy stories that underpin longer-term investor interest.

5. Commodities and terms-of-trade

Resource-rich LatAm and EMEA benefit from elevated metals and energy cycles, while importers in Asia gain from softer energy prices. This divergence argues for active, region-specific allocation.

6. Sector leadership durability

AI-linked supply chains in North Asia, the EM consumer boom, and commodity cycles provide potential long-run drivers. Yet late-cycle rotation into defensives could alter the leadership balance.

7. Positioning and liquidity

Under-ownership suggests room for inflows, but flows can be lumpy and smaller EMs may see disproportionate swings on incremental moves. This creates both opportunity and volatility.

Overall, these factors suggest the rally can continue, but its sustainability will depend on earnings breadth, the dollar’s path, policy progress, and global risk appetite.

What could derail EM outperformance?

-

Tariff escalation: An escalation in U.S. trade policy, such as renewed tariff rounds, could hurt EM exporters and particularly developed peers with high U.S. revenue exposure. This risk underscores how dependent global earnings are on trade policy stability.

-

Dollar strength: A resurgence in the USD could reverse EM relative gains, given the historical sensitivity of EM asset flows and performance to dollar cycles.

-

Positioning fragility: While flows are improving, investor positioning remains light and can change abruptly, leading to higher volatility. These risks mean investors should remain mindful that EM outperformance is not guaranteed and depends on external as well as domestic policy conditions.

Investment lens: What it means for EM allocation

EM remains under-owned, with its global AUM share dropping to 5% from 8% in 2017, and stands to benefit from powerful rotation trades from past winners to less favored markets. Leadership has also shifted within EM—from regions with stellar returns in 2022–24, like Taiwan and India, to laggards such as Korea and LATAM now taking the lead. Each year tells a different story and EM companies face unique domestic and external challenges. A long-term and active approach, focusing on structural trends such as friendshoring, technological innovation and the EM consumer boom, remains crucial.

Final word

Emerging markets are enjoying a structural and cyclical tailwind, with earnings momentum and sector leadership in their favor. But investors should remain alert to macro headwinds such as tariffs and dollar swings that could test EM resilience into year-end.

Read the original analysis: Can the EM rally keep running?

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.