Business sentiment: Loss of momentum but no change in direction

The S&P Global PMI surveys are a key input in the assessment of the cyclical environment. Judging by the manufacturing PMI, many countries have seen a weakening of momentum in the second quarter of 2024 versus the first quarter. However, for most countries, the level of the PMI in June is still higher than in December 2023. Moreover, 17 countries out of 31 still have a PMI of 50 or higher, which reflects ongoing growth in economic activity. Focusing on the Eurozone and using the composite PMI to take into account the important role of services, it is reassuring to see that in June, although dropping from the 52.2 level recorded in May, the composite PMI was still in ‘real GDP growth territory’ at 50.9. A drop below 50 might fuel a narrative of slow growth, at best, with an increased risk of negative quarterly numbers. However, the combination of ongoing disinflation, the ECB that has started a rate cutting cycle and structural investment needs -green and digital transition- leads us to think that the recent loss of momentum of survey data does not represent a change of direction for the Eurozone business cycle.

In the assessment of the cyclical environment, business surveys play an important role. A key input are the S&P Global PMI surveys because of their broad coverage, their timeliness, and their close correlation with real GDP growth.

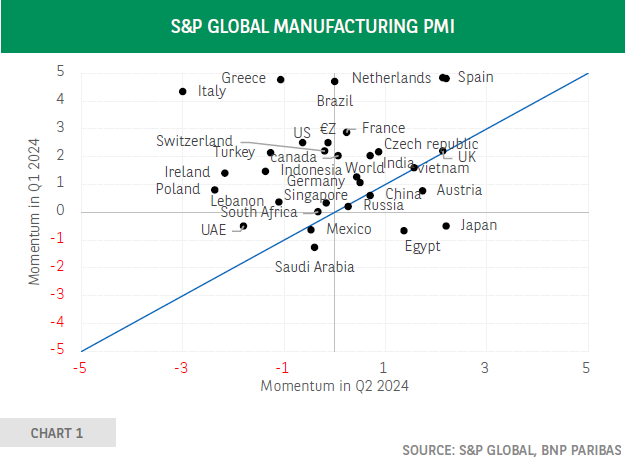

Chart 1 compares the momentum of the manufacturing PMI data for the second quarter of this year with that of the first quarter. Most countries are above the diagonal line, which reflects a loss of momentum in the second quarter versus the first. Is this a source of concern? Before answering this, let’s remember that the PMI questionnaire asks whether, in the case of output, the survey participant has a higher, unchanged or lower level of production compared to the previous month.

A loss of momentum thus implies a less dynamic growth environment, that is the balance of companies reporting a higher output has decreased. Nonetheless, before drawing any firm conclusions, one needs to check whether the recent momentum measure is positive (though less than before) or even negative and, secondly, where this leaves us in terms of latest reading of the PMI level.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.