Brexit talks, Carney and Politics: time for the pound to break free?

In a week relatively free of economic data and earnings news, fundamental events taking place in the UK could still spark some life into GBP/USD, which has had two of its quietest months for 2 years. Before we discuss the painfully slow progress of cable, it’s worth looking at the upcoming events and spending some time assessing the potential financial market impact.

Bank of England Governor Mark Carney delivers his Mansion House address, 0830 BST, Tuesday 20th June

The Mansion House event was scheduled for last week, but was delayed after the Grenfell Tower fire. In the past, Mark Carney has used his Mansion House speech to deliver a very candid message on the state of the UK economy and even to deliver a message on policy, anyone remember when Carney introduced forward guidance at his first Mansion House speech? While we expect Carney to be more tight-lipped this time round, we do think that he will need to address the recent vote split at the BOE, where 3 members’ voted to hike interest rates last week, and 5 voted to keep rates steady. We should get a sense from Carney if there is a chance that other MPC members will also switch to voting for a rate hike in the coming months. However, we think that a near-term rate hike from the BOE is unlikely. Firstly, Kristen Forbes, one of the MPC dissenters, is leaving at the end of this month, and we don’t know how her replacement, Silvana Tenreyo, will vote and whether she will continue Forbes’ tradition of voting for a hike. Secondly, we expect Carney to continue to sound concerned about the squeeze on households, after the rise in inflation and the collapse in wage growth. Lastly, we believe that there is a chance that Carney could use this speech to hint at the end of the Term Funding Scheme that was implemented after the Brexit vote. If this happens then we doubt that the bank will end this scheme and hike rates at the same time, so a rate hike could be on the back burner for some time. We expect Carney’s speech to have the biggest impact on the pound, and any shock sign that rates could rise in the coming months is likely to have a major upward impact on sterling and UK bond yields.

Brexit negotiations begin and EU leaders’ Summit: Thursday and Friday 22/23rd June

The UK and the EU have formally started Brexit negotiations this week. So far, there have been official handshakes and everything has been very polite, however the battle could get fierce later this week. The two biggest clashes between the UK and the EU may come on Tuesday and Thursday when issues such as the location of two UK-based agencies, the European Medicines Agency and the European Banking Authority, are expected to feature in the talks. On Thursday, EU leaders will discuss the big Brexit questions over dinner, Theresa May has not been invited. The markets will be listening for any leaks and titbits of information from these talks, and any sign that the EU is likely to treat the UK harshly or stop the UK from easily accessing to the EU single market after Brexit could send a cold shiver through UK asset prices. We believe that the pound, which is very sensitive to the prospect of a hard Brexit, and the FTSE 250 could be most at risk from weakness if the talks don’t seem to be progressing in a constructive fashion. It is worth remembering that the pound tends to have a negative correlation with the FTSE 100, so if the pound declines this week on the back of negative sentiment emanating from these talks then we may see the UK’s main stock index perform well.

UK Queen’s Speech, and vote: Wednesday 21st June, vote 28/29th June

This event is usually innocuous for financial markets, but we believe that the fallout from the Queen’s Speech vote could have major ramifications for UK asset prices. The current UK government is still without a formal majority in Parliament, as there has been no official deal between the Conservatives and Northern Ireland’s DUP party. This could make the next week fairly hairy for Theresa May. The Official Opening of Parliament takes place on Wednesday 21st June, followed by a vote on the Queen’s Speech the following week. The vote on the 28th -29th June will be critical, if it looks like the government won’t achieve the majority necessary to get the vote passed then it is likely that the Conservative Party could depose of Theresa May, thus leaving the UK facing a new Prime Minister less than a year after May took office. Globally, financial asset prices have been remarkably resilient in the face of political unrest, however we believe that the pound and the FTSE 250 could be targets of selling pressure if the Conservative Party decides to replace Theresa May with a Brexiteer. Reports at the weekend suggested that the 1922 Conservative Backbench Committee, which is rife with Brexiteers, is plotting to replace May behind the scenes, and that some of them are unhappy with the softening in the government’s Brexit stance since the election earlier this month. We would expect to see volatility spike in the pound if the market has to once more start pricing in the prospect of a hard Brexit.

Sterling analysis: Why so stagnant?

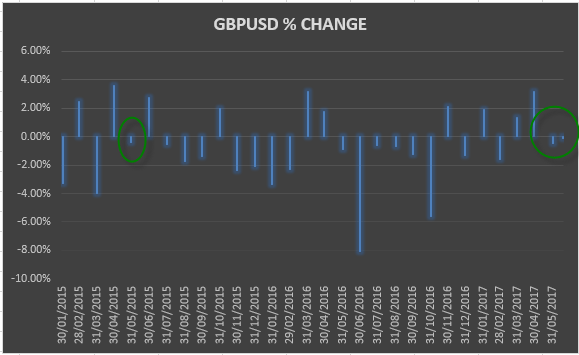

We have done some monthly analysis on the % change in GBP/USD since 2015 and we have found some interesting results. GBP/USD’s % price movement has been -0.47% for May and -0.15% so far for June. These are the smallest monthly price moves since May 2015, you can see the results in a chart in figure 1 below. This suggests that throughout the UK election campaign and during the inconclusive result, the pound was incredibly stable when looked at on a weekly and monthly basis. This is highlighted by the fact that the pound has been range-bound in recent weeks, and was unable to make headway above the key 1.30 resistance level vs. the US dollar.

Looking ahead at this week’s political and central bank risks two things stand out as potential drivers of sterling volatility. Firstly, a hawkish Mark Carney. This would be a major shock to the market, as the UK Overnight-Index-Swaps (OIS) market, a way to gauge market expectations for interest rates, is still not fully pricing in a single rate hike by the end of 2018. We expect this to be a low probability, but high risk event, which could trigger an initial knee jerk reaction higher in the pound, and could see GBP/USD get back above 1.30, towards the 1.30- 1.35 range in the next three months.

We believe that the prospect of Theresa May being ousted as PM in the next few weeks has a much higher probability of occurring. The latest YouGov survey has seen Theresa May’s approval rating slump to -34 from +10 before the election was called. If Theresa May can’t get enough votes to pass next week’s Queen’s Speech Bill then this increases the risk that a Brexiteer gets inside the door at Number 10, which could be seen as Kryptonite for the pound, and trigger a move back towards 1.20.

Thus, GBP/USD may remain stable in the face of this week’s political and monetary policy risks, however, it is unlikely to stay that way if we see turmoil in the Conservative Party, which in our view is the biggest risk to the pound right now.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)