Brexit and the next 100 days in five charts

New UK prime minister Boris Johnson will face the same hurdles as Theresa May, and crafting a new Brexit deal will be tricky. The new leader may be open to 'no deal', but Parliament will do all it can to stop it. We think a general election is increasingly likely - maybe even inevitable - and the pound is likely to come under further pressure.

With 100 days to go until Brexit, the UK finally has a new prime minister - former foreign secretary Boris Johnson.

Fears are growing that the UK could leave the EU without a deal on 31 October, but at least in the first instance, one of the PM's first acts will be to return to Brussels and seek a reworked deal. But with neither side willing to compromise on the Irish backstop - the mechanism designed to avoid a return to a hard border between Ireland and Northern Ireland - negotiations are unlikely to bear fruit.

This sets the stage for an almighty battle in October as Parliament tries to stop 'no deal' from happening - and a no-confidence vote in the government is likely to happen in the run-up to the Brexit deadline. A general election is getting more likely - perhaps even inevitable. Recent polling suggests that an election might not actually be a bad thing for Mr Johnson - but given that an election would almost certainly require another Article 50 extension, his party's renewed popularity could falter by the time the vote occurs

All of this uncertainty makes for a tricky few months for the economy, and this has sparked talk of a UK rate cut later this year. Markets see a 50% chance of easing in 2019, although we're yet to be convinced. Even so, the risks for the pound are intensifying - we could see EUR/GBP hit 0.92 over the summer.

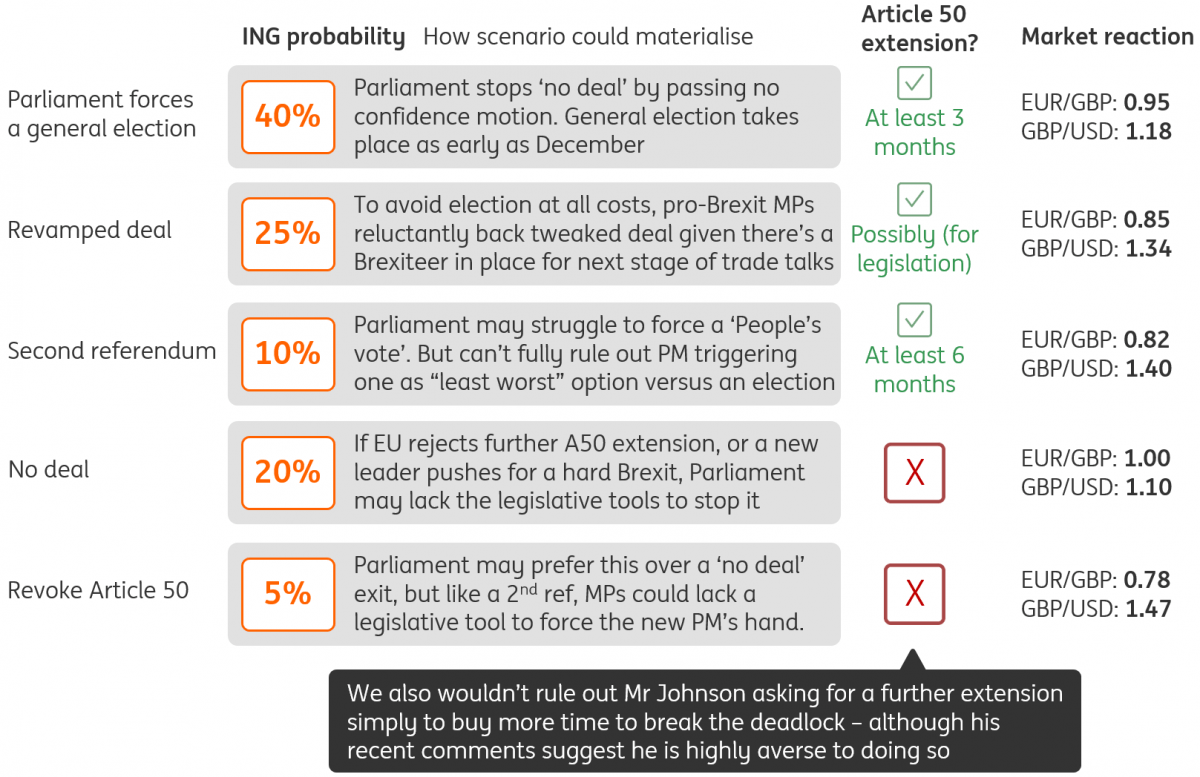

Our updated Brexit scenarios

Finding a tweaked deal that both the EU and Parliament can agree to will be challenging

Despite all the ‘no deal’ rhetoric, we assume the new prime minister will initially head to Brussels in September to attempt a renegotiation of PM May’s existing deal. But seeking a meaningful change to the agreement from the EU – and then getting enough MPs to support it – will be seriously challenging.

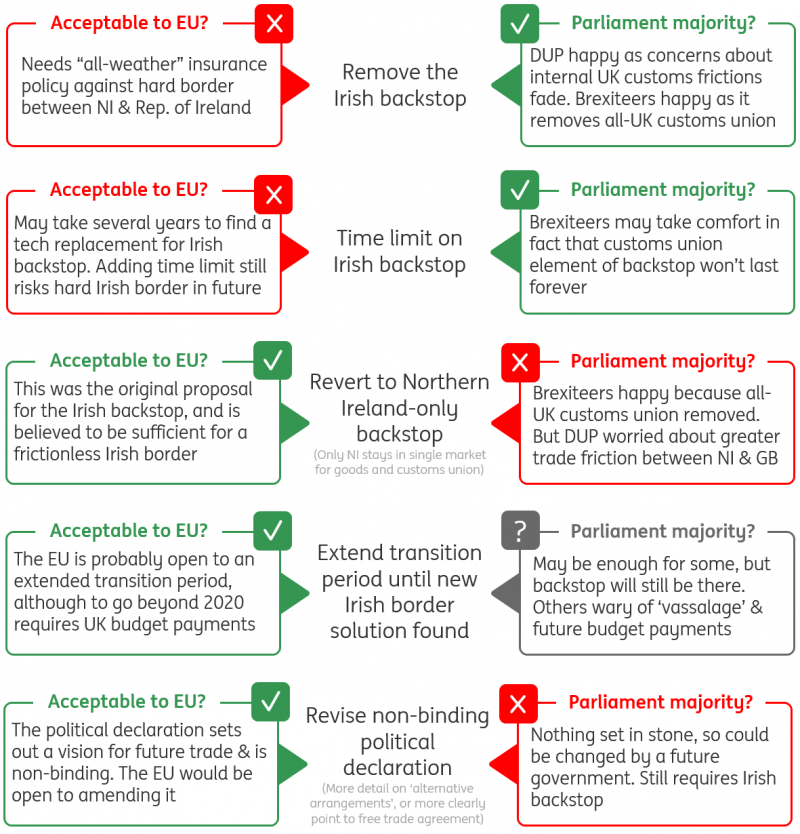

Brussels has ruled out removing, or time-limiting, the contentious Irish backstop – something which Mr Johnson has repeatedly said is a red-line in talks. So what could the new prime minister do? The chart below shows how most proposals would be unacceptable to either the UK or the EU, although one particular idea looks interesting.

One way the new PM might be able to command a majority is if he can convince sceptical MPs that the Irish backstop will never come into effect - and the most obvious way of doing that is to ask for a long transition period with the EU. In theory, that could allow time to find a different - perhaps technological - solution to preventing a hard border on the island of Ireland.

In reality, it could be several years before such technology becomes available (if it becomes available at all), but in principle the EU would probably be open to a more prolonged transition period. The current deal leaves the door open to a transition until the end of 2022, assuming both sides agree.

What are Mr Johnson's options for a revised deal?

If a deal is to get a majority in Parliament, the devil might not be in the detail after all

So is the ‘long transition deal’ a strategy that could work for Mr Johnson? We see three reasons why it probably won’t.

- While it is probably the PM’s best chance of demonstrating the Irish backstop will not be needed, the backstop will nevertheless remain a part of the deal. And as long as the backstop stays, leaving open the possibility of regulatory diverge between Northern Ireland and the British mainland at some point in the future, the Democratic Unionist Party (DUP) are unlikely to back the agreement.

- Secondly, an extended transition period will require fresh budget commitments for the next EU multiannual financial framework (MFF), which begins at the start of 2021. The idea of paying more money, rather than less, to the EU is unlikely to go down well with the domestic UK audience.

- Thirdly, for many pro-Brexit MPs, an extended transition period would present too much ‘vassalage’ – staying within the single market but without a say in the rules.

All of that means it’s hard to see pro-Brexit Conservative/DUP lawmakers backing such a deal. But as always, the politics matters. If MPs don’t back a revised deal, opposition lawmakers may well succeed in forcing an election to avert ‘no deal’. Some Brexiteers may conclude that it’s safer to ‘swallow’ a lightly-amended deal, and take the fight to the next stage of talks where the ultimate trading relationship will be agreed than it is to fight an election and risk losing control of Brexit altogether.

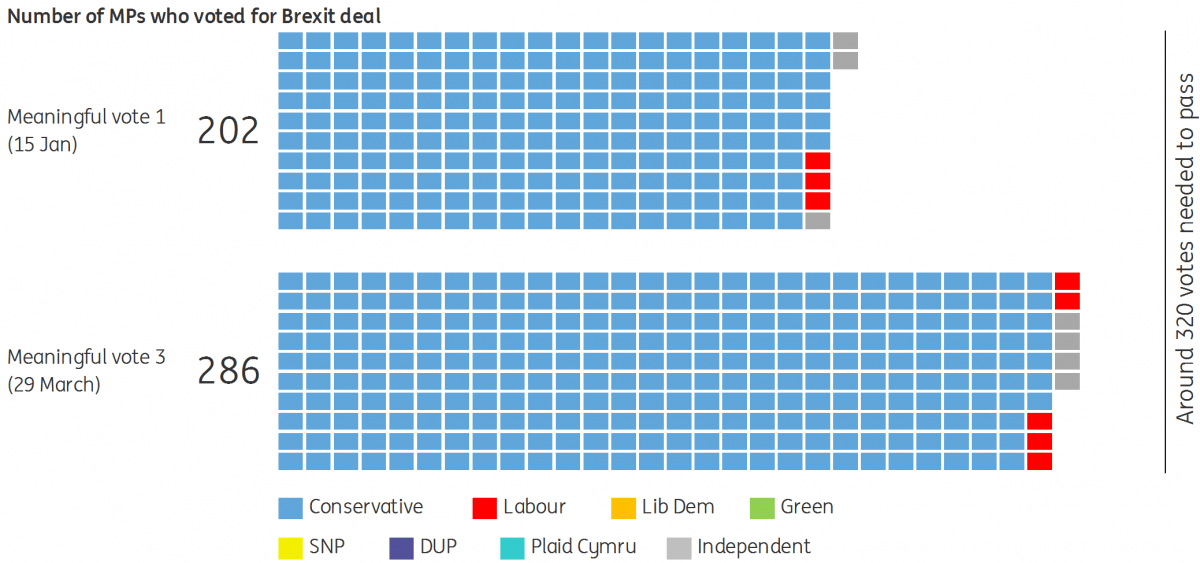

Unlikely as that may sound, something similar actually happened back in March, when a number of pro-Brexit Conservatives voted for the deal in the third meaningful vote, on the basis that Mrs May had committed to resigning her post if the agreement passed. The chart below shows that 81 additional Conservative MPs – including Mr Johnson himself - voted for the deal third-time around at the end of March, than in the initial vote in mid-January.

A number of Brexiteers voted for Mrs May's deal on the third vote

The election numbers look good for Mr Johnson - but can they last?

Our base case is that new negotiations will not prove successful, and this could set up an almighty battle in October as Parliament races to try and prevent the new government pursuing a ‘no deal’ exit. While a 'no deal' is possible (we see a 20% chance at the moment), all of this is more likely to culminate in a no-confidence vote in the government. One way or another, a late 2019 election is getting increasingly likely.

Predicting the outcome of an election is very challenging. But as the polls stand, things are looking good for Mr Johnson. His repeated commitment to get the UK out of the EU one way or another has resonated with many voters.

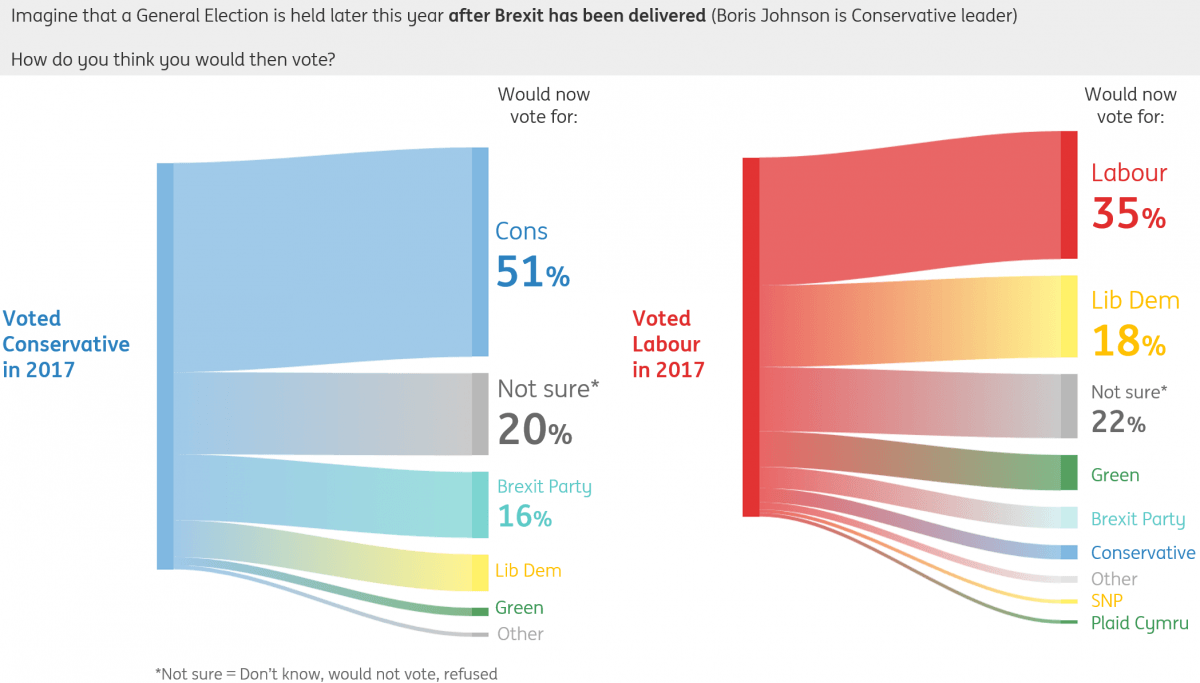

A recent YouGov survey found that around 51% of Conservative voters at the 2017 election (64% if you exclude those that aren’t sure/wouldn’t vote etc.) would vote for Mr Johnson’s party at an election, assuming Brexit is done by then. While that is still a sharp fall compared to the last election, polls suggest Labour would fare worse. Less than half of 2017 Labour voters said they would vote for the party again in a post-Brexit election.

A failure to live up to the promise of achieving Brexit by October would undoubtedly dent Conservative support

Translating all of this back into the UK’s first-past-the-post electoral system is not straightforward, but in theory a Conservative share of the vote of around 30% could translate into a decent result for Mr Johnson. Some commentators have gone as far as to suggest he himself could trigger an election to run on a ‘no deal’ ticket to ‘cash in’ this advantage.

We think that’s unlikely – not least given the lessons of the 2017 election where Mrs May’s polling (which was significantly stronger than Mr Johnson’s is now) failed to translate into a Conservative majority when the public had their say.

But the bigger issue for the new government is that an election – however it comes about – would almost certainly require a further article 50 extension. A failure to live up to the promise of achieving Brexit by October would undoubtedly dent Conservative support. And while the new PM may make a 'no deal' Brexit a formal campaign pledge - potentially shoring up support in key Leave-supporting areas - polling from Hanbury/Politico suggests this could alienate the more centrist Conservative voters in swing seats in areas such as London and Scotland.

It's also worth noting that, while the main opposition Labour Party may not do so well either, the party arguably has a wider pool of potential coalition/confidence and supply partners than the Conservatives. This means a Labour-led coalition is not an inconceivable outcome of a 2019 election, should the Conservatives fail to gain (or come close to) a majority.

Polls suggest a more divided Labour Party than Conservatives at an election

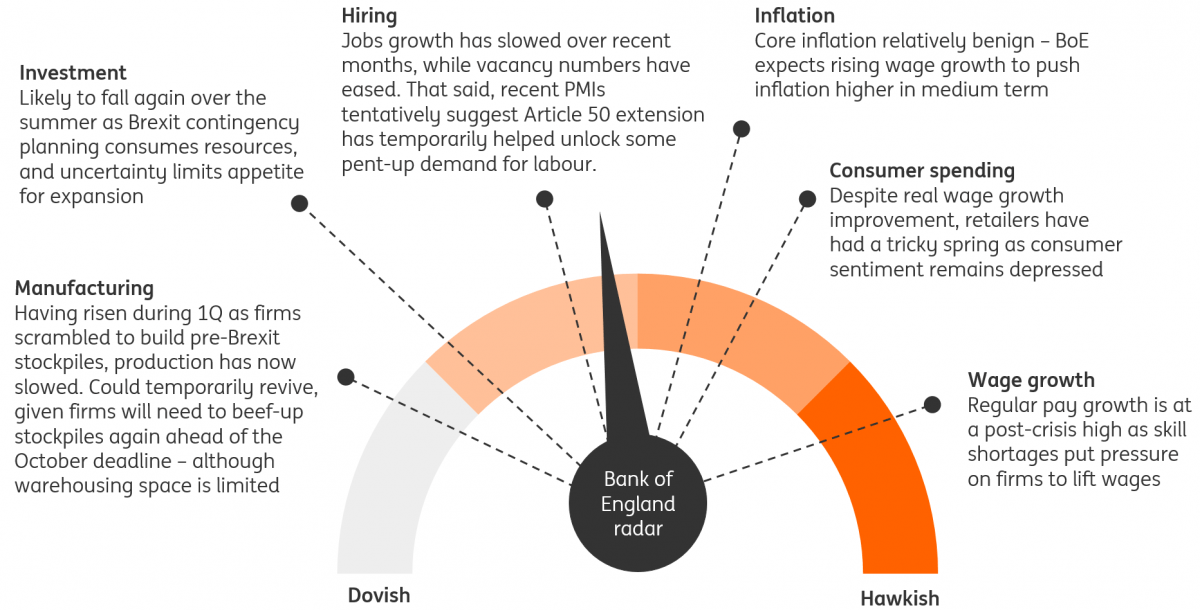

Uncertainty to take its toll on growth, although rate cuts not yet on the horizon

All of this uncertainty will continue to take its toll on growth. The prospect of further declines in investment, coupled with the recent lacklustre retail spending numbers, suggests underlying quarterly growth (once volatile production/inventory numbers are stripped out) will remain capped at around 0.2/0.3% for much of the rest of the year. Benign inflation projections and the prospects of monetary easing abroad have sparked talk of a UK rate cut - markets are pricing a 50% chance of one happening by the end of 2019.

At this stage, we aren't convinced. Wage growth has reached another post-crisis high, and this has been a key a hawkish factor for policymakers over the past couple of years. A lot will depend on Brexit of course, but if an election takes place, or Article 50 is extended to allow more time to break the deadlock, we expect rates to remain on hold for the time being.

However, a further deterioration in UK growth, a significant escalation of global trade tensions, or a 'no deal' Brexit in October, could be catalyst for fresh easing from the BoE.

BoE radar: Investment set to remain a drag on economic activity

Read the original analysis: Brexit and the next 100 days in five charts

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.