Breakout to ATHs – Will it last?

For two weeks at most. S&P 500 led by Nasdaq with semis driven by TSM earnings (AI chips, brought to you Thursday) though decidedly broke above the 4,835 resistance after struggling to break below 4,815, which was the level I gave you in the premium article (breaking which would have invited 4,807 in the least), and also Ellin in our intraday channel.

Market breadth improved with advance-decline line reaching over 1100 (which is for now a lower high vs. recent tops), and the same goes for new highs new lows – this is similar to the daily oscillators bearish divergence I talked on Jan 01, translating into the similarly solid likelihood of stocks shortly entering a soft patch when Friday‘s push higher gets exhausted, Mar rate cuts even more questioned (Waller wasn‘t enough), and following this soft patch dead ahead (whether that comes on GDP Thursday, core PCE Friday, or on the to be hawkishly perceived FOMC the following Wednesday, is a matter of semantics, but my pick is for a wake up call on inflation data Friday).

This soft patch though won‘t be the end of it – as I wrote in another extensive article a week ago, I expect stocks to shake it off, and surge even higher so as to make a top, and then a true correction hits to position stocks for 2H 2024 rally.

As regards yields, they made the top in the 5.10-5.20% region on 10y called, and I don‘t think they would overcome that high. Meandering well below 4.50% before turning down again to finish 1H 2024, seems most likely to me. That‘s in spite of the Treasury needing to raise plenty of new money ($3T for 2024) and refinance old debt, with the „reserve“ in reverse repos growing thin. It‘s a matter of time till they would decide to get some fresh powder and reload, and most likely it‘ll take downside price pressures in equities and bonds to do that (for the Fed as well) – we aren‘t yet close to that though.

That would also coincide with the incoming data – this week‘s set still favored soft landing, but there were a few outliers, notably the unemployment claims beat. Big picture though, manufacturing remains in a recession that I called inevitable already in mid 2022, services are barely growing, and solid retail sales with consumer sentiment can look differently three months from now. Recession is though in no way imminent – real estate won‘tank either thanks to insufficient supply – therefore, watch ISM manufacturing and unemployment to decide on the onset of recession, or its further delay.

Not too hold, not too cold, the economy will be humming along in the coming weeks, but again remember my last week‘s call (not just thanks to Red Sea, and boy and girl, what kind of a week we had there) about (sticky) inflation risks to the upside.

Credit markets

Source: www.stockcharts.com

Some dialing back of rate cuts expectations is still ahead, but more or less, 10y yield is to start levelling off soon, and turn reasonably stable, which would over the near term (as per the stock market writings above) be conducive to the upcoming stock market push driven by shaking off upcoming disappointment over no cut too soon.

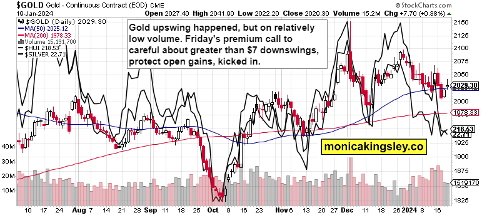

Gold, Silver and Miners

Source: www.stockcharts.com

Gold is entering a cautious phase, and has been really resilient to the weekly push higher in yields. Over the weeks ahead, I‘m looking for more bottom searching since the Fed is going to disappoint the doves.

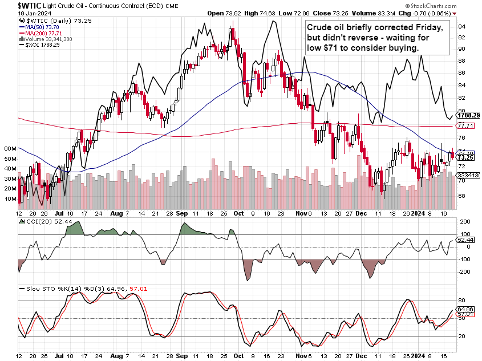

Crude Oil

Source: www.stockcharts.com

Crude oil won‘t correct by too much, and the price risks are to the upside – without geopolitics though, it‘ll be a slow grind higher over the weeks ahead, first $75 and then low $80s.

Copper is turning the corner higher, low $3.70s worked as support again, but remains range bound for now, albeit with a bullish short-term bias.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.