Bond sell-off a knee-jerk reaction to sound bites and slogans

Outlook:

The reason for the wild jump in yields is the expectation of more fiscal stimulus and rising inflation in the US that will bleed over to other countries. It is a classic case of "Sell on the rumor." It's also a classic overshoot--the deflation trade was overdone and now we are seeing the inflation trade get overdone.

The US 10-year note yield, quoted at 2.24% near 8 am ET, is up 44 points over the past month. The Bund yield is 0.36%, or up 31 points over the month. The JGB is quoted at 00.02%, up 4 points. We re-ally wish Bloomberg or somebody would start publishing yield differential charts, which are scarcer than hen's teeth. That the diff is so hard to find doesn't mean it's not a key factor in FX. It is. The 2-year is supposedly more sensitive and there, too, we see the US yield rise greater than in other countries. The US 2-year is quoted at 0.98% while the German version is 0.60%.

We have two questions: at what point has the US yield reached its equilibrium level, and when does eco-nomic reality set in, not only in the US but in Europe? For European yields to rise because the US elect-ed Trump is more than silly. It's unsustainable and dangerous. Yields are supposed to respond to hard domestic economic data, right? Like actual inflation.

The bond sell-off is also a knee-jerk response to sound bites and slogans, and doesn't qualify as decent analysis. Bloomberg reports that Goldman analysts see a real possibility of stagflation of the several sce-narios Trump could bring. "The positive fiscal impulse from his tax reform and infrastructure proposals could provide a near-term boost to growth and, depending on the specifics, could have positive longer-run supply side effects. However, other proposals could lead to new restrictions on foreign trade and immigration, which could have negative implications for growth, particularly over the longer term."

What effect is the election of Trump going to have on capital flows into the US? After all, the US runs a big current account deficit, $119.9 billion as of end-Q2, or 2.6% of GDP. The money to pay for it comes from incoming flows of all sorts, including foreign investment in US and corporate debt and equities, direct investment and plain old cash.

But past data on capital inflows is probably as good a guide to future data as the polls were to the out-come of the election.

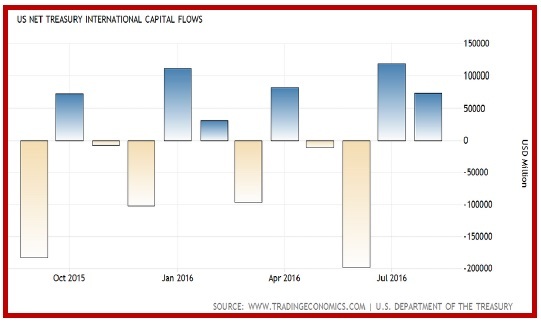

We tried to look at trends in capital flows and immediately got bogged down in vast amounts of data, most of it with incomprehensible labels. The most often-cited data is the TICS report but in practice, the inflow of capital is pretty choppy. See the chart. Also, the data is reported with a big lag, so the best we can do in early November is the August data (we get the Sept data on Nov 16). One of the key numbers in the last report was foreigners buying $48.3 billion in long-term US government and corporate securi-ties. Including the short-term paper, total buying by overseas investors was $73.8 billion in August 2016.

Another popular measure is direct foreign investment (FDI), which showed a cumulative total as of end-2014 is $2.9 trillion, of which 70% comes from European and 13% from Japan, with the lion's share of the European flow from the UK and Netherlands, homes of the shell company. See the chart. What's important about the number is that it's falling, in part on flows to emerging markets, especially China. But again, it's a choppy series.

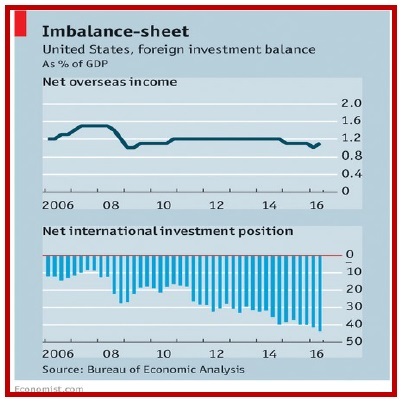

Then there is something named the net international investment position or NIIP. This adds up all the US assets owned by foreigners and subtracts from it all the assets owned overseas by Americans. Ac-cording to The Economist, NIIP has fallen to -44% of GDP, the lowest since records began in 1976, or about 7 times more than any other country. And yet the income from US overseas holdings is still a positive and about 1% of GDP. As The Economist puts it, "Since 1989 foreigners have owned more assets in America than Americans have owned overseas; in the jargon, the net international investment position (NIIP) has been negative. But America is an unusual borrower. For almost all of that time, it has received more income on its overseas investments than it has paid out to foreigners. This is strange: it is akin to someone's savings earning more than enough interest to service his far bigger debts."

How can this be? Well, US investors abroad are yield-seekers while foreign investors in the US just want the perceived safety of the US sovereign—and are willing to pay the taxes to get it. "Between 1990 and 2010 the average yield America received on its foreign direct investments (FDI) was about 6.2 percentage points higher than what it paid out on comparable liabilities."

A lesser argument has it that the world lets the US get away with what would be considered excess debt anywhere else. The French complained in the 1970's that it is due to the US having "exorbitant privi-lege" arising from being the issuer of the reserve currency (and demanded their gold back from storage in the US). The top reserve currency gets a discount on the interest rate it has to pay over non-reserve currency countries.

It's far too delicate an issue to mention political risk. France is not a reserve currency issuer because of shenanigans like serial nationalizations, including the banks in 1981, but nobody likes to mention it. Besides, nobody can really untangle what is reserve currency privilege and what is investments and investment inflows due to the far bigger and more varied menu of options in the US.

Political risk seldom affects yields or flows in the US. Is that going to change with Trump and given the way the data is organized, how will we know it? And do we think Mr. Trump will take the extra three minutes it takes to understand the tricky nuance of the net international investment position? It's not only Mexico at risk. Japan and South Korea are unhappily reviewing the future, too. The press re-ports that Chinese Pres Xi telephoned Trump and told him cooperation is the only way forward.

And according to the WSJ, the one consistent Trump campaign promise is naming China a currency manipulator and using executive authority to impose tariffs. Analysts note that over the past two years, China has been intervening to prevent the yuan from being too weak, the opposite of currency-war ma-nipulation, but mere facts tend not to bother Trump. In a "60 Minutes" TV interview last night, Trump said he had spoken with Pres Obama about N. Korea, among other things. This may have not been a reference to nukes or other foreign policy issues, but rather a reference to China's unwillingness to rein in its client state. Maybe the deal Trump thinks he can make with China is swapping some of the prom-ised tariffs for a more aggressive Chinese control of N. Korea. This is not entirely a bad thing even if it harks back to outdated ideas about international relations—gunboat diplomacy.

A big red light is the appointment of Stephen Bannon as "chief strategist and chief counsellor." Bannon is known for publishing invented conspiracy theories and outright falsehoods to whip up the uneducat-ed and uninformed. His appointment is very bad news for the financial markets.

Political Tidbit: We heard a good one on TV: The first black president, Mr. Obama, was gracious and welcoming to the man who is backed by the Ku Klux Klan. They call this leading by example but we call it downright heroic.

We would bet that the Dems would not have fared so badly if even one financial big shot had gone to jail for the 2008 Crisis. We also bet that the white uneducated Trump voter would not have been so ag-grieved if the past year or two in the news had not been dominated by endless talk about LGBT issues, marriage equality and white cops shooting too many black people.

It may seem ridiculous for white people to feel neglected but and put-upon but not irrelevant to the winning Trump campaign focus on this one specific demographic. In the spring, pollster Nate Silver at 538.com wrote we don't have to worry about Trump because his demographic of angry white blue-collar workers is only about 35-40% of the population.

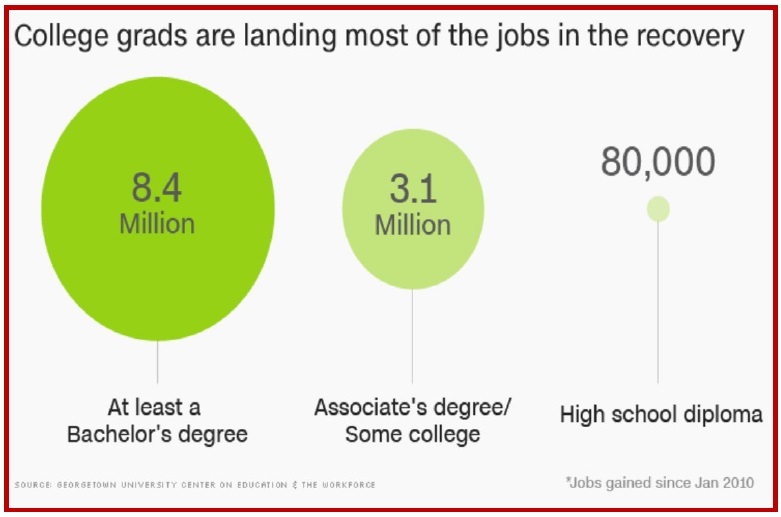

But catch this: One data point that emerged in the great election autopsy: according to a Georgetown University report in June, "Of the 11.6 million jobs created after the Great Recession, 8.4 million went to those with at least a bachelor's degree. Another 3 million went to those with associate's de-grees or some college education." Only 80,000 jobs of all those millions called for a high school di-ploma.

Would the polls have been different if they had considered this data? You bet. And the pollsters are cagey because they have no statistical basis for the judgment, but when asked if Bernie might have beaten Trump, seem to agree that yes, he might well have.

And Trump got two thirds of voters with only a high school education, although he also got a larger than expected chunk of those with a college education, too. The Washington Post is brutal about it: "The reality is that six in 10 Americans do not have a college degree, and they elected Donald Trump. College-educated people didn't just fail to see this coming — they have struggled to display even a ru-dimentary understanding of the worldviews of those who voted for Trump."

Yeah, unfortunately it's a worldview that says we should have saved the buggy-whip maker jobs in the age of the automobile. It's not a classic free-market Republican point of view.

Meanwhile, Attorney General Holder said he is working on a bill to amend the Constitution to get rid of the electoral college and have the popular vote prevail. A petition is being circulated to require VP Biden to demand Trumps' taxes, among other matters relevant to conflict of interest. And Giuliani says Trump will not seek to enrich himself while president and a blind trust is not really necessary—he shouldn't have to fire his own children. Really? He enriched himself at the expense of desperate jobless people who used up savings and ran up credit cards to take courses at Trump University.

Clinton believes the FBI interference in the last 11 days of the campaign contributed to her loss. She is probably right. So did the presence of the third and fourth candidates. Dislike of Clinton was very strong. More qualified than Trump, no doubt. But to a majority, just as unlikeable and untrustworthy as Trump. We probably have to concede that Clinton did not lose because of being a woman. She lost be-cause of Bill, the private server, the suspicion she is in bed with Goldman Sachs, the greed for speech money, the pay-for-play at the Foundation, and the smug self-righteousness that bedevils so many libs.

If Dems stayed home instead of raising her numbers, it's a function of Clinton losing because of per-ceived elitism as well as Trump winning because of perceived populism. Never mind that Trump has never personally known any blue collar workers and wouldn't care to meet any, either—it was a demo-graphic abandoned by the Dems and ripe for the plucking. That Trump got under their skin with racism and xenophobia and sexism is irrelevant, or so the winners think—it was just a ploy to win.

Diehard liberals don't buy it for a minute, hence the street protests all over the country. Comedian Bill Maher had baseball caps made saying "We Are Still Here" and called for "resistance" against Trump-ism. Never underestimate the power of the libs to hold marches and send petitions and generally annoy those who would trample liberal values. They have had a lot of practice since the 1960's.

Unless Trump hires first-class people who keep him under control, we are at risk of a presidency that looks like the campaign—two policy positions in the same sentence, more lies than truthful facts, the failure to observe cultural norms of decency and tolerance, the so-called American values. And that's not even considering the conflicts of interest and how he is going to deal with the Chinese. To be fair, which is hard with the repulsive man, he seemed reasonable enough in a long interview with 60 Minutes on TV Sunday night. But this morning the WSJ has a front-page story on Trump's only con-sistent policy stance of the lot—naming China a currency manipulator and using executive authority to impose tariffs.

| Current | Signal | Signal | Signal | |||

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 107.83 | SHORT USD | STRONG | 11/02/16 | 103.54 | 1.28% |

| GBP/USD | 1.2526 | LONG GBP | NEW*STRONG | 11/04/16 | 1.2489 | 0.30% |

| EUR/USD | 1.0769 | LONG EUR | NEW*STRONG | 11/04/16 | 1.1097 | 1.17% |

| EUR/JPY | 116.13 | LONG EURO | WEAK | 11/03/16 | 114.30 | 1.60% |

| EUR/GBP | 0.8598 | SHORT EURO | NEW*STRONG | 11/14/16 | 0.8598 | 0.00% |

| USD/CHF | 0.9955 | SHORT USD | WEAK | 10/03/16 | 0.9726 | 2.86% |

| USD/CAD | 1.3582 | LONG USD | STRONG | 09/15/16 | 1.3203 | 2.87% |

| NZD/USD | 0.7088 | SHORT NZD | NEW*STRONG | 11/14/16 | 0.7088 | 0.00% |

| AUD/USD | 0.7535 | SHORT AUD | NEW*STRONG | 11/14/16 | 0.7535 | 0.00% |

| AUD/JPY | 81.25 | LONG AUD | STRONG | 10/06/16 | 78.48 | 3.53% |

| USD/MXN | 21.0053 | LONG USD | WEAK | 10/31/16 | 18.6214 | 11.11% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat