BOJ policymakers unwavering on easy policy stance – March meeting minutes

USDINR 77.35 ▲ 0.30%.

EUR/USD 1.0511 ▼ 0.38%.

GBP/USD 1.2286 ▼ 0.41%.

India 10-Year Bond Yield 7.454 ▲ 0.04%.

US 10-Year Bond Yield 3.139 ▲ 0.47%.

ADXY 103.19 ▼ 0.35%.

Brent Oil 112.64 ▲ 0.22%.

Gold 1,875.51 ▼ 0.39%.

NIFTY 50 16,227.25 ▼ 1.12%.

Global developments

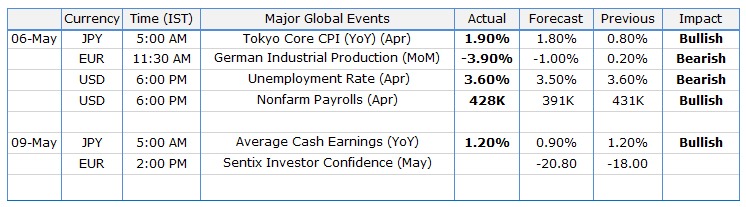

US April headline NFP came in at 428k against expectations of 391k. Other aspects of the jobs report were however not that encouraging. The unemployment rate came in higher than expected at 3.6% (exp 3.5%). Labor force participation declined. Wage growth too came in lower than expected. Labor market strength could be turning a corner. Higher interest rates and a stronger dollar would start hurting fresh hiring.

There seems to be concern among ECB members regarding Euro's recent weakness. A weak Euro further exacerbates inflationary pressures. We have been seeing some verbal intervention. One member said the deposit rate which currently stands at -0.5% could be in positive territory by early 2023.

Price action across assets

US yields continued to climb with the yield on 10y rising to 3.13%. The Dollar has been trading strong. Intermittent short-covering bounces in Euro and Sterling have been short-lived. US equities extended their fall on Friday with Nasdaq dropping another 1.4%. Nasdaq is down more than 23% YTD. Brent continues to remain elevated at USD 112 per barrel.

US April payrolls rise more than expected, wage rises cool.

Domestic developments

USD/INR

The Rupee weakened as a stronger Dollar and higher crude prices weighed. Stops were triggered on the break of 76.75, causing the Rupee to weaken to almost a new all-time low against the Dollar.

Bonds and rates

The Gsec auction went through smoothly. There was no devolvement. However, despite the successful auction, there was a late sell-off with the yield on benchmark 10y ending 5bps higher at 7.45%. FPIs are merely utilizing 29.5% of their available limit in Government securities.

Equities

Nifty ended 1.6% lower on Friday. After RBI's surprise policy tightening, it has been the fragile global risk sentiment that has been weighing on Domestic equities. FPI sell-off continues unabated. FPIs have pulled out a net ~USD 22.5bn in the last eight months.

Strategy

Exporters are advised to cover on upticks towards 77.50. Importers are suggested to cover on dips towards 76.50. The 3M range for USDINR is 74.00–78.00 and the 6M range is 74.50–78.50.

GST receipts may be around Rs 1.5 trillion in May.

FX outlook of the day

USD/INR (Spot: 77.10)

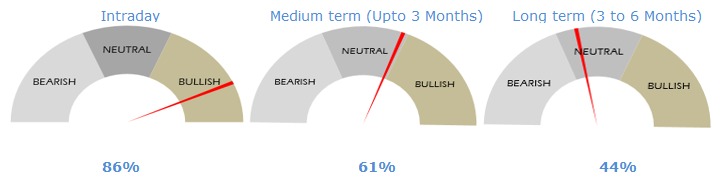

The Rupee weakened as a stronger Dollar and higher crude prices weighed. Stops were triggered on the break of 76.75, causing the Rupee to weaken to almost a new all-time low against the Dollar. US yields continued to climb with the yield on 10y rising to 3.13%. US April headline NFP came in at 428k against expectations of 391k. Labor market strength could be turning a corner. Higher interest rates and a stronger dollar would start hurting fresh hiring. The Dollar has been trading strong globally which is expected to keep the Indian rupee under pressure along with elevated crude oil prices. The pair is expected to trade with a neutral to bullish bias. The intraday range for the pair is expected to be 76.95-77.50.

EUR/USD (Spot: 1.0509)

The EURUSD pair has tumbled below 1.0520 and is likely to test the psychological support at 1.0500. The asset is scaling continuously lower right after the open bid on Monday. Euro bulls are likely to remain volatile this week ahead of the speech from European Central Bank’s Christine Lagarde, which is due on Wednesday. The speech from ECB’s Lagarde will provide insights on the likely monetary policy action by the ECB in June. It is worth noting that the ECB left its interest rates unchanged in its last interest rate decision announcement. The ECB dictated that policy rates will remain unchanged till the end of its bond-buying program, which is expected in the third quarter. Therefore, investors should not brace for a rate hike by the ECB before the end of this year. Also, the fears of stagflation in the eurozone after the Ukraine crisis have eroded the chances of hawkish tone adaptation by the ECB. The pair is expected to trade with a neutral to bearish bias. The intraday range for the pair is expected to be 1.0470-1.0550.

GBP/USD (Spot: 1.2293)

The GBPUSD pair is oscillating in a narrow range as renewed recession fears after the monetary policy announcement by the Bank of England have side-lined investors. The announcement of the monetary policy by BoE Governor Andrew Bailey unveiled a rate hike by 25 basis points with a majority of 6-3. Apart from the rate hike decision, the BoE dictated that inflation will persist for a longer period and it may reach up to 10% by 2024. The households are facing the strong headwinds of higher energy bills and food prices, which are already impacting their real income. And, lower job additions with higher personal expenses are fueling the signs of recession. The pair is expected to trade with a neutral to bearish bias. The intraday range for the pair is expected to be 1.2250-1.2340.

USD/JPY (Spot: 130.87)

The USDJPY pair has failed to deliver any major movement despite the Bank of Japan releasing its monetary policy minutes. The minutes belonged to the monetary policy announced by the BoJ in April last week. The decision came in line with the forecast of -0.1%. The BOJ policymakers adopted a ‘neutral’ stance on the policy rates as the institution is committed to releasing more stimulus packages to spurt the aggregate demand in the economy. The Japanese economy has yet not reached its pre-pandemic growth levels. Also, the inflation rate is very much low in the economy which seeks attention despite a recent rise in energy bills and food prices for the households. The pair is expected to trade with a neutral to bullish bias. The intraday range for the pair is expected to be 130.50- 131.20.

Centre ups scrutiny of borrowings by states.

Economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.