BOE Preview: Three reasons why Carney's last Super Thursday may send GBP/USD down

- The Bank of England may drop its hawkish bias despite the Brexit calm

- The bank's fresh inflation forecasts and the Governor's sentiment will determine market movement

- GBP/USD has more room to the downside than to the upside

Super Thursday is even more super this time – and sterling volatility may surge – while its price may drop. The Bank of England publishes its interest rate, the meeting minutes from that decision, and the Quarterly Inflation Report. What makes this decision even more "super" is that it is the last one led by BOE Governor Mark Carney. Moreover, the forecasts included in the QIR feed into the elections.

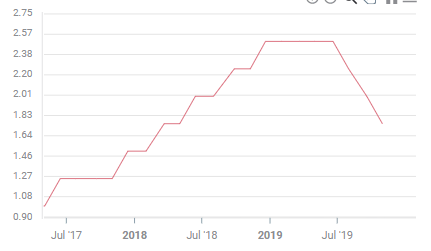

The bank is set to leave the interest rate unchanged at 0.75% and the Asset Purchase Facility – also known as Quantitative Easing – at £435 billion. The meeting minutes are also expected to show a unanimous vote within the nine-strong Monetary Policy Committee (MPC) to refrain from action.

Unless one or two members dissent and either vote for a cut or a hike – an almost non-existent scenario – the focus would be on the QIR's forecasts and Carney's tone.

And that is where the negatives may outweigh the positives despite the relative calm around Brexit.

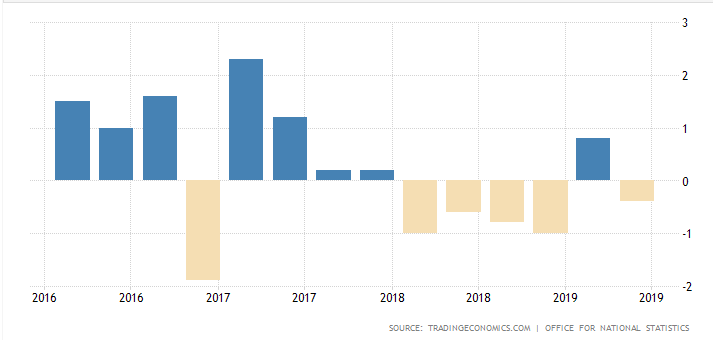

1) Brexit has already bitten

While unemployment remains low, the UK economy is suffering from a slump in investment. The BOE has already warned about this worrying trend – the result of Brexit uncertainty – several times. It is hard to make long-term decisions when the political landscape is changing at a rapid clip. Companies prefer hiring workers – which they can lay off quickly – than invest in machinery the may never pay off due to an uncompetitive environment.

Source: Trading Economics

Growth has been slow and the economy even contracted in the second quarter of the year. While Britain likely returned to expansion in the third quarter, meager growth is on the cards. Fresh figures for the third quarter will only be made available next week, but data from the US, China, and the euro-zone all point to a slowdown. The UK is unlikely to be different, perhaps even worse.

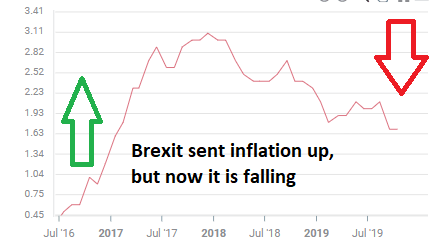

2) Inflation failed to pick up

The "Old Lady" targets an annual Consumer Price Index rate of 2%. When inflation persistently exceeded these levels in 2018, the bank raised rates and signaled more hikes are in the pipeline. However, the data disappointed in the past two months and CPI stands at only 1.7%.

The recent rise of the pound means that imported goods will now be cheaper, further depressing inflation. The QIR includes fresh inflation forecasts and these will likely be downgraded.

An outlook showing weaker CPI may turn into the bank abandoning its hawkish bias – removing the intention to raise rates from its statement.

3) Peer pressure

Last but not least, the BOE is not alone. Slower growth and inflation are global phenomena – and the direction of monetary policy is also shared between different regions.

The Federal Reserve has made a U-turn by cutting interest rates three times this year after hiking as late as December 2017.

The European Central Bank set the deposit rate deeper into negative territory and restarted its bond-buying scheme. Central banks in Canada and Japan have been more dovish while Australia and New Zealand cut rates.

These moves give Carney and his colleagues more reasons to become more dovish – at least for the sake of keeping the pound down and pushing inflation higher.

Three BOE scenarios for GBP/USD

1) Abandoning the hawkish bias: All in all, despite some Brexit certainty and a low unemployment rate, there are good chances that the BOE will abandon its hawkish bias and weigh on sterling.

2) Bias unchanged, lower forecasts: Another possible scenario is for the bank to lower its inflation forecasts but still state that it sees "gradual and limited" hikes down the line. In this case, sterling may shake, but is unlikely to move, as this is the BOE's current policy.

3) No changes at all: The third and most unlikely scenario is for Carney and co. to maintain inflation forecasts unchanged. GBP/USD may rise in response to such potential defiance by the BOE.

As it is the Governor's last post-QIR press-conference, he may feel freer to comment on current conditions and perhaps even share his opinions on Brexit. Carney has been extremely cautious about saying anything that could have been perceived as political. However, his last Super Thursday may be special.

Background: Why the BOE matters for sterling

The Bank of England is responsible for setting interest rates in the UK. The government's target for the bank is 2% annual headline inflation with a band of 1% below or above.

When the BOE raises interest rates, buying sterling becomes more attractive as the money deposited in British bank accounts provides a higher yield. When the London-based institution cuts rates, the pound becomes less attractive.

After the financial crisis broke out, the BOE slashed its interest rates to 0.50% and introduced a bond-buying scheme. GBP/USD tumbled down and never recovered the levels around $2 per £1. The BOE's next move was to cut the rates to 0.25% after Brexit and that sent GBP/USD down from 1.50 to as low as 1.1876 at some point. Higher inflation allowed the bank to raise rates gradually to 0.75%.

Governor Mark Carney, previously leading the Bank of Canada, will leave his post at the end of 2019 after two extensions. His successor is yet to be named. The BOE is waiting for the UK elections on December 12.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.