Benchmarks and Broomsticks: A guide to the upcoming annual changes to jobs data

Summary

Against a slew of souring economic data, the jobs market generally, and nonfarm payrolls in particular, has been a bright spot for the economy.

While the sample size of the establishment survey used to derive nonfarm payrolls estimate is quite large, capturing roughly one-third of establishments, it is nonetheless a sample. Therefore, the Bureau of Labor Statistics routinely benchmarks the level of nonfarm payrolls to more comprehensive measures of employment from employer tax records.

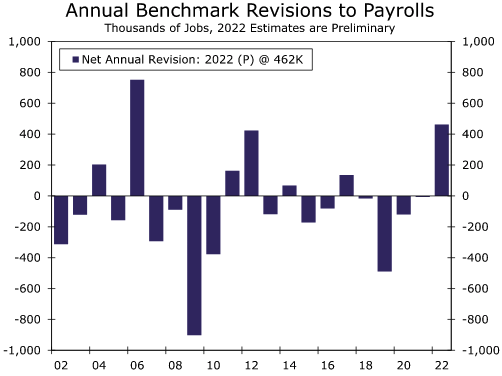

The January jobs report will include revised measures of nonfarm payrolls as part of the annual benchmarking process. Preliminary estimates suggest the level of payrolls in March 2022 will be revised higher by 462,000, or 0.3%.

The benchmarking process, however, will shed little light about how hiring has fared since last March when conditions have grown more challenging with the Fed's aggressive efforts to tamp down inflation. Updated seasonal factors may paint a slightly different picture of the pace of hiring the past few months relative to mid-2022, but it will not be until next year's benchmarking process that we'll see the fuller picture of how nonfarm payrolls have fared under the rapidly changed environment of the past 10 months.

The January jobs report will also include new population controls to the household survey data. As is customary (and unlike the establishment survey), the historical data will not be revised. This can lead to ineffectual month-to-month comparisons of household employment, unemployment and labor force levels. Ratios like the unemployment rate or labor force participation rate should be less affected, but the changes still open the door to some surprising monthly moves.

Will benchmark revisions darken the rosy payroll picture?

A slew of data has pointed to the economy souring of late. It is no longer merely the housing market in retreat, but manufacturing production and consumer spending are now on the back foot. The Leading Economic Index has declined for 10 consecutive months, and with momentum slowing sharply late in Q4, GDP in the first quarter of this year may very well be negative.

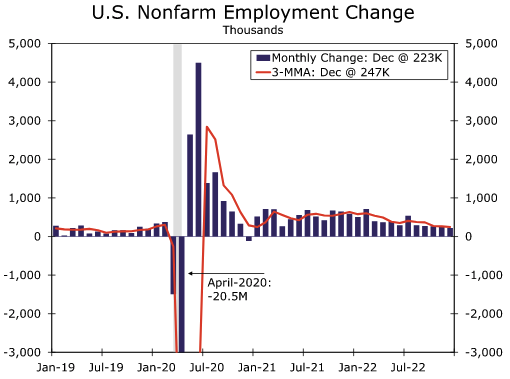

Against the worsening backdrop, the most robust defense against an imminent recession (or rebuttal that the U.S. economy was already in one in the first half of 2022) has been a strong rate of job growth. Nonfarm payrolls, the most ubiquitous measure of employment, expanded by an average of 375,000 per month in 2022. Although hiring slowed to a two-year low in December, payrolls increased by 223,000, or 40,000 more than the 2010-2019 average. We expect the gradual slowdown in payrolls to continue in the near term and look for a 190,000 gain in January's payroll report on Friday. But what if the recent impressive picture of hiring is a mirage?

Source: U.S. Department of Labor and Wells Fargo Economics

Source: U.S. Department of Labor and Wells Fargo Economics

Establishment survey: Timely yet imperfect

Nonfarm payroll estimates are based on a survey of establishments, rather than the entire population of firms. The large sample size—670,000 establishments—captures roughly one-third of all nonfarm jobs and makes it generally preferable to the household survey’s measure of employment, which only covers 60,000 households and therefore has a larger margin of error.

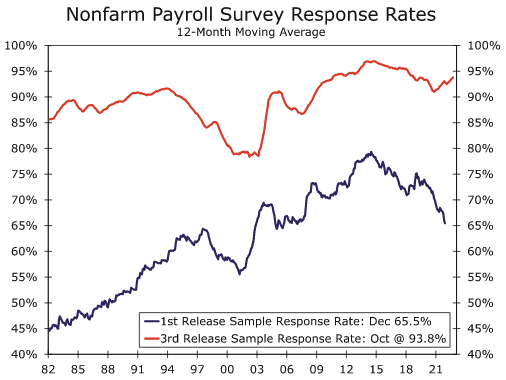

Yet as a survey, it has a number of issues with which to contend. Among them is non-response, which reduces the reliability of a survey’s estimate. The average response rate for the first read on nonfarm payrolls fell to a 17-year low in 2022 (Figure 2). However, the response rate by the third release has trended higher since the early days of COVID and are now not wildly far off from the prevailing rate of the 2010s, suggesting non-response has not been a major issue for 2022's total hiring picture.

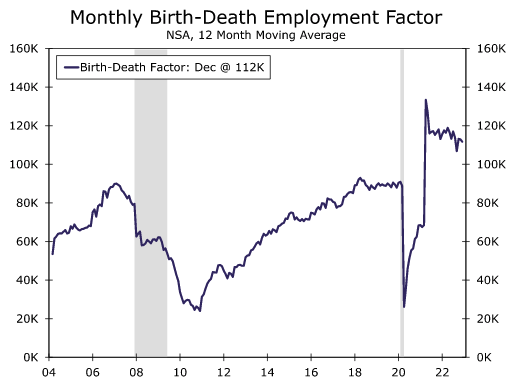

Surveying the wrong mix of establishments (sampling error) is another potential issue, as is the inability to capture jobs created by new firms (non-sampling error). To reduce non-sampling error, the Bureau of Labor Statistics (BLS) forecasts the number of net jobs being created by new businesses (firm "births") not yet captured in the sample. This "birth-death" adjustment scales employment growth up or down depending on the net rate of firm formation. Over the past year, firm formation has been quite strong, helping to lift the forecasted birth-death factor to the monthly level of payrolls to a historically high level.

Source: U.S. Department of Labor and Wells Fargo Economics

Source: U.S. Department of Labor and Wells Fargo Economics

To improve the reliability of payroll survey estimates, each year the BLS benchmarks nonfarm payrolls to more comprehensive measures of employment. The January employment report released on Friday, February 3 will include the annual benchmark revisions, which will adjust the March 2022 level of payrolls with employment counts based on employer tax records for the same period. Preliminary estimates suggest the total level of nonfarm employment was 462,000 higher in March 2022 than currently reported (Figure 4). Put differently, the preliminary benchmark estimates point to the monthly pace of nonfarm job growth being on average 39,000 stronger from April 2021 to March 2022. Over the past 11 years, the absolute change from the benchmark adjustment to the level of nonfarm payrolls has averaged 0.15%, so the 0.3% projected increase would be on the larger side, but not unusually so.

Benchmark revisions already dated

The benchmark revision, however, will have little to say about how hiring has fared in subsequent months. Since March, the operating environment for businesses has become more challenging. With the Fed aggressively tightening policy, inflation rising to a 41-year high and ongoing worker shortages, some skepticism has surfaced that nonfarm payrolls have overstated the true pace of hiring in recent months.

Benchmark revisions showed that when economic conditions began to deteriorate heading into the Great Recession, employment was not as strong as nonfarm payrolls indicated at the time (Figure 4). Concerns that actual hiring may similarly be weaker today than indicated by current nonfarm payrolls have also been fueled by a recent report by the Federal Reserve Bank of Philadelphia. The analysis estimated that in Q2-2022 (beyond the period in which the upcoming annual payroll benchmarks will cover), a mere 10,500 jobs were added compared to the 1.1 million reported by the current payroll figures.

The Philadelphia Fed’s estimates, however, have only been reported for a few quarters now and are based on less complete data than the BLS uses. The authors suggest some caution in taking them as gospel of future national revisions, noting that it would take large revisions over three quarters to suggest the national revisions would be revised even slightly in the same direction of the state revisions. The research notes “we need to track this work over more years to learn whether our early benchmarks regularly predict the direction of data revisions to the CES estimates of national data.” Given the lagged incorporation of revisions, it will not be until next year's benchmarking process we see the fuller picture of how nonfarm payrolls have fared under the rapidly changing environment of the past 10 months.

Other changes to the establishment and household survey

To the extent the January Employment Situation's adjustments to the establishment survey do end up altering the recent picture of hiring, it would be more likely to come from the updated seasonal factors. Changes to seasonal factors for the past five years could potentially show a steadier pace of job growth in recent months, or alternatively that hiring has lost momentum more quickly.

Not to be left out, the household survey will use new population controls to reflect the latest population estimates from the Census Bureau. Unlike the establishment survey, however, historical data are not revised. This can lead to ineffectual month-to-month comparisons of household employment, unemployment and labor force levels. Monthly comparisons of ratios such as the unemployment rate or labor force participation should be less fraught as both the numerator and denominator are subject to the adjustments, but the lack of revisions to prior data nonetheless ushers in the potential for some surprising monthly moves.

Author

Wells Fargo Research Team

Wells Fargo