Banker's Big Bang theory

Era of Quantitative Easing (QE)…

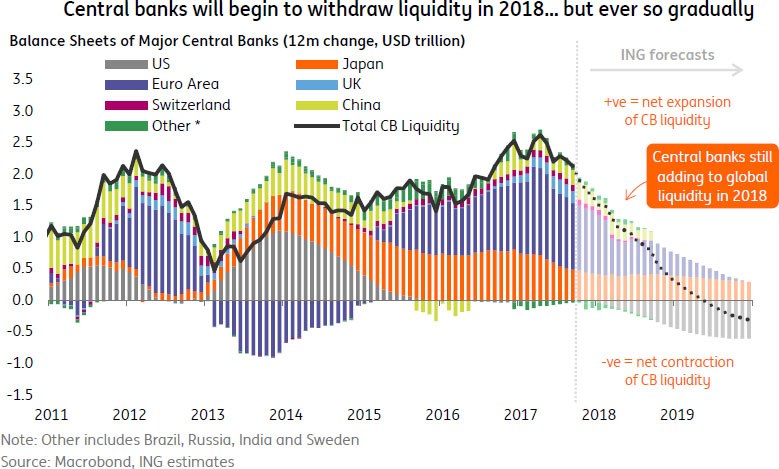

Over the last decade central banks have had a significant impact on financial markets as their adoption of aggressively accommodative monetary policy, via quantitative easing, has seen trillions of dollars injected into the financial system. The era of central bank bond buying that has sent prices of government and corporate debt soaring since the 2008-09 financial crises is set to reach a turning point this year, after policymakers sketched out plans last year to rein in stimulus measures.

When the Federal Reserve began to unwind its bond-buying programme, the Bank of Japan cranked up its even grander quantitative easing scheme. By the time the Fed started raising interest rates, the European Central Bank had unveiled its own monetary programme (LTRO). BoE raised rates for the first time in nearly a decade from 0.25 percent to 0.5 percent but kept easing program unchanged.

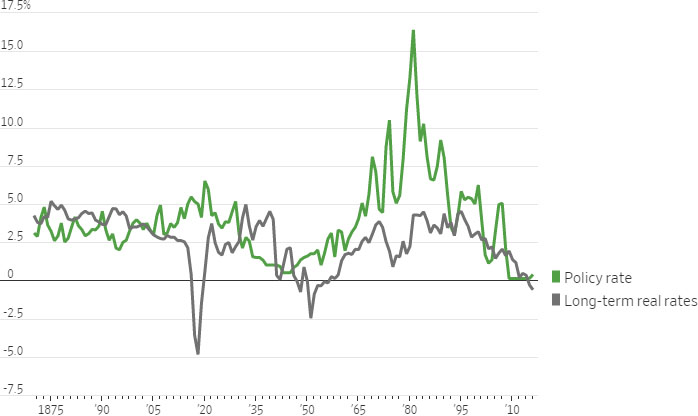

If longer-term rates suddenly rose, that could stop chasing risk-on trades in stock markets that have been hitting repeated new highs. The fact longer-term yields- especially “real” ones that are inflation indexed have stayed low have helped push money into risky assets because investors get little extra purchasing power for holding safer securities (Flight of money from fixed to risky asset classes).

Subdued real rates have been main drive in 2017 of returns in other emerging markets and especially into equity and debt markets. Low real rates also boost Yellow metal- gold demand and real estate too, which don’t pay coupons but don’t lose value when inflation rises.

Bumpy Road Ahead…..

So far, those longer-term rates have remained subtle, even as the U.S. Federal Reserve increased short-term rates three times in 2017 and other central banks (ECB, BoE and BoJ) signals that the era of super-easy monetary policy may soon come to an end.

While Central Banks would like to reverse their earlier accommodative monetary policy, the current scenario doesn’t favor them to act aggressively. Hence, Investors are cheering by a booming global economy and the promise of central banks to tighten monetary policy only gradually.

Indeed, the yield curve - the yield gap between short and long-term Treasuries is now at its flattest since 2007, and many investors underscore that, in the past, this has often preceded an economic slowdown in the U.S. Hence the possibility of tightening monetary policy is reduced in most of the regions.

Key challenges ahead of central banks….

US is associated with the new Administration. If US cut taxes is a part of a looser fiscal policy, then they should be prepared to have a tighter monetary policy to offset it. The US is stumbling towards the most substantial tax reforms for more than 30 years, but while some sort of reform is welcome, the timing is worrying. One really should not be boosting the economy when it is close to full capacity. The electoral cycle and the economic cycle get misaligned.

In Europe, concerns about the effect of the end of European QE, arguing that the ECB’s exit from bond markets is the single biggest risk facing global markets in 2018, given how the Eurozone’s bond purchases have sent money flowing everywhere. As the ECB slows and ultimately ends QE in 2018, the amount of cash flowing to risky assets such as credit and equities will slow down and ultimately dry up altogether.

In UK, everything seems interlinked with Brexit talk and negotiation, it is almost impossible to discuss the economy without attaching a “despite Brexit” or “because of Brexit” label.

The Bank of Japan is seen as the last grown-up in the room actively filling the global liquidity punch bowl with both hands. On last Tuesday, the BOJ modestly trimmed its purchases of Japanese government bonds by about $10 billion in the 10- to 25-year maturities and another $10 billion in maturities of more than 25 years. But they are still buying ETFs, J-REITs and corporate paper. Things are still not clear for BoJ.

Despite the ongoing rate hikes and balance sheet normalization in advanced economies led by the Fed, most Asian central banks are maintaining status quo interest rates except the Hong Kong Monetary Authority and Bank of Korea. Softer future inflation expectation and therefore real rates- could be major concerns in front of central bankers. This has been and this will be supporting factors for Asian markets in 2018.

Amidst this one thing is continuously increasing is LIBOR, which is reflective of short term rates in the economy. Libor which serves as the basis for trillions of dollars in loans, would increase the borrowing cost for the Corporate. With increasing short terms but long term rates being unchanged, the road ahead could be very bumpy for the Central Bankers to have a decisive monetary policy.

In nutshell, 2018 could be a challenging year for central banks to do a balancing act - Normalizing the balance sheet and tightening the monetary policy amongst softer inflation & growth concerns and at the same time not spook investors’ sentiment which has improved now after a long time since 2008 recession.

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.