Bad news for Bonds: An Oil shock could break the safe-haven playbook

A dramatic escalation of geopolitical tensions in the Middle East puts bond investors in a dilemma. In normal circumstances, investors would rush into US Treasuries, pushing prices higher and yields lower, in a classic flight to safety. Not this time.

US Treasuries play a unique role in the global financial system, serving as the de facto risk-free asset due to their extreme safety and liquidity. The usual playbook, however, isn't working now as a spike in Oil prices raised worries that inflationary pressures could accelerate again and force the US Federal Reserve to slow or scale back its plan to cut interest rates further.

Higher Oil prices don’t bode well for almost anyone

Crude Oil prices surged to the highest level since June 2025 on fears of a widening conflict and the effective closure of the Strait of Hormuz.

-1772529538510-1772529538514.png)

The key question here is by how much Oil prices could rise and for how long. US President Donald Trump stated that the US military operation in Iran could take four to five weeks, and more strikes would continue for as long as necessary, underscoring the risk of a prolonged war in the key oil-producing region. It’s hard to know the ultimate goal of the US administration, but one thing is clear: the longer the war lasts, the worse the energy shock is likely to be.

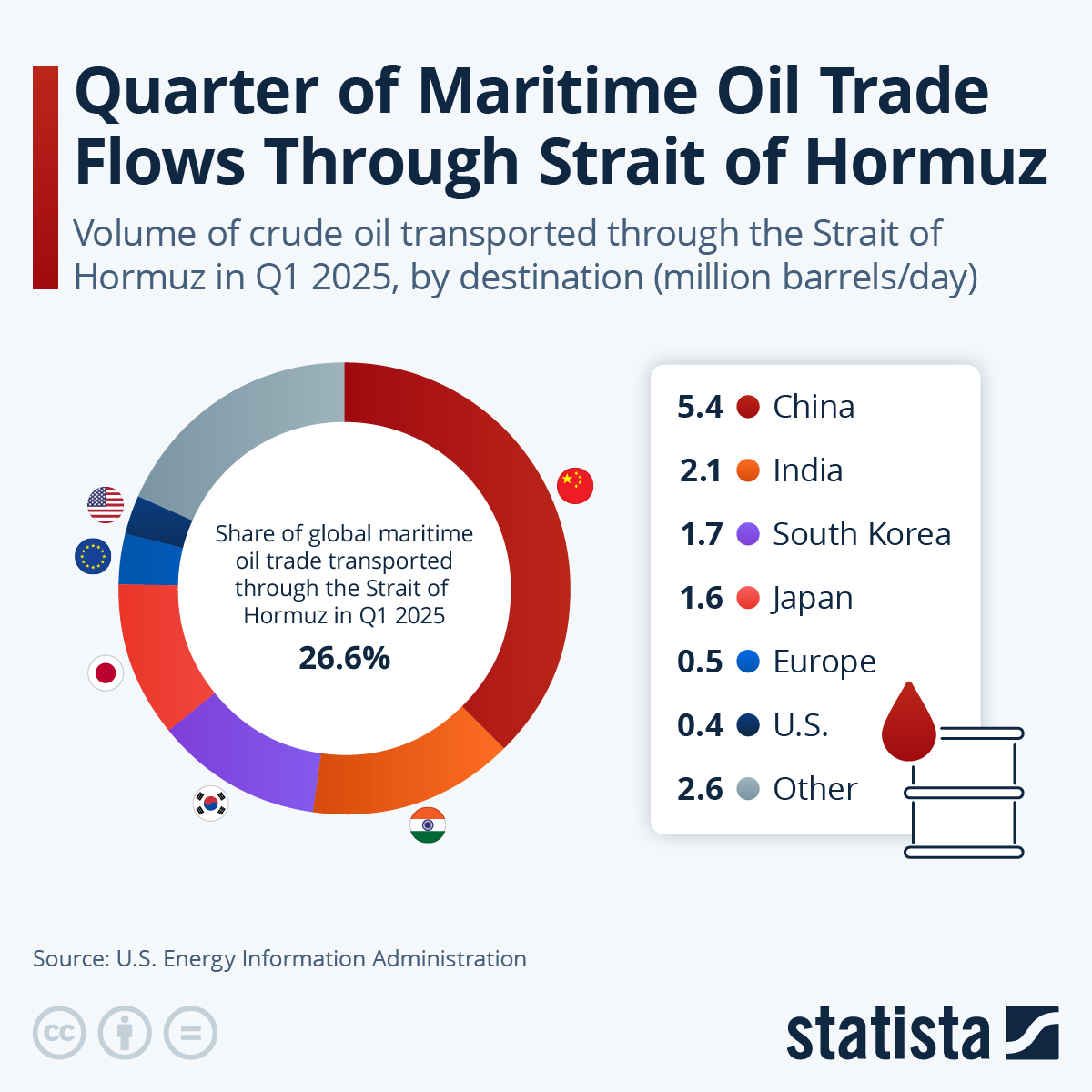

The Hormuz question

The other question is what happens in the Strait of Hormuz. Iran’s Islamic Revolutionary Guard Corps (IRGC) announced that the strait is closed for shipping traffic and warned that any vessel attempting to pass through the strategic waterway would be set on fire.

The Strait of Hormuz is one of the world’s most critical oil transit routes, with roughly 20% of global supplies passing through it. Any disruptions there will further send Crude prices soaring.

Moreover, Iran has targeted infrastructure critical to the world’s energy production as part of its retaliation and warned that it will not allow a single drop of Oil to leave the region, fueling fears of a fresh energy crisis that could ramp up inflation.

Expensive Oil means fewer Fed rate cuts and more borrowing

The sharp moves in Oil have driven a significant spike in sovereign bond yields. This is because investors are quickly pricing in that a prolonged increase in Oil prices would filter through inflation.

Market participants had already trimmed their bets for three Fed rate cuts this year following the release of the producer inflation data that signaled that price pressures remain deeply entrenched within the American economy. And that was before the Middle East war broke out.

-1772529625262-1772529625264.png)

The prices paid component of the ISM Manufacturing PMI, a survey gauging how US factories are doing, surged to 70.5 in February, its strongest reading since June 2022. This broadly means that the vast majority of manufacturing firms polled saw input prices increase recently. This also raises questions about whether the Fed will be able to cut rates at the pace that markets had been pricing.

There’s also the risk of excessive government borrowing as efforts to shield households and businesses from rising energy costs could increase bond supply. This should keep the benchmark 10-year US bond yield closer to or above the 4% important psychological threshold.

In conclusion, very few countries would benefit from a prolonged spike in Oil prices, and the US isn’t one of them. Bond investors know that, and they don’t like it.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.