Australian Dollar Price Forecast: Upside remains capped by 0.7100

- AUD/USD resumes its upside momentum, retargeting the 0.7100 region.

- The US Dollar trades with marginal gains amid steady jitters in the Middle East.

- Investors remain focused on rising effervescence in the Strait of Hormuz.

The Aussie Dollar's continuous rebound seems to have strengthened in the last few days, giving bulls back control and paving the way for AUD/USD to perhaps test the upper end of its annual range sooner rather than later. For now, the pair’s positive outlook should stay strong since inflation in Australia is still high and the RBA keeps its hawkish stance in place.

The Australian Dollar (AUD) sets aside Friday’s pullback and regains upside traction in quite a positive start to the week, sending AUD/USD to the upper 0.7000s following the mixed tone in the risk-linked universe.

Indeed, the US Dollar (USD) now trades with modest gains, surrendering most of its earlier advance as investors continue to evaluate the crisis in the Middle East after US-Iran peace talks broke down over the weekend and President Trump announced the US Navy is ready to blockade Iranian ports.

Following these events, crude oil prices advance markedly, once again stoking concerns surrounding global inflation.

Australia: still resilient, but momentum is softening

Australia's economic story remains largely optimistic, bolstered by robust internal dynamics. However, we're seeing initial indications that the current cycle has been losing some of its impulse.

Overall, the situation hasn't shifted dramatically: the economy is still outperforming a lot of its counterparts, inflation is stubbornly high in several crucial areas, and the Reserve Bank of Australia (RBA) is maintaining a careful, data-driven approach following its recent couple of rate hikes.

That being the case, some signs of strain are emerging: the March Purchasing Managers’ Index (PMI) figures for both manufacturing and services dipped below the 50 mark, suggesting a slowdown in domestic activity.

On a brighter side, February's trade surplus swelled to A$5.686 billion, marking the most substantial figure since the middle of 2025. In addition, growth remains robust. Indeed, the economy saw a 0.8% QoQ expansion in Q4 2025, translating to a 2.6% annual gain as per the Gross Domestic Product (GDP data. The job market, though still relatively strong, is displaying early indications of a slowdown. On this, the Unemployment Rate ticked up to 4.3% in February, even as the Employment Change climbed by almost 49K individuals.

However, inflation continues to be the primary hurdle. The latest Consumer Price Index (CPI) showed a rise of 3.7% YoY, while the Trimmed Mean clocked in at 3.3% YoY, and the Weighted Median rose 3.5% from a year earlier. All in all, disinflation is underway, though its progress is slower than many had hoped.

Considering this, the RBA isn't signalling a conclusion to its efforts. They've indicated that inflation could remain above their target until around the midpoint of 2028.

China: more of a stabiliser than a growth engine

China is no longer giving the Aussie a real boost, but it is still doing enough to keep the backdrop from deteriorating.

The numbers still look good, at least at first glance. the economy expanded by an annualised 4.5% in Q4 2025, and Retail Sales rose by 2.8% YoY over the first two months of the year. Trade is also ticking along, with the February trade balance coming in just above $90.00 billion.

That split is clear in the business activity data after official figures from the National Bureau of Statistics (NBS) still show activity in contraction territory, while private surveys like RatingDog remain in expansion, even if momentum cooled a touch in March.

Inflation sits somewhere in between, as the CPI rose 1.2% YoY in February, while Producer Prices stayed in deflation at -0.9% over the past year.

All in, China looks more like a stabilising force than a true growth engine. Against that backdrop, the People’s Bank of China (PBoC) is likely to stay on hold, with Loan Prime Rates (LPR) expected to remain unchanged at 3.00% and 3.50% at the next meeting.

RBA: tightening bias intact, but the timing is up for debate

The RBA delivered a very tight call at its latest meeting, with a 5–4 split in favour of a 25 basis points hike, taking the Official Cash Rate (OCR) to 4.10%, matching initial estimates. That alone tells you how divided the board has become.

That said, the core message hasn’t really changed, as capacity constraints are still biting, and higher crude oil prices are likely to keep near-term inflation pressure alive. In her press conference, Governor Michele Bullock was quite clear on that front, arguing that demand is still running too strong for comfort.

Where the debate is shifting is around timing, as certain officials seem to be adopting a more cautious approach, making an impasse to assess the current situation. This pause is likely influenced by the unpredictable global environment and the delayed effects of previous monetary policy changes.

The latest Minutes capture that more circumspect mood. Indeed, it does look that the economic horizon is less certain at the moment, with international events injecting further unpredictability into the policy decisions ahead.

Market sentiment currently leans toward more tightening, with just over 60 basis points of additional tightening already pencilled in by year-end.

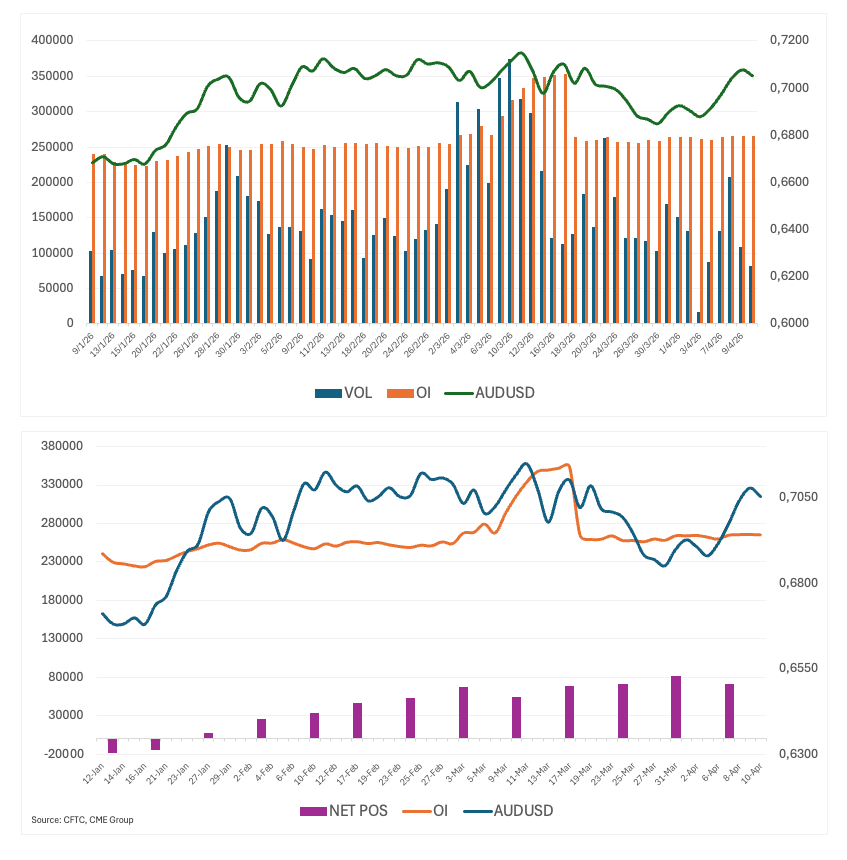

AUD positioning: longs easing, but still crowded

The AUD continues to hold a strong net long position, even though the most recent speculative data indicates a slight decrease in this positioning for the week ended on April 7. Indeed, non-commercial net longs have edged lower to around 70K contracts, suggesting some trimming of bullish exposure after the extended build-up seen in prior weeks.

Price action, however, continues to lean soft. AUD/USD has drifted further lower toward the 0.6970 area during that period, reinforcing the divergence that has characterised the pair in recent weeks, where positioning remains constructive but price fails to confirm.

Additionally, open interest has declined slightly, pointing to some positions being closed rather than aggressively reversed. This points to a measured scaling back of long positions, rather than a complete reversal.

The Aussie, therefore, remains exposed: though the modest trimming of longs eases some short-term pressure, overall positioning is still high and doesn't reflect current market conditions. Without a turnaround in the wider economy, the possibility of further long liquidations remains, particularly given the Greenback current strength.

AUD/USD outlook: the rally is there; conviction still isn’t

Base case, cautiously constructive:

Spot is currently trading within the 0.7000–0.7100 range, always looking at the geopolitical backdrop. However, the upward movement could begin to stall as it approaches the key resistance zone around 0.7100. This is contingent on the US Dollar not gaining traction and the overall risk environment not deteriorating.

Bull case, needs confirmation:

To keep this rally going, the market needs to show some real belief. If risk appetite continues to improve, then spot could break above 0.7100 with some conviction, setting the next milestone at 0.7200 while reinforcing the constructive outlook at the same time.

Bear case, risks still there:

However, the potential for a reversal should not be ruled out in case the current sentiment sours, the Greenback picks up pace, or Chinese fundamentals deteriorate. A drop below the 0.7000 yardstick would probably trigger a deeper retracement, potentially targeting the 0.6900 region.

The rally is real, but it still feels fragile. Markets need stronger conviction to keep it going.

What matters for AUD/USD now

Near term: the US dollar, general risk mood, and any new geopolitical news will still be the major drivers. Later this week, Westpac's Consumer Confidence gauge will be the only event of note in Oz. However, all the attention is expected to be on the publication of key Chinese data, including GDP figures, Balance of Trade, Retail Sales and Industrial Production.

Risks: a slowdown in the Chinese economy, a more aggressive Federal Reserve (Fed), or any change in the RBA's position may quickly make the Aussie unstable.

Technical corner

In the daily chart, AUD/USD trades at 0.7063, retaining a constructive bullish bias as it holds above the 55-day simple moving average (SMA) at 0.7028 and the 100-day SMA at 0.6867, with the 200-day SMA down at 0.6701 reinforcing the broader uptrend structure. The 14-day Relative Strength Index around 57 suggests positive but not overextended momentum, while a subdued Average Directional Index near 21 hints at a modestly trending market rather than a strong directional impulse.

On the topside, initial resistance emerges at the 0.7188 area, where a key Fibonacci anchor and a horizontal barrier coincide, ahead of further caps at 0.7283 and 0.7661. On the downside, immediate support is seen at the 0.7028 zone, backed closely by the 23.6% Fibonacci retracement at 0.7007, with deeper demand expected near the 0.6895–0.6867 band that combines the 38.2% retracement and the 100-day SMA, before the 200-day SMA and horizontal support cluster between roughly 0.6714 and 0.6660.

(The technical analysis of this story was written with the help of an AI tool.)

Bottom line: constructive, but not quite there yet

The overall picture for the Australian Dollar remains strong, and the RBA isn't likely to change its position in the near future, which should maintain a floor against occasional bouts of selling pressure.

Furthermore, the Australian currency thrives when investors are feeling confident, but when things get shaky, the Greenback is often the one regaining its footing. Consequently, despite a generally favourable long-term view, the immediate future is still somewhat unpredictable.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.