Australian Dollar Price Forecast: Next on the upside… the moon?

- AUD/USD surpasses the 0.6900 hurdle with certain conviction on Monday.

- The US Dollar remains on the back foot, weighed down by BoJ intervention talks.

- The Australian inflation data could prove to be key for next week’s RBA meeting.

AUD/USD keeps its positive streak well and sound so far, opening the door to a potential challenge of the key 0.7000 threshold in the short-term horizon, always on the back of USD weakness, widespread improvement in the risk-associated universe and prospects that the RBA could soon embark on another tightening cycle.

The Australian Dollar (AUD) kicks off the week on the front foot, with its ongoing uptrend showing little sign of losing impulse. That is pushing AUD/USD to a sixth straight daily gain and, notably, back above the 0.6900 mark for the first time since October 2024.

This move is almost entirely a US Dollar (USD) story. Broad-based weakness in the Greenback, helped by an improving risk mood, continues to do the heavy lifting. Investor sentiment remains upbeat following Trump’s comments in Davos last week, while tensions linked to Greenland have also cooled, removing another layer of support for the USD.

Australia: easing momentum, steady footing

Australia’s latest data haven’t exactly set pulses racing, but they don’t point to trouble either. Momentum remains steady, yes, but the broader picture still looks very much like a soft landing.

That theme is echoed in January’s Purchasing Managers’ Index (PMI) figures, as both Manufacturing and Services improved and stayed comfortably in expansionary territory, at 52.4 and 56.0 respectively. Retail Sales are holding up reasonably well, and while the trade surplus narrowed to A$2.936 billion in November, it remains firmly in the black.

Economic growth is cooling, though only gradually. Indeed, Gross Domestic Product (GDP) expanded by 0.4% QoQ in the July–September period, easing from 0.7% previously. On a yearly basis, the GDP held steady at 2.1%, matching the Reserve Bank of Australia (RBA) projections.

The labour market continues to be a bright spot. Employment jumped by 65.2K in December, and the Unemployment Rate unexpectedly edged lower to 4.1% from 4.3%.

Inflation remains the most awkward part of the story. Progress is there, but it’s slow. Headline Consumer Price Index (CPI) inflation eased to 3.4% in November, while the trimmed mean slipped to 3.2%, still above the RBA’s target range. One small positive came from the Melbourne Institute survey, where consumer inflation expectations ticked down to 4.6% from 4.7%.

China: support without fireworks

China is still offering underlying support to the AUD, just not with the punch seen in earlier cycles.

The economy grew at an annualised pace of 4.5% in the October–December quarter, with quarterly growth at 1.2%. Retail Sales rose 0.9% in a year to December. Solid numbers, but not the sort that tend to ignite sharp AUD rallies.

More recent indicators point to stabilisation: Both the official Manufacturing PMI and the Caixin index nudged back into expansion at 50.1 in December. Services activity also improved, with the non-manufacturing PMI at 50.2 and the Caixin Services PMI holding at a healthy 52.0.

Trade was the standout. The surplus widened to $114.1 billion in December, driven by nearly a 7% jump in exports and a robust 5.7% increase in imports.

Inflation remains mixed. CPI inflation was unchanged at 0.8% year-on-year in December, while Producer Price Index (PPI) inflation stayed negative at -1.9%, highlighting that deflationary pressures haven’t fully faded.

For now, the People’s Bank of China (PBoc) is sticking to a cautious approach: Loan Prime Rates (LPR) were left unchanged earlier in January at 3.00% for the one-year and 3.50% for the five-year, reinforcing expectations that policy support will remain gradual rather than forceful.

RBA: comfortable holding the line

The RBA struck a firm tone at its December meeting, leaving its Official Cash Rate (OCR) unchanged at 3.60% and signalling no real urgency to adjust policy.

Governor Michele Bullock pushed back against expectations for near-term rate cuts, making it clear the Board is comfortable keeping rates higher for longer and is prepared to tighten further if inflation refuses to cooperate.

The December meeting Minutes added some nuance, revealing debate around whether financial conditions are restrictive enough. That discussion keeps rate cuts firmly in the “not guaranteed” bucket.

Attention now turns to the fourth-quarter trimmed mean CPI print later this week, which could be a key input into the next phase of the policy debate.

Even so, markets are currently pricing roughly a 63% probability of a rate hike at the February 3 meeting, with close to 70 basis points of tightening priced in by year end.

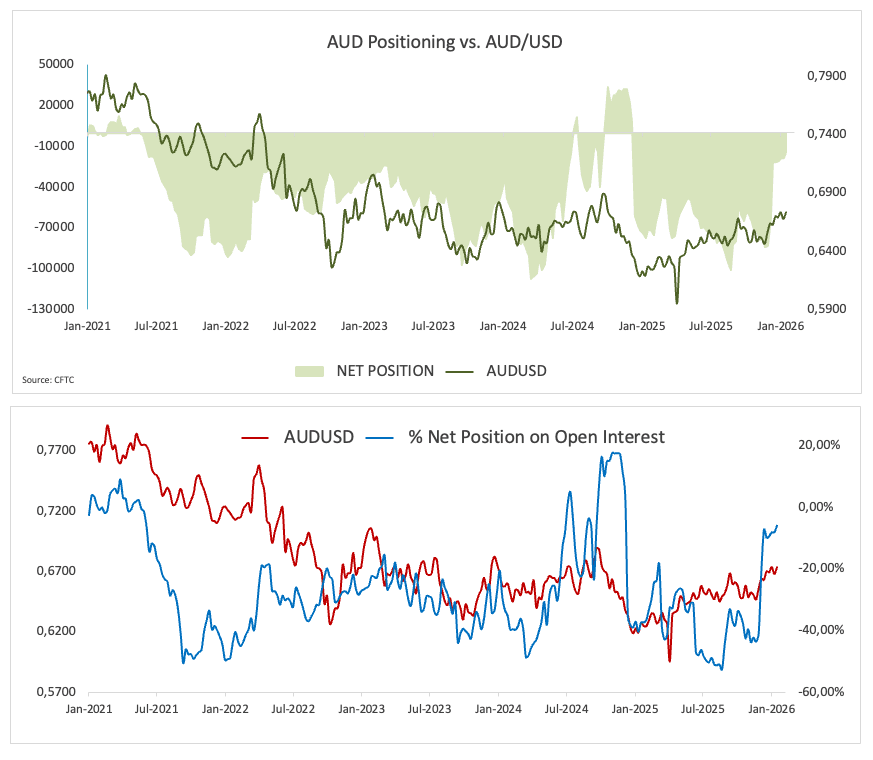

Positioning: pressure easing, optimism tentative

Positioning data hint that the worst of the bearish mood may be behind us, although conviction remains thin. Commodity Futures Trading Commission (CFTC) data for the week ending January 20 show speculative net short positions in the AUD trimmed to around 14K contracts, the least negative reading since late September 2024.

Open interest has also picked up, rising to roughly 230.6K contracts. That suggests some fresh engagement, but overall the picture still leans more towards caution than outright bullish enthusiasm.

What could tip the balance next

Near term: US data releases, tariff-related headlines and the upcoming Fed meeting are likely to dominate the USD side of the equation. Domestically, the January 28 inflation data will be the key release ahead of next week’s RBA rate decision.

Risks: The AUD remains highly sensitive to global risk sentiment. Any sharp risk-off shift, renewed concerns around China, or a stronger-than-expected rebound in the USD could quickly cap further gains.

Technical landscape

AUD/USD bullish move looks unstoppable for now. However, as the pair further enter into the overbought lands, the idea of a technical correction is expected to gather traction.

Next on tap comes the 0.7000 threshold, while the break above this level should meet the next hurdle of relevance not before the 2023 ceiling at 0.7157 (February 2).

Speaking about the likelihood of a corrective move, the so far 2026 bottom at 0.6663 (January 9) emerges as an immediate, albeit minor, contention. Down from here comes the weekly trough at 0.6592 (December 18), a level reinforced by the proximity of the temporary 55-day and 100-day SMAs in the 0.6630-0.6600 band. A deeper drop could prompt spot to challenge its critical 200-day SMA at 0.6542 ahead of the November floor at 0.6421 (November 21).

Looking at the broader picture, further gains are likely while above its 200-week and 200-day SMAs at 0.6618 and 0.6542.

In the meantime, momentum indicators look bullish, with caution: the Relative Strength Index (RSI) remains well overbought mnear the 80 level, while the Average Directional Index (ADX) past 37 suggests a robust trend.

-1769445012093-1769445012098.png&w=1536&q=95)

Bottom line

AUD/USD remains closely tied to global risk sentiment and China’s economic trajectory. A sustained break above 0.7000 would be needed to send a clearer bullish signal.

For now, a choppy USD, steady, if unspectacular, domestic data, an RBA planning on start tightening its monetary policy, and modest backing from China keep the bias skewed towards further gains.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.