August central bank overview

Major central bank rundown

The central banks are listed below with their current state of play. The link for each central bank is included in the title of the bank and the next scheduled meeting is in the title too.

Reserve Bank of Australia, Governor Phillip Lowe, 0.10%, meets August 03

Faster than expected economic recovery

On the face of it, there was not much change in July. No rate hikes are expected until actual inflation is within the 2-3% range and supportive monetary conditions (low rates etc) are to be maintained in order to support a return to full employment and for inflation to be consistent with this target. The labour market is still, like June’s meeting, not expected to be tight enough to spur higher age growth (and therefore inflation with it) until 2024. The economic recovery is still regarded as ‘stronger than earlier expected and is forecast to continue’. The three-year yield target remained the same keeping to the April 2024 bond as its 3-year yield target instead of pushing it further down the line to the November 2024 bond. Bond purchases were extended until mid-November but reduced by $1 billion a week. So, a more confident meeting on balance from the RBA.

The takeaway

The central scenario remains that the condition for a lift in the cash rate will not be met until 2024. The data the RBA want to see is inflation in the 2-3% range and spurred on by wages growth that exceeds 3%. A temporary spike in inflation is not stated to be enough to move the RBA for now.

COVID-19 resurgence

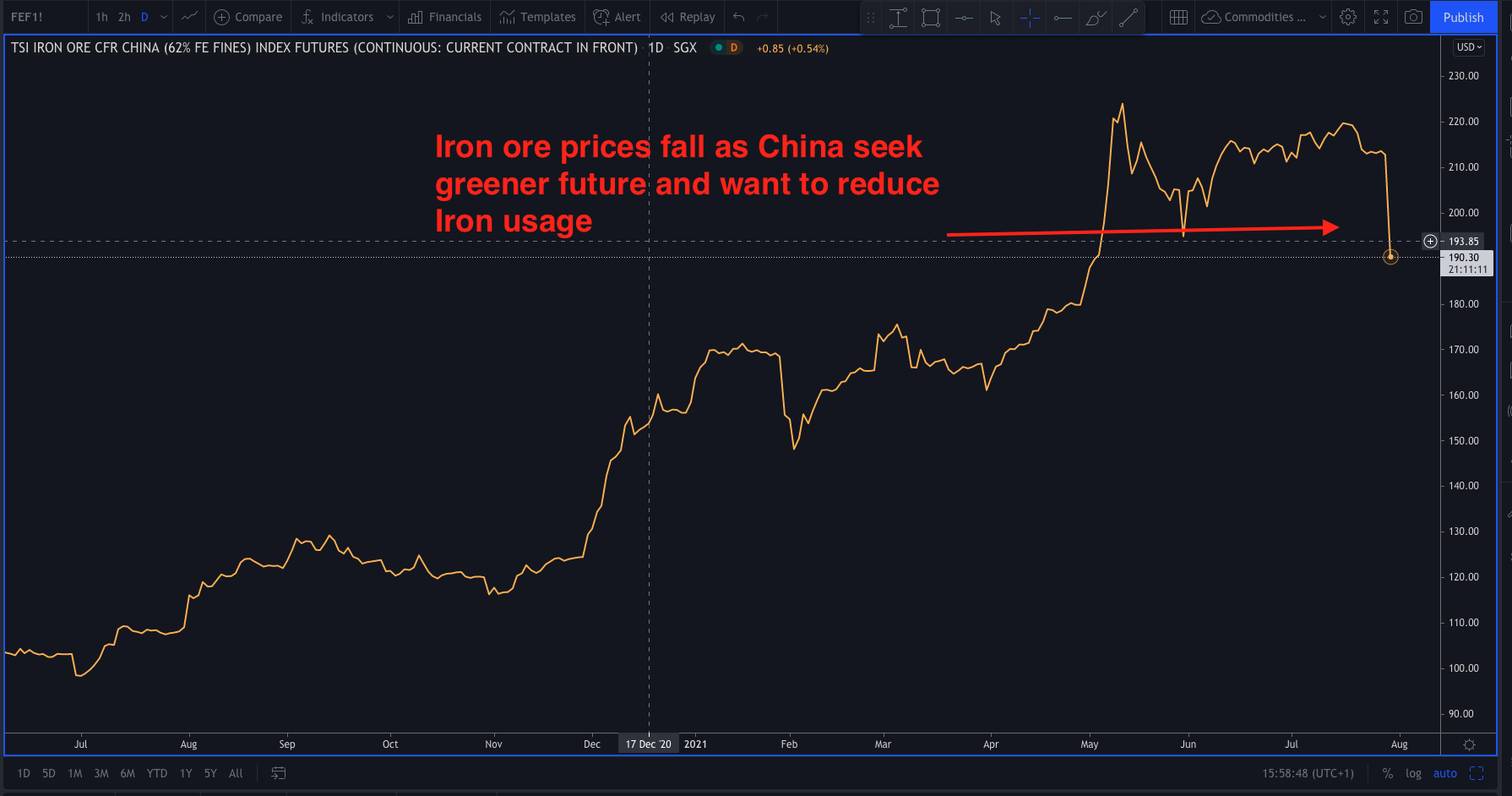

Headwinds now remain for the Australian dollar right now as the nation struggles to manage the rising delta variant. Australia’s New South Wales Premier says that he will tighten COVID-19 lockdown rules in the worst impacted areas of Sydney. The sharp rise of the Delta variant has resulted in a number of strict lockdowns in Australia and that looks set to continue. The RBA is meeting next week and Westpac sees that the RBA may now increase their tapering levels to $6 billion per week.

There is a distinct bias for AUDCAD selling over the course of the next month.

This is especially the case with the recent dip in Iron ore prices this last week.

European Central Bank, President Christine Lagarde, -0.50%, meets September

Dovish tilt in the context

The meeting on July 23 kept interest rates kept unchanged and both the size of the bond purchases (PEPP) were unchanged at €1.85 trillion and AP purchases are continuing at the speed of €20 billion a month. Going into the ECB meeting there were expectations that, after the ECB’s strategic review, the ECB would be revealing a more dovish hand. This was hinted at in the run-up to the meeting by Christine Lagarde who said that the PEPP could ‘change’ into something else. However, on Friday July 16 a sources report said that, due to disagreement, the bond purchases would be left unchanged/not mentioned until September’s meeting. This would have marked a shift from the June 10th meeting where a sources piece revealed that three ECB board members were in favour of bond tapering.

‘Marginal’ disagreement

Christine Lagarde noted in the press conference that there was some ‘marginal disagreement’. It was not surprising as within the GC are fiscal conservatives like Germany and the more liberally minded Italians, so getting an agreement was always going to be tough. Germany’s Weidmann & Belgium’s Wunsch opposed the ECB’s new guidance according to Bloomberg/sources as it signalled a commitment to lower rates for longer. In addition to these two members, sources note that several more voiced objections due to the length of commitment and a lack of clarity. The ECB will accept an overshoot of inflation which they expect to be temporarily higher. Remember, they now have a symmetric 2% target. Some members wanted to aim for ‘at least 2% inflation’, not just 2% inflation.

The takeaway?

The ECB did not deny the dovish expectations, only disappointed with a lack of action at their last meeting. It looks like setting up for a lower for longer message in September, but with internal disagreement. The path of least resistance is to see it as euro bearish until proven otherwise.

The EURGBP pair looks weak as the BoE meets next week and both Ramsden & Saunders are more hawkish now.

Bank of Canada, Governor Tiff Macklem, 0.25%, meets September 08

At the last meeting the BoC held rates at 0.25% but the surprise this month was that the central bank was a little more neutral than many market participants were expecting. Yes, they cut asset purchases from $3 bln top $2 bln and they still see lifting rates around 2022 however, the adjustment was expected. The BoC note the ‘continued progress towards recovery and the Bank’s increased confidence in the strength of the Canadian economic outlook’. The last BoC meeting had been a holding meeting after the hawkish surprise they gave in April and this was far more neutral in tone.

Inflation

Like the Fed, the BoC see it as transitory. The BoC gave a caveat to this by saying that ‘the factors pushing up inflation are transitory, but their persistence and magnitude are uncertain and will be monitored closely’.

Growth

The BoC expects growth of around 6% in 2021 (lower than previously forecast), 4½% in 2022 (revised higher) and 3¼% in 2023. Consumption is expected to lead the domestic recovery and international demand to underpin an exports recovery.

COVID-19

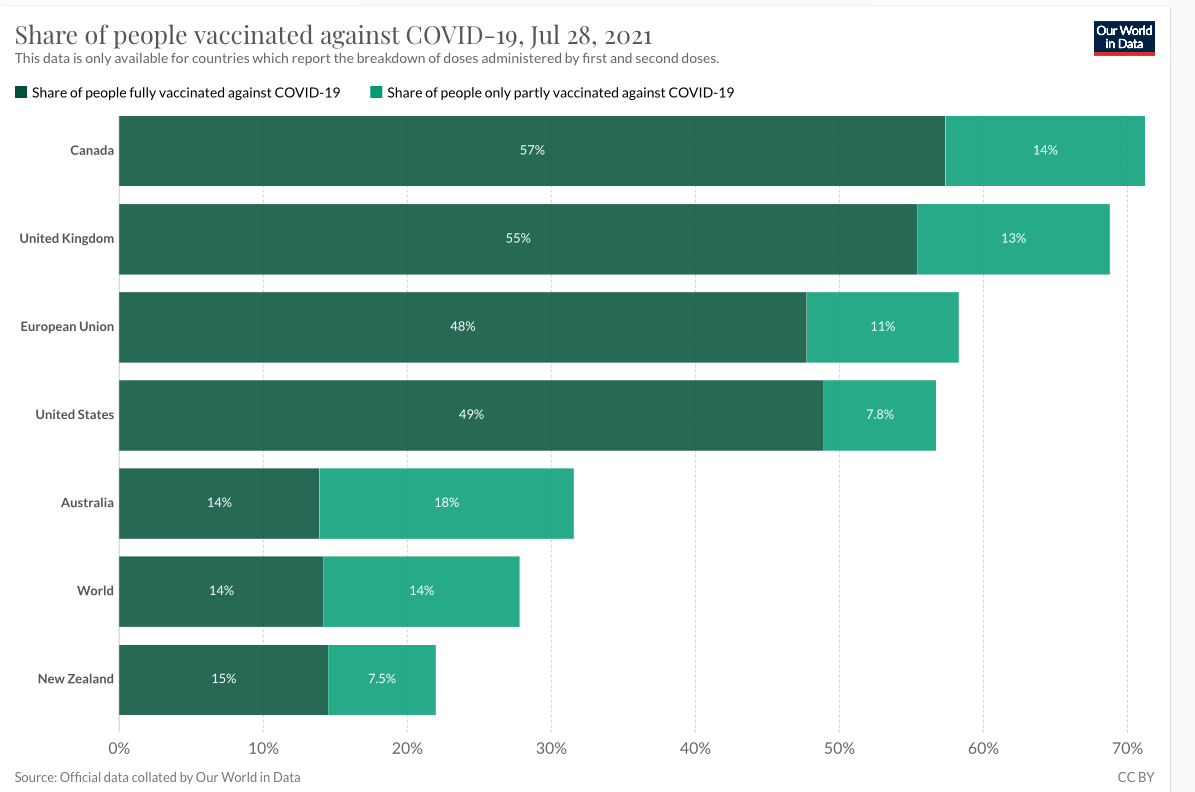

The broad view was one of vaccine confidence with a touch of uncertainty concerning the delta variant and spreading where vaccination rates were low, However, Canada has vaccinated around 57% of their population.

The takeaway

Nothing much to note aside from the fact that CAD should remain supported. As long as the AUD remains weak then the AUDCAD downside makes sense for the month ahead.

Remember too that stronger oil supports the CAD as around 17% of all Canadian exports are oil-related. There is a negative correlation between USD/CAD and oil has broken down recently. Canada’s top export is Crude Petroleum at over $66 billion and around 15.5% of Canada’s total exports.

Federal Reserve, Chair: Jerome Powell, 0.125%. meets August 26-28

Powell edges towards tapering

In the June meeting, 7 members were looking for hikes in 2022 and 13 members in 2023. This was a significant jump from the March meeting where only 4 members saw a hike in 2022 and 7 members saw hikes in 2023. This resulted in the US10 year yields jumping higher and gave the USD a bullish boost. At the meeting this week there were no economic projections due, so that left Powell with an open hand to maintain his regular dovish hand. He achieved this with gold moving lower out of the meeting. However, there was some edging towards tapering.

Substantial further progress?

This is the test for the Fed. Question: What does it mean? Answer: Whatever the Fed wants it to mean, and it is not worth the effort trying to ascertain what economic criteria have to be met for this to be fulfilled This is clearly more a ‘gut feel’ thing and the Fed will have met that test when they say it has been met. It will be easier to tell with hindsight, than foresight. One outstanding area is jobs with the US still 6 million jobs lower than pre-pandemic levels. However, jobs are clearly a key area. In fact, Powell said there is ‘still some ground to cover’ for jobs. However, it is a slight concession that things are looking more positive. One good jobs print with a decent participation rate and that will have animal spirits running and USDJPY soaring higher. Especially as Powell said it should ‘not take long to reach a strong labour market.

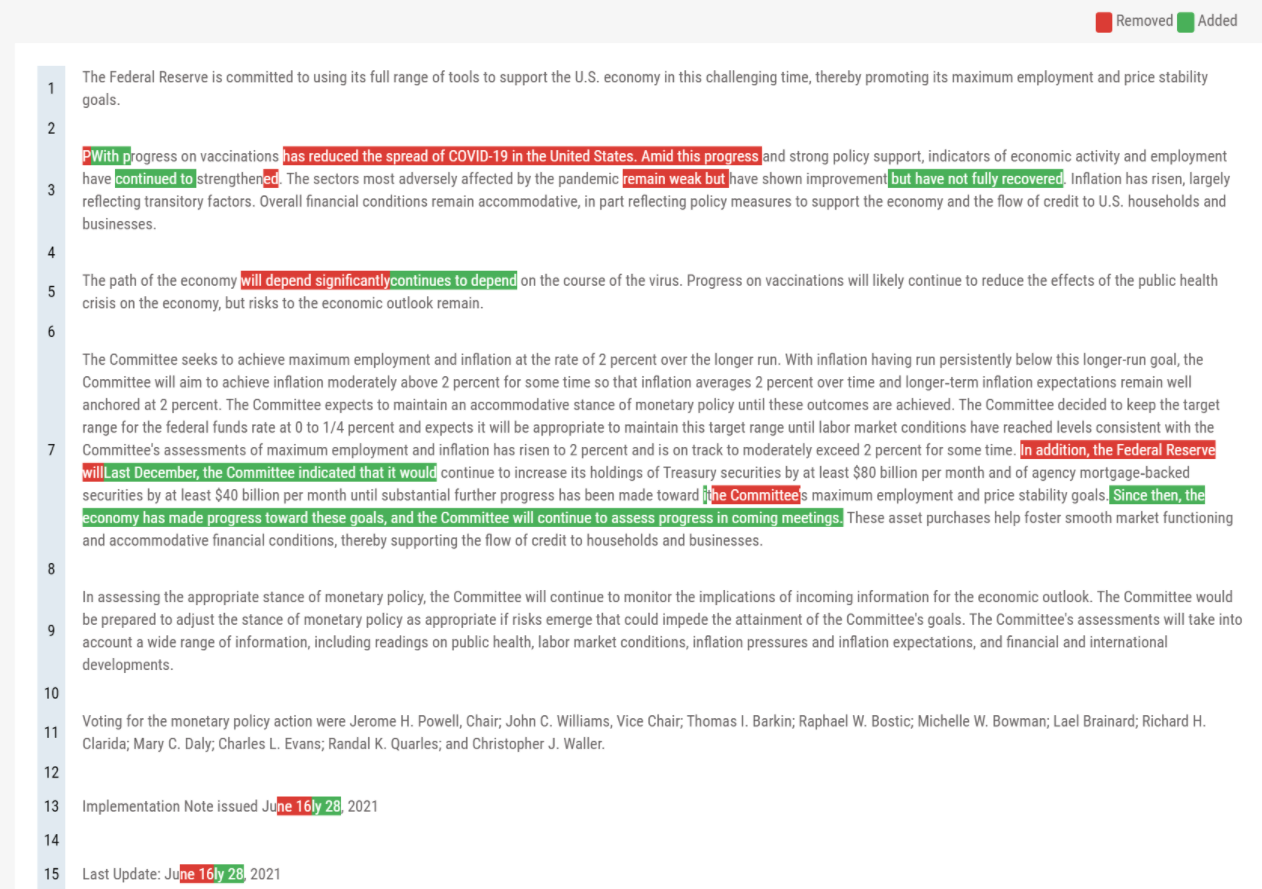

The path of QE stayed at $120 bln per month and guidance was unchanged. The Fed finally launched its standing repo facility. The pandemic was referenced, but vaccine optimism continued to steer the mood. The defat strain was acknowledged by Powell, but not feared. Inflation was recognised as transitory with the chance it may be more tricky. In which case the Fed has tools to address it. Powell said that the Fed were still some way away from raising interest rates and that ideally, the bank would not raise rates until tapering had been concluded.

Federal Reserve statement

The takeaway

In the end, Powell has edged closer to allowing the FOMC board to start tapering. If it is not announced in August, then most economists see September as the time to at least announce tapering. This means that any dips lower in the USD may be transitory and the June 15/16 spike in the DXY seems justified.

If the USD remains weak and real yields low, then gold buying makes sense from $1810. However, a note of caution, if bonds start selling off gain and or the USD gains then gold longs don’t make sense. So as long as real yields are low, and the USD is weak then gold buying is on the cards. Don’t go chasing gold though. Only enter where it makes sense.

Bank of England, Governor Andrew Bailey, 0.10%, meets August 05

Up until this week’s meeting there had been two upbeat central bank meetings from the Bank of England. It could have been anticipated that this would really have increased the odds of a hawkish twist from the BoE. Heading into the Bank of England meeting Sonia futures were pricing in a more optimistic Bank of England with interest rates projected to rise next year. However. The actual meeting itself was a disappointment. The only dissenter to the headline prints was Andy Haldane who voted to taper asset purchases. The vote was 8-1 in favour of tapering. However, this was Andy Haldane’s very last MPC meeting, and a lack of hawkish comment left the GBP stop sell off fairly quickly out of the meeting.

Inflation was considered transitory, so no need to raise rates quickly. The high inflation print from May was acknowledged as being ‘above the 2% target’ (it was 2.1%).

Growth expectations were revised higher by 1.5% with a strong recovery noted in the consumer-facing services for which restrictions were loosened in April. The hot housing market, which could have had the BoE act to contain, was merely seen as ‘strong’. So, no worries there from the BoE.

The meeting as a whole was a very holding affair and August is now seen as the key date for the MPC to ‘fully assess the economic outlook’. Perhaps the BoE will taper next time? One thing for certain is that it now needs Vlieghe and Ramsden to quickly fill the absence of Haldane’s hawkish shoes if the BoE is going to move towards tapering. Ramsden and Saunders have stepped up, but Vlieghe said this week that he wants to keep monetary policy as is for at least several quarters. However, will he change his mind?

GBPJPY longs continue to make sense and a break of 156.00 would open up 160.00. Buying into the BoE makes sense as long as the risk tone is positive.

Swiss National Bank, Chair: Thomas Jordan, -0.75%, meets September

The SNB interest rates are the world’s lowest at-0.75% due to the highly valued Franc. As an export-driven economy, they hate a strong CHF and are doing their best to make it as unattractive as possible. The market generally ignores this and keeps buying CHF on risk aversion which has been here in one form or another since around 2008/2009 according to the EURCHF chart The SNB hate this and repeat, as they did in the latest meeting, that the ‘Swiss franc remains highly valued’. However, recent prices mean the EURCHF long term floor does look in place.

On their June 17 meeting, the SNB left rates unchanged. The inflation forecasts were revised higher again. The reasons cited had increased too from the previous meeting. In the March meeting, it was only oil-related products that were mentioned. In the June meeting, it expanded to ‘higher prices for oil products and tourism-related services, as well as for goods affected by supply bottlenecks’. The new forecast stands at 0.4% for 2021, and 0.6% for both 2022 and 2023. The conditional inflation forecast is based on the assumption that the SNB policy rate remains at −0.75% over the entire forecast horizon. Watch out for high inflation to possibly prompt the SNB into action, but note that we are nowhere near that now.

In terms of growth, the SNB was far more upbeat. In the March meeting, they projected growth of 2.5% -3%. In the June meeting, they noted that the economic indicators had improved significantly of late. Growth for 2021 is now seen at around 3.5 mainly due to the lower than expected decline in GDP in Q1. The statement struck a tone of optimism vs ‘who knows what will really happen. However, a more optimistic note was found in the statement.

The SNB will continue to intervene in the FX markets. The Swiss are always mindful of the EURCHF exchange rate because a strong CHF hurts the Swiss export economy. This is why the opening paragraph, and sentence number two, reads: ‘Despite the recent weakening, the Swiss franc remains highly valued’ . The SNB want a weaker CHF. The rest of the world wants CHF as a place of safety in a crisis, so we have this constant tug of war going on.

The SNB are still content to be the lowest of the central bank pack and dissuade would-be investors by charging them for holding CHF. EURCHF for a 6-12 month hold is worth considering and just checking in with the ECB and SNB policy shifts. The ECB may be about to become more bearish, so that could be a dip in the EURCHF worth buying into.

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, meets September 21

The Bank of Japan still remains a very bearish bank and there is no sign of exiting from its easy monetary policy. The latest meeting saw no surprises, and everything was expected in the July 16 policy meeting. For years Japan has struggled to see any inflation, so with inflation rising around the world, it was interesting to see that the BoJ expect consumer inflation to remain around 0% for the time being. Short term inflation rises are seen as transitory, of course.

The headlines were as expected with Interest rates remaining at 0.10%. In a similarly unmoved fashion, the Yield Curve Control (YCC) was maintained to target 10-year JGB yields at 0.0%. The vote on YCC was made by 8-1 votes. The only dissenter was Mr Katoaka who said that it was desirable to further strengthen monetary easing by lowering short and long-term interest rates, with a view to encouraging firms to make active business fixed investment for the post-COVID-19 era.

The general outlook is that the economy will recover at a slightly slower pace than expected in the June meeting due to the COVID-19 induced lockdowns that Japan has experienced. So, the growth outlook for real GDP was tweaked a little with the 2021 median forecast being reduced from 3.8% to 4.0%. However, the 2022 forecast was revised higher to 2.7% from 2.4% and the 2023 median forecast was unchanged at 1.3%.

The new funding scheme announced to help firms adapt to greener climate demands in the future was put into place. These may include (1) green loans/bonds, (2) sustainability-linked loans/bonds with performance targets related to efforts on climate change, and (3) transition finance.

Core CPI was revised higher again, but this time more substantially than June’s projections. 2021’s forecast was revised up to 0.6% from 0.1% and the 2022 forecast up to 0.9% from 0.8%. 2023’s forecast was unchanged. So, that gives us a sense of a 12-month inflation hike. Remember, that low inflation has dogged the BoJ for years so it will be interesting to see how the BoJ cope with rising inflation if and when it comes.

The only thing to say is that there is no change to the perspective that the Bank of Japan is ready to step in to support Japanese equity markets if they are needed to. Aside from this, there is no change expected for the foreseeable future.

Fed vs BoJ favours USD/JPY upside

Longer-term the Fed will move before the BoJ. It may only take one good job report from the US. So, look for decent areas of support for medium-term USDJY buying and just check the US 10-year yields keep moving higher. 108.00 looks an obvious area.

Reserve Bank of New Zealand, Governor Adrian Orr, 0.25%, meets August 18

Coming into the meeting expectations were building for a more bullish RBNZ. The RBNZ delivered. The official cash rate remained the same at 0.25%, but the headline surprise was that the RBNZ agreed to halt additional asset purchases under the LSAP agreement by July 23. This was the move that opened up NZD strength immediately on the decision.

This means that the RBNZ can be considered as setting up for a sooner rate hike than previously projected. Remember in the prior meeting a rate hike was signalled for 2022. This can be considered even sooner now and the ANZ investment bank now sees the RBNZ raising rates in August. The ASB bank had previously called for a November hike this year, but now too have brought that forward to an August hike. The rising business conditions mean that the RBNZ have confidence about the recovery and there are also now more concerns about inflation than in the prior meeting. The Committee stated that they now expect near-term spikes in headline CPI inflation in the June and September quarters. These reflect factors that are either one-off in nature, such as high oil prices, or expected to be temporary in duration, such as supply shortfalls and higher transport costs. The RBNZ showed some uncertainty here too in recognising that they were unsure how the medium-term outlook for inflation would be impacted. The jury is out. However, you can see that halting the LSAP programme shows that the RBNZ does not want to be guilty of overstimulating the economy if inflation is about to rip higher. Interest rate hikes will contain inflation. The RBNZ recognised that the recent rise in house prices has been unsustainable. Some Gov’t action had limited New Zealand house prices like the increase in loan to value restrictions and changes to housing tax policies. Also, extra supply in housing stock is expected to help keep a lid on prices. However, the key line from a monetary policy point of view is that ‘the Committee agreed that any future increases in mortgage rates will further dampen house price growth’. This pretty much shows that the RBNZ are seeing rate hikes coming.

The takeaway

Like last month this keeps open a central bank divergence between the RBA and the RBNZ. The RBA are on hold after their last interest rate meeting and want to see unemployment move down to 4%. The RBNZ, by contrast, now see a rate hike in 2022. The bond yield spread has moved lower, and this makes a sell on rallies for the AUDNZD the obvious trade. If the risk tone remains positive a very deep NZDJPY long makes sense as does an NZDUSD long as long as the Fed don’t look like tapering.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.