At the center is inflation and how “transitory” it will turn out to be

Outlook: The hot news this week is likely Chinese trade data tomorrow and CPI on Thursday, with US CPI on Wednesday, and retail sales and consumer sentiment on Friday. All week we are going to get readings on central bank attitudes toward tapering and by how much inflation is influencing that decision. And oh, yes, earnings season begins.

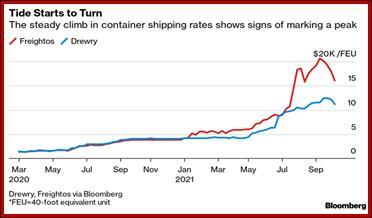

At the center is inflation and how “transitory” it will turn out to be. Just about all central banks are now admitting inflation will be higher and last longer than originally expected, implying they will NOT postpone tapering and hikes. (Having said that, see relief in the form of container shipping delays abating.).

WolfStreet offers this summary of those who are already on the move:

-

Bank of Korea: 1 hike, by 25 basis points

-

Czech National Bank: 3 hikes, by a total of 125 basis points

-

National Bank of Poland: 1 hike, by 40 basis points

-

Central Bank of Iceland: 3 hikes, by a total 75 basis points

-

Norges Bank (Norway): 1 hike, by 25 basis points

-

Reserve Bank of New Zealand: by 25 basis points.

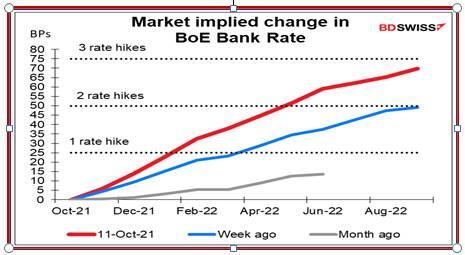

So far the most dramatic remarks are coming from the Bank of England, with Gov Bailey worried about inflation becoming “embedded” while MPC member Saunders used the term “persistent.” New chief economist Huw Pill said the “balance of risks is currently shifting towards great concerns about the inflation outlook, as the current strength of inflation looks set to prove more long-lasting than originally anticipated.” Gittler at BDSwiss offers one of his wonderfully clear charts showing rate hike expectations of two and perhaps three hikes by next August. We think the market is going overboard, but you never know.

One issue not getting enough attention is that the central banks are viewing inflation data in comparison to their targets, which were set long before Covid and supply problems emerged. Granted, we went through the rigamarole at the Fed (and then the ECB) about averaging to allow higher inflation rates for some unspecified length of time, but that old “near 2%” was never changed. So far nobody is challenging it when it’s obvious the central banks are fighting the last war—deflation—when it’s the war before that they should be looking at. They have excuses to avoid facing housing prices up so much in every developed world country (in the US by not measuring it and using proxy data instead). They exclude food and energy from CPI to get core CPI when the average Joe cannot exclude those prices.

We get the last Fed minutes this week but comments from Feds going forward will be more useful. If the market is right, the Fed will move first, before the BoE, and the BoE remarks will be seen as PR. This is still dollar-supportive… as is the looming crisis in China.

Tidbit: the Nobel prize for economics goes to one guy, labor market economist Card from UCal Berkeley, who demonstrated that a rise in the minimum wage does not reduce overall employment, mirroring the 1976 study, and immigrants do not lower pay for native-born workers.

The other winners are from Angrist (MIT) and Imbens (Stanford) who are probability gurus showing that valid conclusions can be drawn about cause and effect even when studies can’t be conducted by strict scientific methods. We need to find out more about this.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat