Another payrolls week rolls around

It’s yet another US nonfarm payrolls week. This indicator has always been the biggie of the month, but now with US inflation well above the Fed’s 2% target, it’s even more important than usual as the determining factor for US monetary policy.

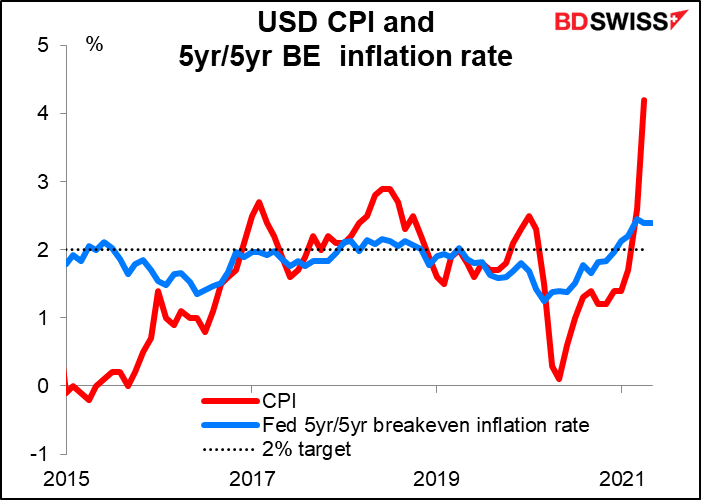

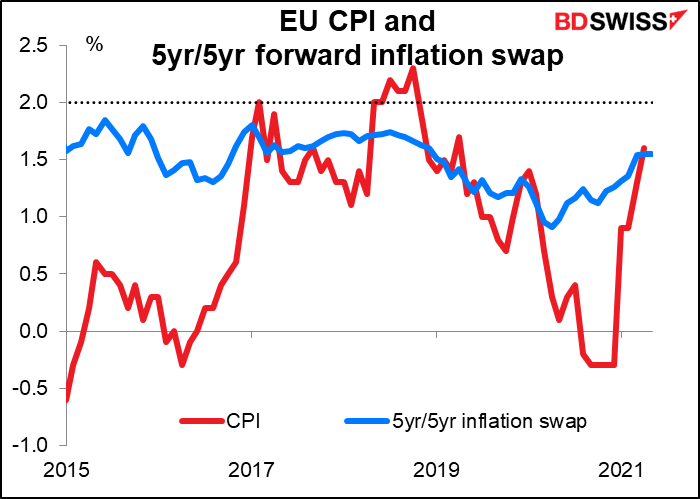

The Fed’s recently revised Statement on Longer-Run Goals and Monetary Policy Strategy said that after inflation has been running persistently below 2%, “appropriate monetary policy will likely aim to achieve inflation moderately above 2 % for some time.” They also said that “longer-term inflation expectations that are well anchored at 2%” are desirable. Well, now we have both of those: the CPI inflation rate jumped to 4.2% yoy in April, while the 5yr/5yr breakeven inflation rate (the inflation rate that the market is forecasting for the five-year period starting five years from now) is 2.4%, i.e. slightly over 2%. The Fed can now rest easy about its inflation goal – indeed, if anything many people are concerned that inflation may exceed its target (although most Fed officials don’t agree.)

That leaves the labor market as the deciding factor in whether the Fed has achieved its targets under its “dual mandate” of “maximum employment and stable prices.”

We’ve recently heard more and more from various members of the rate-setting Federal Open Market Committee (FOMC) that they should start “thinking about thinking about” withdrawing some of their extraordinary monetary stimulus. This follows last week’s revelation from the minutes of the Fed’s April meeting that “A number of participants suggested that if the economy continued to make rapid progress toward the Committee's goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.” Since then we’ve heard similar comments from a few individuals. For example, Vice Chair Quarles Wednesday said, “If my expectations about economic growth, employment, and inflation over the coming months are borne out . . . and especially if they come in stronger than I expect . . . it will become important for the [FOMC] to begin discussing our plans to adjust the pace of asset purchases at upcoming meetings.” He also said that the Fed might have to spell out in more detail what exactly constitutes “substantial further progress…toward our broad and inclusive definition of maximum employment.”

Notice that Quarles said, “our broad and inclusive definition of maximum employment” (emphasis added). This is part of the Fed’s new awareness of how its policies affect minorities in America, a revelation that apparently became clear when it held a series of 14 “Fed Listens” events around the country in 2019 “to hear about how monetary policy affects peoples’ daily lives and livelihoods.”As a result, the Fed has focused intensely on racism over the last few months. Wednesday for example the Minneapolis Fed is hosting the sixth of an 11-part series on “Racism and the Economy,” this time focusing on entrepreneurship. Racism is not a traditional concern of central banks as far as I know.

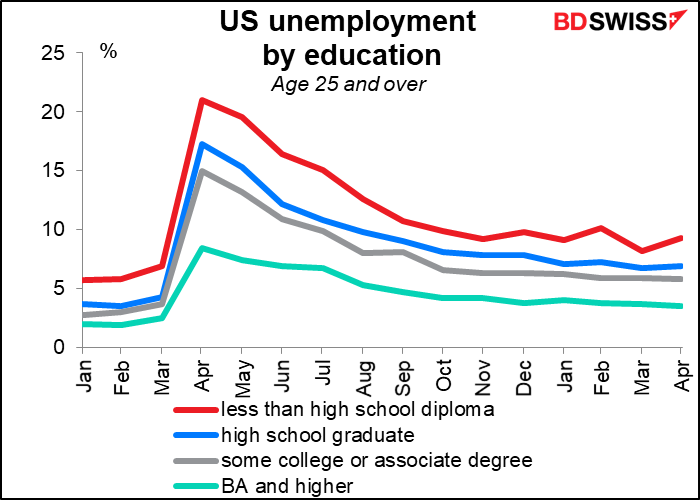

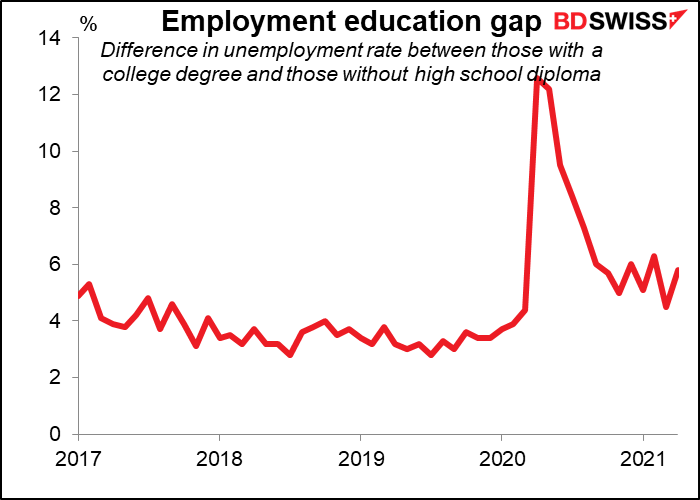

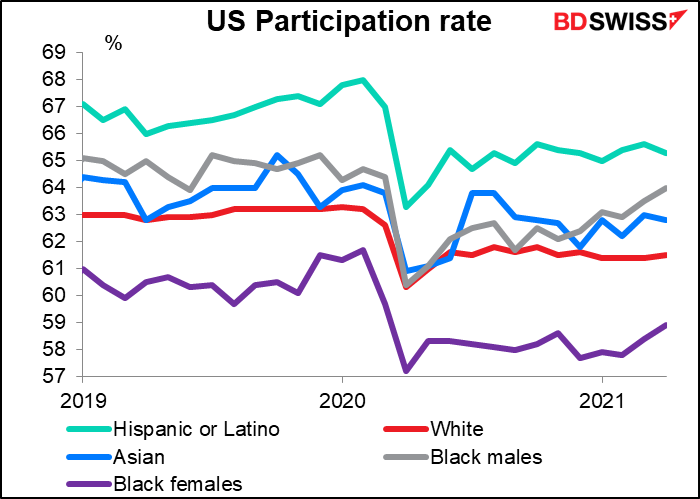

We should therefore look not only at the traditional data, such as the number of new jobs and the unemployment rate, but also other metrics that show how “broad and inclusive” employment gains are. Such as the unemployment rate for people with different educational backgrounds and the participation rate for people of different races. They show that there’s still “substantial” room for “further progress.”

The debate raging among FOMC members about when they should start “thinking about thinking about” tapering their bond purchases seems to be much more serious than the parallel debate among European Central Bank (ECB) Governing Council members. ECB President Lagarde last week said it was “far too early and it’s actually unnecessary to debate longer-term issues,” such as tapering down the bond purchases. Similarly, ECB Council member Panetta noted in an interview this week that he sees no justification for the central bank to slow the pace of bond purchases in the ECB’s Pandemic Emergency Purchase Program (PEPP) at its next meeting on June 10th.

Press reports say that “some conservative central bank governors such as the Netherlands' Klaas Knot are making the case for the ECB to start dialing back its emergency measures and revert to more traditional forms of stimulus.” However, I couldn’t find anyone except for Knot who’s saying this. Even Bundesbank President and uber-hawk Jens Weidmann said, “The emergency purchase program PEPP is clearly linked to the pandemic and will end when it has been overcome. However, no one can reliably estimate when exactly that will be.”

Meanwhile, the single-mandate ECB has neither achieved its inflation target of “close to, but below, 2%” nor have inflation expectations reached that level either.

So while the Bank of Canada is tapering its bond purchases, the Reserve Bank of New Zealand is forecasting rate hikes, and the Fed is at least “thinking about thinking about” tapering its purchases, no such movement is apparent at the ECB. Futures rates reflect this; EUR rates (blue line) are expected to be the second-slowest in rising over the next 2 ½ years, after JPY (green line). Monetary policy diversion could lead again to a lower EUR/USD.

This week: NFP, RBA, G7 finance ministers’ meeting, EU CPI

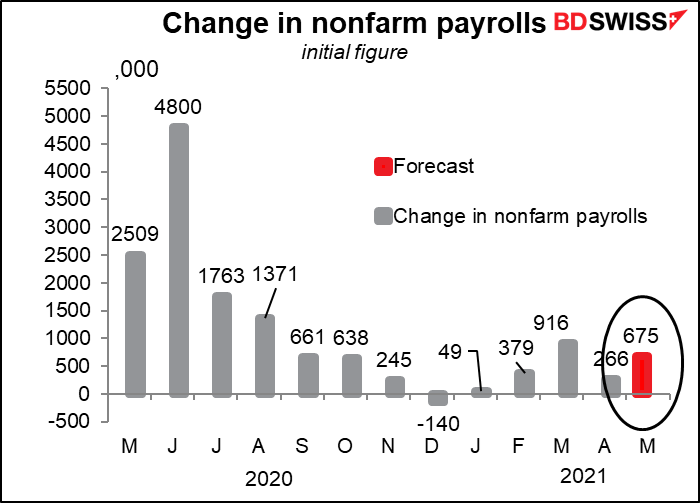

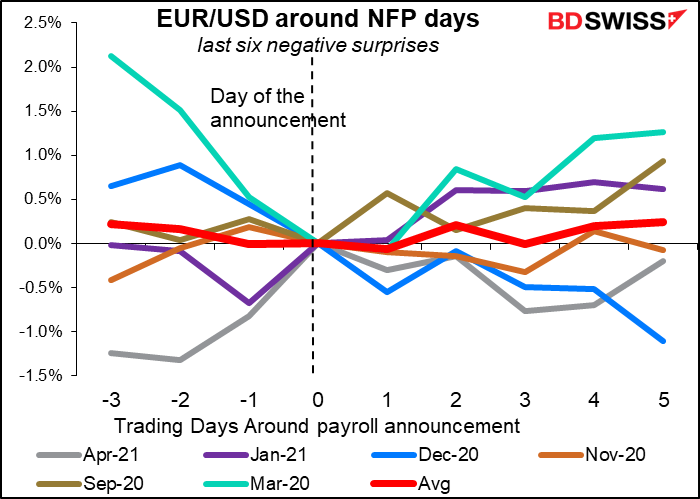

There’s a lot going on this week. As mentioned above, the focus will be on Friday’s US nonfarm payrolls (NFP). After last month’s forecasts of +1mn proved to be wildly optimistic (the actual was +266k), this month economists are dialing back their forecasts. The median is +675k, with forecasts ranging from +335k to +925k. Of course, there’s plenty of time for people to revise their forecasts.

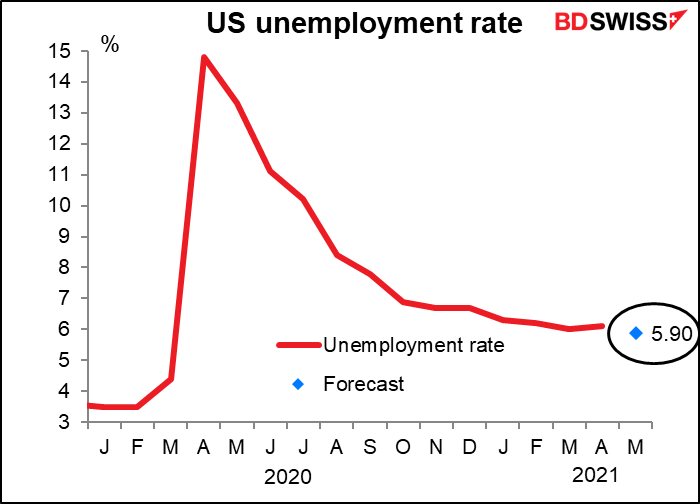

The unemployment rate is expected to fall to 5.9% from 6.1%.

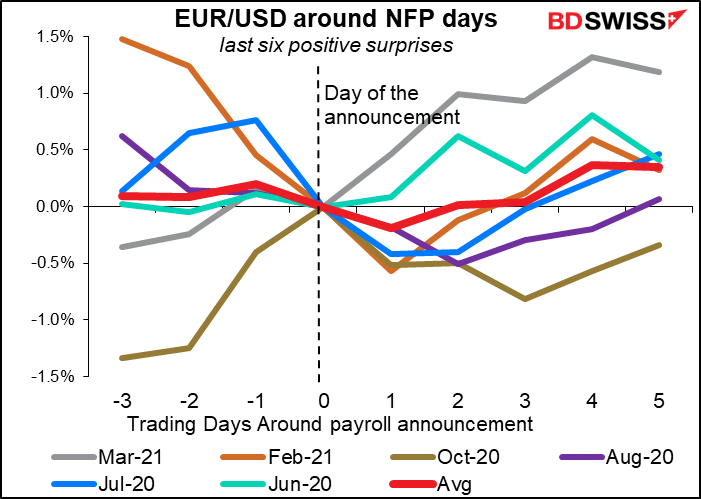

Just from looking at the results, it seems that positive surprises have a more powerful impact on the subsequent movement of the dollar than negative surprises do.

Monday is a holiday in the US (Memorial Day) so the ADP Report, which usually comes out on the Wednesday before the NFP, will be delayed until Thursday. The NFP comes out on Friday as usual though.

Reserve Bank of Australia (RBA) meeting: On hold

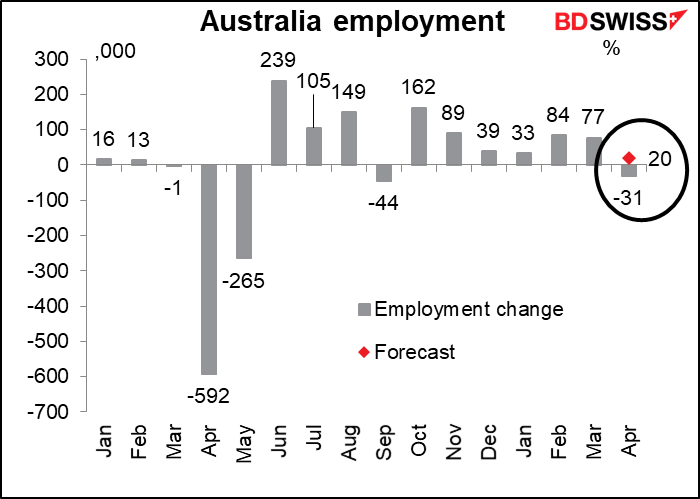

The only major central bank meeting this coming week is the RBA on Tuesday. The other two commodity currency central banks have already started normalizing policy: the Bank of Canada over a month ago started tapering down its bond purchases, while the Reserve Bank of New Zealand (RBNZ) earlier this week published a forecast for its official cash rate that incorporated a rate hike in 2Q next year. Will the RBA follow along? Probably not. At their May meeting, they said they would make key decisions about their yield-curve control and quantitive easing programs at their July meeting. That means little to decide this week. The main point of interest will probably be their assessment of labor market conditions after the disappointing April labor force survey (31k decline in jobs instead of +20k rise as expected).

In other central bank activity, the Fed releases the Beige Book on Wednesday, as usual two weeks before the next FOMC meeting.

The G7 finance ministers meet in London on Friday and Saturday ahead of the June 11-13 G7 Summit in Cornwall, England. This follows today’s virtual meeting of the Finance ministers together with the central bank heads. The finance ministers are expected to agree on some uniform taxation of multinationals. That would give a boost to the formal negotiations taking place at the OECD in Paris and directed by the wider G20 group. There are two aims to the negotiations: one, to set a global minimum tax rate for multinationals, and secondly, to ensure that part of their global profits are taxed based on the location of sales. The goal is to limit the ability of companies to shift profits to low tax jurisdictions and instead to ensure that the big US digital companies pay more taxes in the countries where they make sales. If the finance ministers can reach an agreement, the G7 leaders could formally agree to it at the G7 summit the following week and present the plan to the 139 nations negotiating under the “inclusive framework” at the OECD.

The discussions could be important for the FANG+ stocks that are active globally, such as Facebook, Apple, Amazon, and Google.

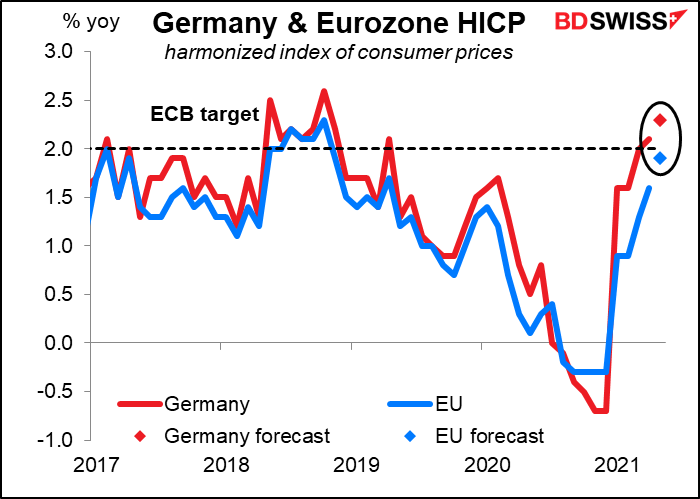

Germany announces its CPI on Monday and the EU-wide CPI is released on Tuesday. Germany is expected to be over 2% yoy, while the EU-wide figure is forecast to be bang on the ECB’s target of “close to, but below, 2%.” However, as we saw above, that’s not likely to be anywhere near enough to spark thoughts of ECB normalization, so it may well pass virtually unnoticed unless perhaps it misses forecasts in which case it could be a EUR-negative factor.

Finally, we get the final purchasing managers’ indices (PMIs) from Markit (manufacturing on Tuesday, service-sector, and composite on Thursday) and with them, the hotly anticipated US Institute of Supply Management (ISM) PMIs for the US.

Last but not least: the biggest event in June

The most exciting thing on the schedule for this month (not necessarily this week) isn’t anything to do with the FX market. It’s the US intelligence agencies’ report to Congress on “unidentified aerial phenomena.” The unclassified report, compiled by the director of national intelligence and the secretary of defense, aims to make public what the Pentagon knows about unidentified flying objects and data analyzed from such encounters.

Author

Marshall Gittler

Trading Analysis