Albert Edwards “Fed is a Slave to the S&P 500”: Would Kevin Warsh Change That?

Society General’s Albert Edwards was at the Bank Credit Analyst annual conference in New York last week.

Also in attendance were Larry Summers, Paul Volcker, and potentially the next Fed Chair, ex Fed-Governor Kevin Warsh.

Edwards’ email comments on Warsh and Summers ring a bell with me.

I was the first speaker and afterward I enjoyed listening to every other speaker at the two-day event. Most notable of the outside economics speakers were Paul Volker, Larry Summers, and most significantly for me, ex Fed-Governor Kevin Warsh. Much to my own regret, I had never familiarised myself with the views of Governor Warsh, who was at the Fed from 2006-11, and played a key role in navigating the Fed through the crisis. He got a rousing reception from the BCA audience as he talked a lot of sense – in particular on how the Yellen Fed has lost its way and current policy is deeply flawed. He explained that the Fed has been “captured” by a groupthink of academics led by the ‘Secular Stagnation’ ideas of his friend, Larry Summers. Rather than admitting they are wrong, this group, who failed to predict the current economic malaise, have constructed this theory to explain why ever more stimulus is required. In particular, Warsh warned that the Fed had become the slave of the S&P.

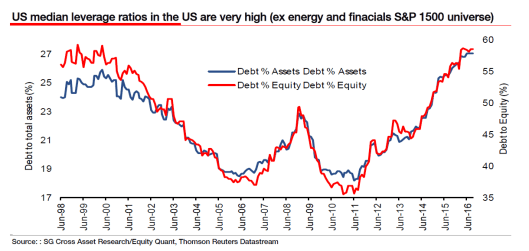

Summers’ relaxed view on the debt build-up, particularly visible in the corporate sector, is in sharp contrast with our own view that this looks set to wreck the US economy.

The problem with Summers’ analysis in my view is that it is the higher debt that is being used to push up asset values (via share buybacks), just as it did during the housing bubble in 2005-7. And by pushing asset values well beyond fundamentals you build debt structures on false asset values, which only become apparent when the asset bubble bursts. And am I in any way reassured that the Fed sees no bubbles? No, I am not. These dudes will never identify an asset bubble – at least before the event!

Median Leverage Ratios

Here we are once again, only this time higher.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc

Mike “Mish” Shedlock is a registered investment advisor for SitkaPacific Capital Management.