2024: Another year of sub-potential economic growth

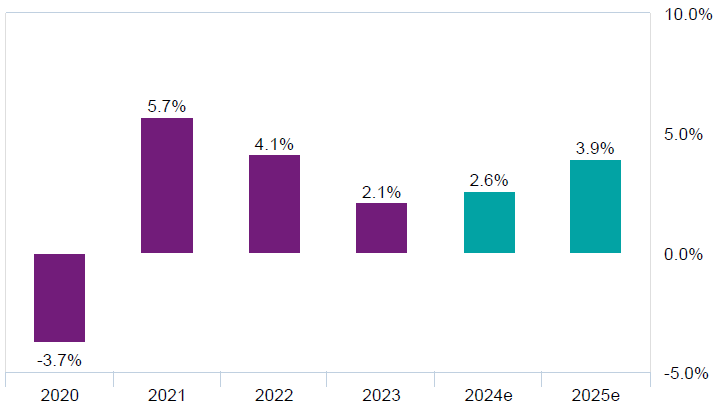

2024 is shaping up to be the second consecutive year with sub-potential GDP growth and with a marginal-to-no correction in the twin deficits, which remain a key concern for markets and the rating outlook. Local and European elections scheduled for June 9 are likely to cement the view of continuity for the current grand coalition beyond 2024. Consumption started the year on a strong footing, supported by robust real wage growth and past saving buffers, and it is expected to be the main growth driver, as public investments could slow at the start of the new Multiannual Financial Framework.

Falling inflation should help boost further real income, with real wages already surpassing pre-commodity shock levels at the end of last summer. Core inflation is forecasted to remain stubbornly above the headline over the next couple of years, which, combined with a tight labor market and strong real wage growth, delays NBR rate cuts vs. CEE peers. The central bank governor offered quite clear forward guidance by saying that the NBR Board discussed in February a potential calendar for rate cuts, and it would be ready to cut rates after at least two months of inflation data releases showing inflation declining after the uptick in January.

GDP (real,y/y)

Source: Erste Group Research

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.