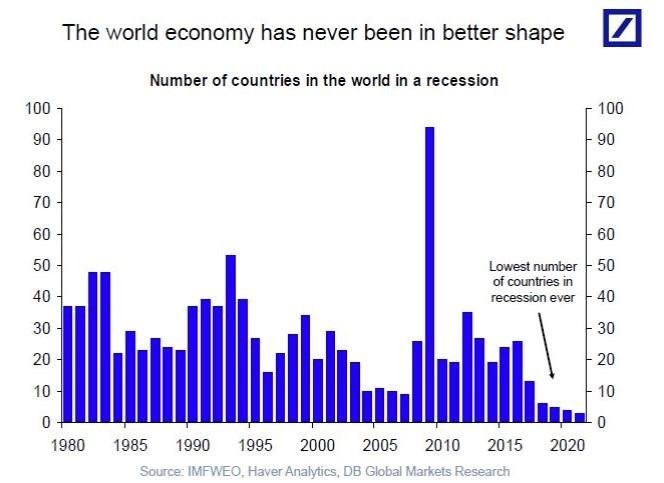

2018 Expected To Have The Fewest Countries In A Recession Ever

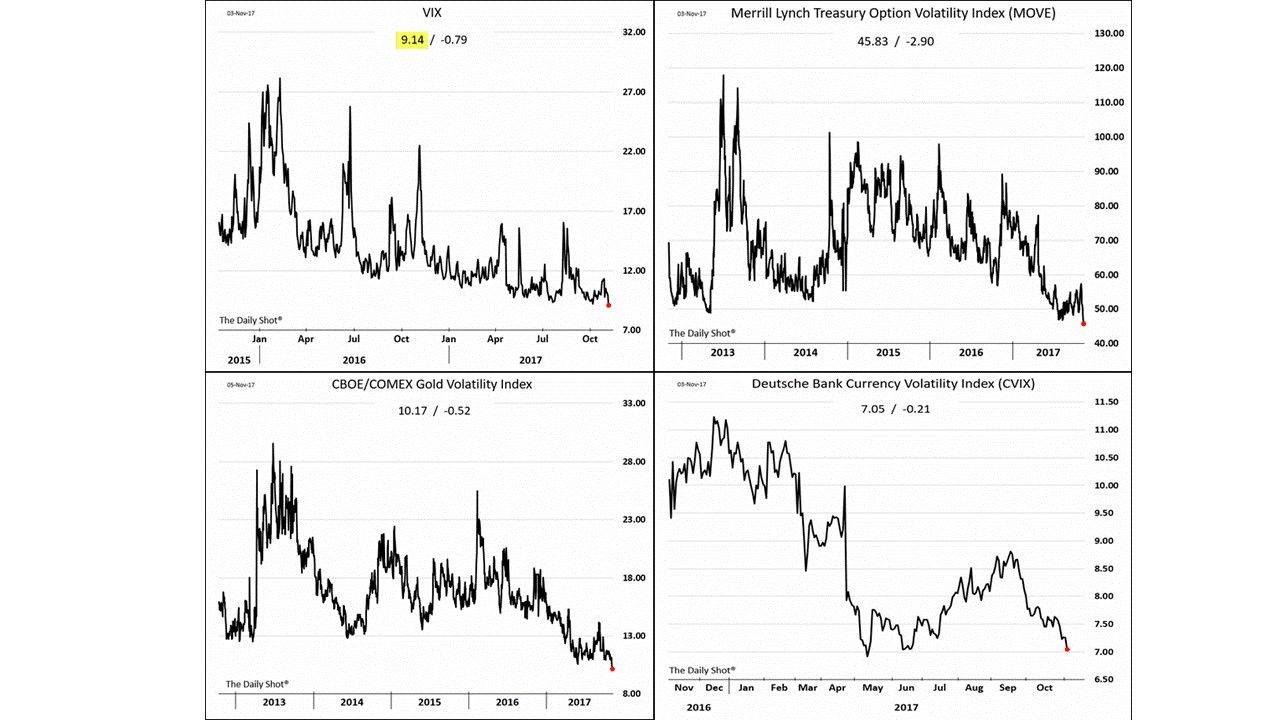

Most Assets See Low Volatility

The stock market had a slightly negative day as the S&P 500 was down 0.02%. The Russell 2000 - RUT was a big laggard as it was down 1.26%. Ever since I warned about it being overextended, it has fallen. The VIX actually had a big up day which was weird since the stock action was so quiet. The VIX was up 5.64% to 9.93 as it remains below the 10 handle. The 4 charts below show the decline in volatility hasn’t been limited to stocks. The currency market, treasury market, and gold market are all seeing near multi-year declines in volatility. Uncertainty isn’t what it used to be. It seems like the market is embracing uncertainty instead of selling off when it occurs. This might be because the issues that are uncertain don’t hold as much weight as the issues previously. For example, the market is now concerned with who will get tax cuts instead of in the past when markets were concerned if Greece would leave the EU and if the entire currency bloc would break up.

Few Countries In Recession

The chart below provides support for this notion that uncertainty is about less important issues as the number of countries in a recession is expected to hit a record low in 2018. This isn’t a perfect indicator since the number of countries in a recession might not matter as much because the number could be swayed by only the small ones. However, the counterpoint to that is it would be almost impossible for only the big countries to be in a recession. This means when there’s a low amount of countries in a recession, the big ones are doing well. This chart shows how broad based the recovery has been as Brazil and China are having good years. India has experienced a slight slowdown which is expected to rebound in 2018. It is a bit disconcerting to see everything working so well. To me, it’s reminiscent of the roaring 1920s. Whenever everything is perfect, it doesn’t usually last long. The chart below goes a few years into the future. While I wouldn’t go as far as saying the 2018 projection is wrong, I think it’s unlikely the record will continually be broken the following 3 years. You can’t just draw a line and continue a trend forever. If that was the case, there would have been no housing burst and stocks would always go up about 8% per year. Don’t get complacent, as this won’t last forever.

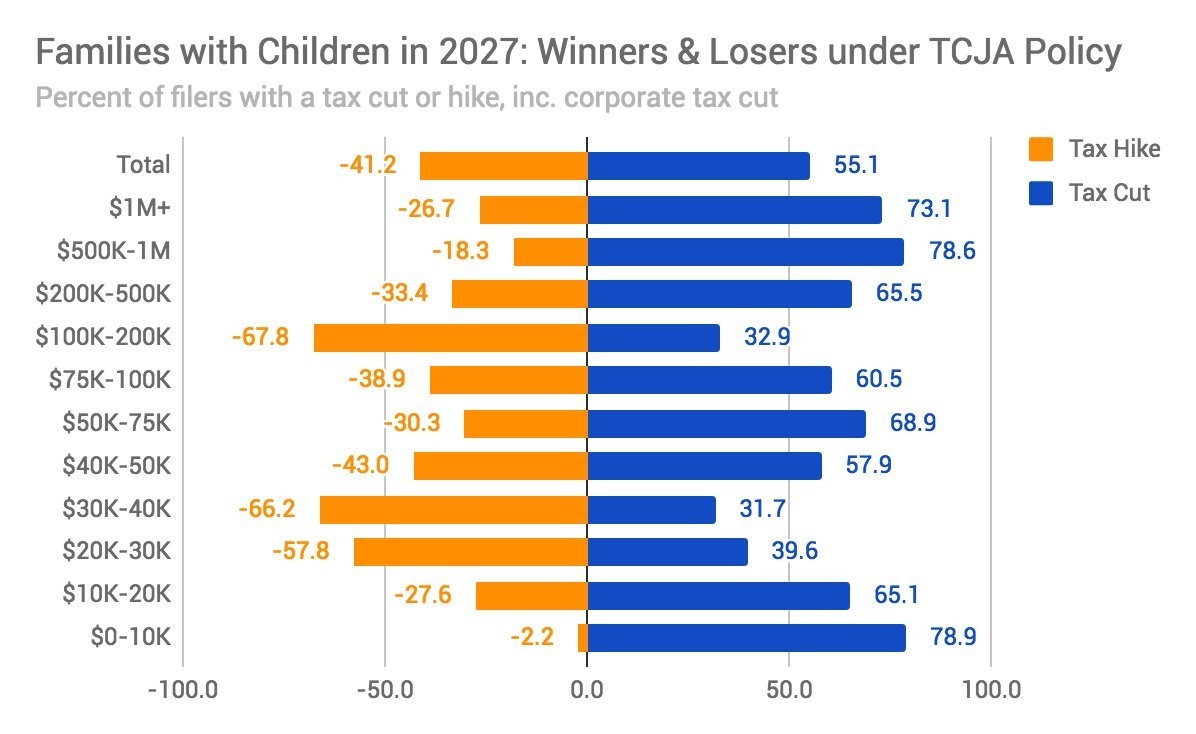

What Tax Cut

The tax cut is looking less and less like a tax cut for millions of American families. We won’t the exact details of the bill until it’s passed. Until then, we are left with analysis like the chart below. As you can see, the results are messy. The likelihood of a tax cut versus a tax increase depends on which income group you are in. Those in the $100,000 to $200,000 group, the $20,000 to $30,000 group, and the $30,000 to $40,000 group all have more people getting a tax increase than a tax cut. The $100,000 to $200,000 income group is very important as the upper middle income group/ lower upper income group is pivotal to consumer spending. The two groups that do the best are the $0 to $10,000 group and the $500,000 to $1,000,000 group. These numbers will be switched up slightly, but it seems likely that whatever is passed, there will be some people who benefit (rich people in low income tax states) and some who will have to pay more taxes (lower income and upper middle income people who live in high income tax states like New York and New Jersey).

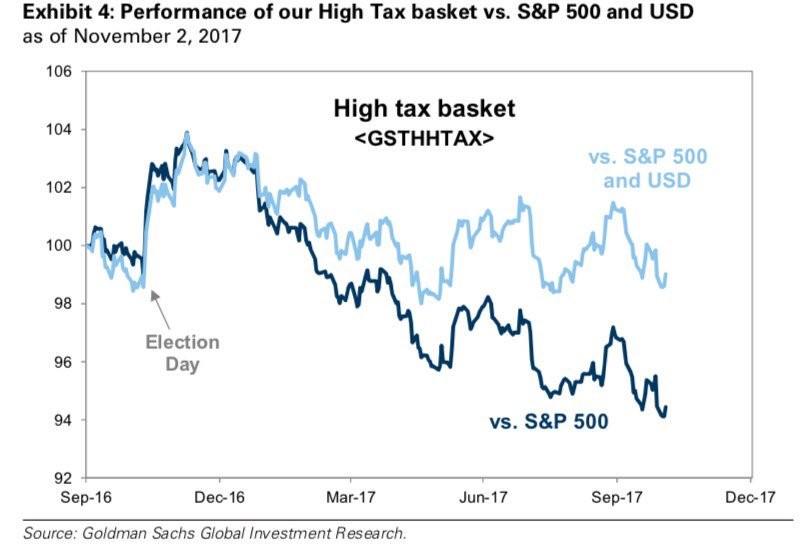

As you can see from the chart below, the high tax stocks continue to underperform the market. This rally is built on global growth and the secular increase in tech margins. It has little to do with tax cuts. The chart also compares the high tax stocks to the S&P 500 and the dollar. The light blue line does better because of how badly the dollar has done. It’s difficult to find an obvious conclusion on where the dollar should go because of tax cuts. They increase the deficit which is bad for the dollar, but they improve growth which is good for the dollar.

The Economy Isn’t Strong?

The chart below is quite damning. We’ve discussed the earnings growth with and without energy, coming to the conclusion that energy made the earnings recession look way worse and made this year’s results better because the comparisons were so weak. The chart below shows the growth in the economy with and without energy. As you can see, without the energy investments this year’s growth would have been 1.03% which is the lowest growth since at least 2011. The energy investments in 2017 contributed to 140 basis points to GDP growth. The good news is that with a solid Q4, this year could be the best one in this recovery. The bad news is the economy is beholden to one sector and that sector is highly volatile. Energy had been doing great until late 2014 when the bottom fell out. Everyone thinks that America becoming the next Saudi Arabia of fossil fuels is a good thing, but it’s not all happiness in paradise. Russia and the OPEC nations have been hit hard since the crash in oil prices.

The price has creeped up lately which is good for energy investment. However, I doubt we will continue to keep up the pace in 2018 because 2017 had extra investment because of the halting of investment in late 2014, 2015, and 2016. The only way I see energy investment and energy earnings growth sustaining anywhere close to the growth rate seen in 2017 would be if oil rallies to the $60s and holds. The earnings growth would fall, but it would still be almost as helpful to S&P 500 earnings. Energy contributed 0.92% to earnings in Q3 2016. In Q3 2017, it contributed 3.56%. If it goes up to 5.5%, the growth rate would be much lower, but the improvement would only be slightly less.

Don Kaufman: Trade small and Live to trade another day at Theotrade.

Don Kaufman: Trade small and Live to trade another day at Theotrade.

Author

TheoTrade Analysis Team

TheoTrade, LLC

Don Kaufman, Co-Founder, Chief Derivatives Instructor (Trader Stocks, Options, Futures) Don is one of the industry's leading financial strategists and educational authorities.