Year ahead – S&P 500: A new bull market in 2025 or a trap?

-

S&P 500 poised to outperform in the year ahead.

-

Accommodative policies and AI optimism could outweigh valuation concerns.

-

Global trade war risks and fewer rate cuts may temper earnings growth.

-

Mid- and small-cap companies could close the gap with larger peers.

It's been a stellar year

Assuming World War III isn’t in the cards for 2025, it's hard to bet against a bullish Wall Street under a new Trump presidency. The US stock market has been a great place for investors, and Republicans will likely want to keep it that way just for the sake of validation. Big US companies are still the safest bet, especially with political and economic uncertainties elsewhere. That said, extreme deregulation could lead to some sharp drops throughout the year.

The S&P 500 had another stellar year, soaring 23% after a 24% gain in 2023—while non-US MSCI indices barely scraped 9%. But there's a familiar pattern: Over the past two decades, the index has been on a bull run for 2-3 years before taking a halt the next year. If history repeats, stock traders may behave more cautiously, speculating a disappointing year either in 2025 or 2026. Mind that the last big dip was in 2022 (-19.44%), but excluding the 2008 crash, declines were usually mild, ranging from 0-6%.

Stretched valuations? No problem... not yet

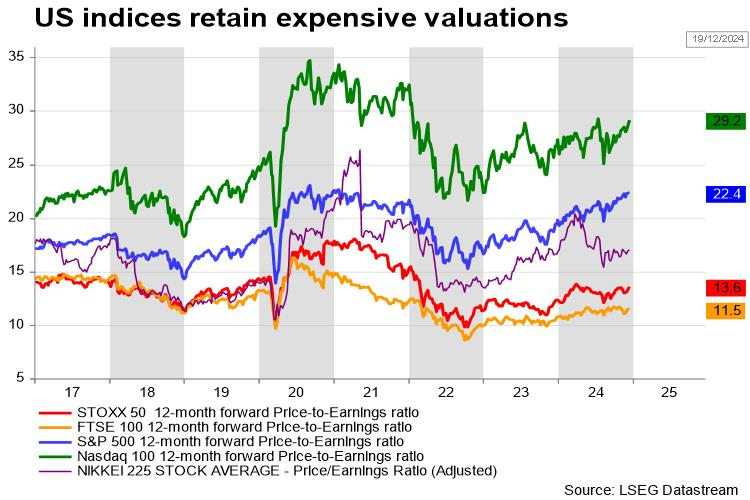

The big question now is whether the market could get choppier as soon as next year. Valuations, which have been a hot topic for over a year, are still in the red zone. With the S&P 500’s forward Price-to-Earnings ratio at nearly 22, it looks pricey compared to its 10- and 20-year averages of 18 and 16. That said, it’s still cheaper than its peaks in 2020 and 1991. In other metrics, Buffett’s favorite market cap-to-GDP ratio is also way higher than usual at 208%, suggesting stocks are outpacing the economy. Plus, Shiller’s Capex index is at its highest since the dot-com bubble and above the typical range of 24-34, warning that stocks might be nearing a cliff edge.

That said, high valuations might take a back seat if earnings guidance can justify them. The four biggest US banks predict the S&P 500 will stay between 6,500 and 7,000 by the end of 2025, with EPS growth of 10-15% compared to 10% estimated for 2024.

Artificial Intelligence is here to stay

Artificial Intelligence may keep driving earnings expectations as investors closely monitor how huge investments in this new technology, which has its links to blockchain, data centers, defense and power sectors, will pay off. Recall that Trump also pledged to make America a blockchain hub. Plus, his pick for Energy Secretary is giving a lift to oil, gas, renewable energy, and infrastructure sectors.

Historic corporate tax cuts could really boost business sentiment during Trump’s second term. With full control of Congress, Republicans have a clear shot at pushing their agenda, including slashing corporate tax rates to 15% for US-made products. This could make manufacturing and real estate stocks even more attractive next year.

Are tax cuts as good as they sound?

However, some opposition could still pop up. Tax cuts might add a whopping $4.6 trillion to the already huge fiscal deficit over the next decade. While everyone loves lower taxes, the Committee for a Responsible Federal Budget warns that the economic boost may only cover 1-14% of the lost revenue. So, the idea that tax cuts will pay for themselves may not be wise, especially if rising bond yields make borrowing more expensive. Keep in mind, stock indices and Treasury yields usually move in opposite directions.

Trade war season two

Import tariffs could become a real headache for US multinational companies, especially with regarding key trade partners like China, Mexico, and Canada. While budget and migration issues could be prioritized in the first half of the year, Trump will eventually turn to foreign policy. He has already warned about imposing a 10-20% tariff on all imports and a 60% tax on Chinese goods to bring manufacturing back to the US.

So far, the market’s been pretty calm about tariff talk, as investors are more prepared than they were during the pre-pandemic US-China trade war. Some even think these threats are just a strategy to get big trade players to negotiate. But a potential trade war should not be underestimated—especially with the geopolitical climate being so tense and uncertain, retaliation might turn out hard. If tariffs do hit, US companies might pass the costs onto consumers, or look into relocating factories, which could again be costly and a time-consuming process. Mergers and acquisitions might also be on the table, which could benefit bank and finance stocks.

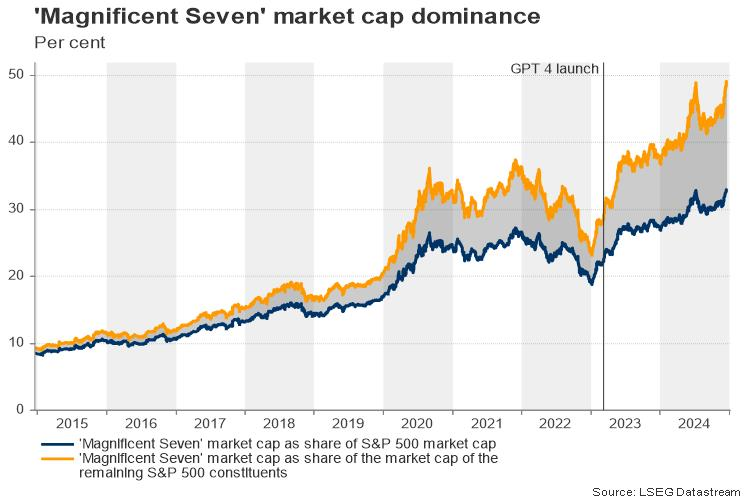

Magnificent Seven and concentration risk

The "Magnificent Seven" have been tested in all grounds and could survive once again given their know-how and huge market shares, but supply chain issues and inflation concerns could make traders reduce their exposure to these stocks, likely slowing their earnings growth, maybe to lower double-digit or event to single-digit levels. Meanwhile, smaller companies could have a shot at catching up, especially with price premiums and less exposure to foreign factories. But for that to happen, the US economy needs to stay strong, and monetary policy needs to stay accommodative. Otherwise, if the economy starts to show cracks, Wall Street could be hit harshly given its concentration to few mega-tech and AI-related stocks such as Nvidia.

Lower interest rates

Finally, the Fed’s rate cut policy will definitely keep traders busy. With Trump backing Jerome Powell's tenure until 2026, we could see a smooth transition into the new year. However, with rising tariffs, tax cuts, and migration controls threatening a resurgence in inflation pressures above the central bank’s 2.0% target, businesses may receive fewer rate cuts next year, as hinted by the Fed's latest dot plot. Remember, it's been the mix of rate cuts, a strong economy and AI optimism that fueled the 2024 stock rally. If that support weakens, traders might have a rough time ahead.

Author

Christina joined Trading Point in May 2017. She holds a master degree in Economics and Business from the Erasmus University Rotterdam with a specialization in International economics.