Wake Up Wall Street (SPY) (QQQ): Why investors need to worry whether Russia invades Ukraine

Here is what you need to know on Friday, January 21:

Equity markets staged the anticipated dead cat bounce we commented on yesterday in our preview note. US equities were for the most part up 1% at the halftime stage yesterday but stumbled thereafter to close comfortably in the red. The NASDAQ was the biggest loser, down 1.34% on Thursday, while the S&P 500 and Dow were down around 1%.

Things are not looking any better on Friday with the Dax taking a hammering in Europe and Netflix cratering overnight. The IMF adds further confusion by saying it feels the Fed hiking rates could hurt the global recovery. Already we are seeing benign economic indicators with yesterday's jobless claims another warning sign adding to the alarm bells from US retail sales and consumer sentiment last week. Stagflation is looking more possible than ever.

We still remain optimistic, though the short term may see some more pain. It is now becoming clear that earnings season is not what we hoped, but this may turn around next week as the tech sector weighs in. Netflix (NFLX) and Peloton (PTON) just merely reversed the ascents seen during the pandemic, but tech giants should be more stable in their earnings profile. If not, then we will start to worry.

The UK is on the verge of a full reopening, as is Ireland, while Spain is also easing. The developed world is set to fully get back to normal, and we still note the pent-up demand and savings profile that is yet to be fully unleashed.

We did allude to rising geopolitical tensions yesterday, and today's meeting between US and Russian foreign ministers did little to change things. A Russian invasion of Ukraine is a high probability, according to President Biden, and we feel markets have yet to give this much credence. Commodity markets are starting to notice as Russia is a major commodity exporter. It is the world's second-largest oil producer and a major gas supplier to Europe. Military action is unlikely to see a military response from the US. Instead, both the EU and US will go for harsh sanctions. Sanctions will cause commodity price hikes, so think of those defensive stocks that may benefit as Russian military action could see a sharp 5% to 10% fall in the S&P 500.

The dollar has weakened somewhat this morning to 1.1350 versus the euro, while Oil is flat at $84.44. Gold is also flat at $1,836, but Bitcoin has finally moved, down 5% at $38,400. Russia likens it to a pyramid scheme.

European markets are lower: Eurostoxx -0.2%, FTSE -0.2% and Dax -2.1%.

US futures are also lower: S&P -0.6%, Dow -0.3%, and NASDAQ down another 1%.

Wall Street (QQQ) (SPY) Stock News

China urging banks to increase lending. Signs of a slowdown?

UK retail sales -3.7% versus -0.6% forecast.

IMF says Fed rate hike may hurt the global recovery.

Netflix (NFLX) craters on poor subscriber growth and poor subscriber forecasts.

Peloton (PTON) drops 24% on rumours of production halt due to high inventory, company denies.

Tesla (TSLA) finished green on Thursday, strong ouperformance.

Schlumberger (SLB) up 1% premarket on earnings beat.

Intel (INTC) to invest $30 billion in new plant in Ohio.

Rio Tinto (RIO) drops 2% after Serbia revokes lithium licenses.

Toyota (TM) halts production in some Japanese factories due to covid.

IBM to sell healthcare data division.

Moderna (MRNA): Bank of America upgrades and UBS gives $221 price target.

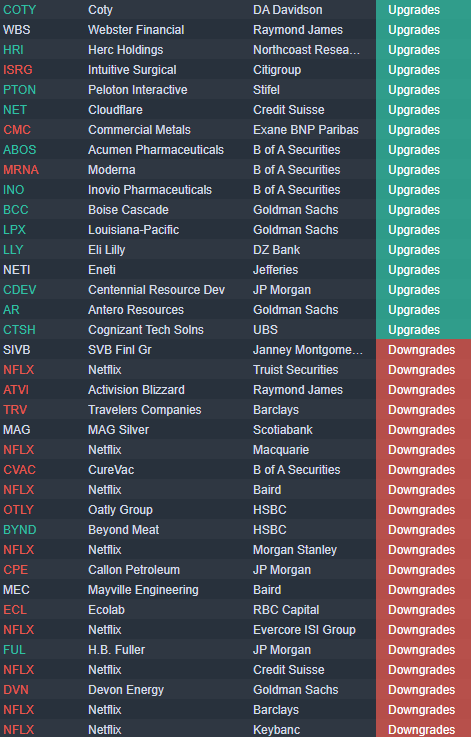

Upgrades and Downgrades

Source: Benzinga Pro

Economic releases

Like this article? Help us with some feedback by answering this survey:

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.