Japanese Yen drags a historic rate hike into intervention country

- USD/JPY closed at its highest level since July 2024.

- US headline inflation hit a fresh cycle high and barely moved the price.

- A BoJ hike next week is fully priced and the Yen still cannot rally.

The Japanese Yen just logged its weakest close in nearly two years on the same day US inflation printed a fresh cycle high, and the most interesting part of the session is what did not happen. USD/JPY ground to a finish around 160.50 on Wednesday, its highest close since July 2024 on the weekly chart, shrugging off both a soft core inflation surprise and the looming Bank of Japan (BoJ) decision next Tuesday, where markets have fully priced a quarter-point hike to 1%, a level the policy rate has not seen since the mid-1990s. A currency that cannot rally on a near-certain hike to a three-decade high suggests the official narrative has the causation backwards: the BoJ is not hiking because inflation demands it, it is hiking because the exchange rate does.

A hike built on forecasts, not prints

The genuinely awkward detail is that Japan's last national Consumer Price Index (CPI) reading came in at just 1.4% YoY, below the BoJ's 2% target, while the bank's own fiscal-year forecast near 2.8% leans almost entirely on imported energy costs that the Strait of Hormuz disruption keeps feeding. The sequencing is stranger still, because May's national CPI lands Thursday night at 23:30 GMT, two days after the decision, meaning the BoJ will move before seeing its own most recent inflation data. Central banks that tighten on forecasts rather than prints are usually defending something other than the price level, and with the pair camped above the line that drew record intervention in 2024, it is not hard to guess what.

The carry that refuses to die

The rate differential explains why the Yen cannot monetize any of this. Friday's 172K Nonfarm Payrolls (NFP) print erased what remained of Federal Reserve (Fed) easing bets, and CME FedWatch now shows a hold next Wednesday around 98% priced, with roughly 70% odds of at least one hike by the December meeting and better than one-in-four odds of two. A gap that was supposed to compress from both ends is barely compressing at all, the carry still pays every day the Yen stays flat, and Japan's energy import bill keeps structural Dollar demand humming underneath. Wednesday's tape made the point with unusual clarity: headline CPI printed 4.2% YoY with the core reading soft at 0.2% MoM, the pair dipped for roughly an hour, and the bid returned to push it to fresh session highs into the close. The session low, set during the Asian morning just above 160.00, never came close to a retest.

Tokyo's awkward waiting game

The Ministry of Finance (MoF) now faces a timing problem with no clean answer, since intervening days before its own central bank hikes looks panicked, while standing aside risks letting speculators conclude the 2024 defense line has quietly moved. History says the MoF cares about velocity more than level, and this grind has been orderly, persistent, and precisely the kind of move that is hardest to justify fighting. The rest of the week offers no domestic circuit breaker either, with the Japanese docket empty until the decision itself, leaving the pair to trade Thursday's US Producer Price Index (PPI) release at 12:30 GMT, where consensus sits at 6.4% YoY, and Friday's University of Michigan (UoM) survey at 14:00 GMT, where one-year inflation expectations last printed near 4.8%. Hot numbers there push the pair deeper into intervention country before Tokyo has even spoken.

Levels and bias

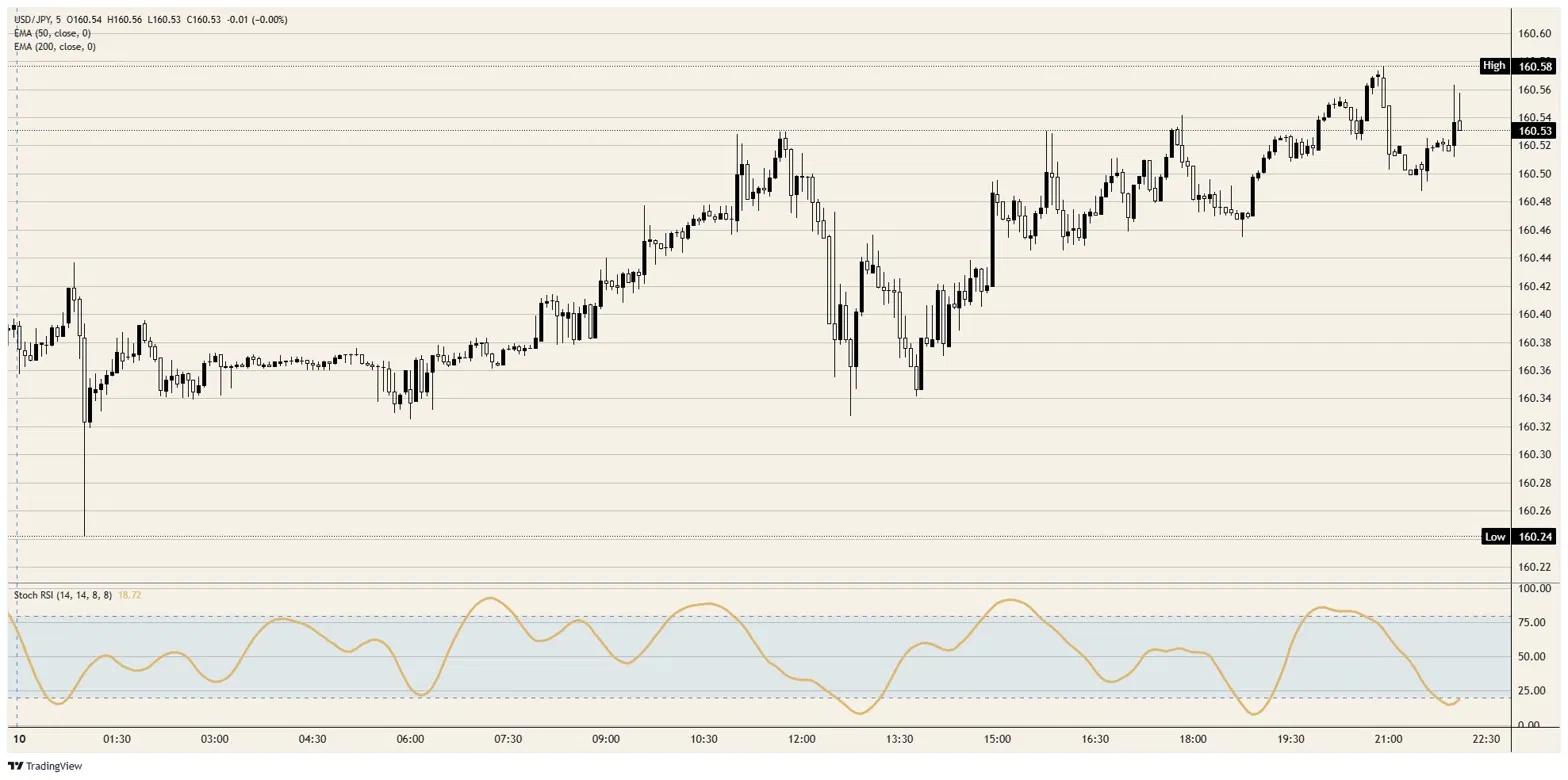

Upside: beyond Wednesday's highs around 160.50 sits the late-April spike close to 161.00, then the 2024 extreme just shy of 162.00, with everything in between exposed to headline risk out of Tokyo. Downside: the 160.00 handle held all session and remains the first test, with the rising 50-day Exponential Moving Average (EMA) near 159.00 the more meaningful floor. Bias: structurally bid, tactically treacherous. Daily momentum is pinned deep in overbought territory on the Stochastic Relative Strength Index (Stoch RSI) heading into a week containing two central bank decisions and a live intervention threat, an asymmetry that favors sharp air pockets over smooth continuation.

USD/JPY 5-minute chart

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The BoJ ultra-loose monetary policy between 2013 and 2024 caused the Yen to depreciate against its main currency peers due to an increasing policy divergence between the Bank of Japan and other main central banks. More recently, the gradually unwinding of this ultra-loose policy has given some support to the Yen.

Over the last decade, the BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supported a widening of the differential between the 10-year US and Japanese bonds, which favored the US Dollar against the Japanese Yen. The BoJ decision in 2024 to gradually abandon the ultra-loose policy, coupled with interest-rate cuts in other major central banks, is narrowing this differential.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.